Key Takeaways

- Investment Arbitrage in Altitude: The shift to kiwi and avocado is not just farming; it’s a calculated arbitrage play. Investors are exploiting the massive price and value-density gap between low-yield subsistence crops and high-demand premium fruits, a gap magnified by Nepal’s unique agro-climatic advantage over the vast, hot plains of India.

- The Patient Capital Revolution: This agrarian transition is fueled by a new class of “patient capital” from family offices and diaspora investors. They bypass the quick-flip mentality of other sectors, embracing 5-to-7-year gestation periods for orchard maturation in exchange for long-term, high-multiple returns that traditional short-cycle agriculture cannot offer.

- Land Aggregation as the New Moat: The primary barrier to entry and the key determinant of success is not horticulture, but mastering the legal and logistical complexities of land aggregation. The most strategic players are building competitive moats by pioneering long-term lease agreements with hundreds of smallholders, effectively unlocking the value of fragmented, underutilized land.

Introduction

Travel through the terraced mid-hills of Nepal, from the windswept valleys of Mustang to the temperate slopes of Dhankuta, and you will witness the quiet beginnings of an economic revolution. For generations, these lands have been a patchwork of maize, millet, and potatoes—staples of subsistence, tethered to the hard realities of local consumption and marginal returns. Today, a different kind of seed is being sown. In cleared plots, meticulously laid out in grids, you will find the saplings of kiwi and avocado. This is not the work of subsistence farmers; this is the work of spreadsheets.

A new class of investor—urban, data-driven, and globally aware—is orchestrating a fundamental agrarian transition. Elite capital, from Kathmandu-based business houses to the returning diaspora, is aggregating land not for traditional staples, but for high-value, long-gestation fruit cultivation. They are trading the certainty of low-margin grain for a calculated, multi-year bet on premium produce. This is a deliberate pivot from agriculture as a way of life to agribusiness as a high-return asset class. The central question is not *what* is being planted, but *why* this specific shift is happening now, and what it signals about the future of investment in Nepal.

This analysis will deconstruct the economic machinery driving this trend. We will investigate why smart money is chasing kiwi and avocado, moving beyond the simplistic narrative of “diversification” to explore the core drivers: the compelling unit economics of high-value crops, the powerful pull of export demand from India’s burgeoning consumer class, and the sophisticated risk-mitigation strategies that transform orchard-based agribusiness from a gamble into a calculated, long-term investment. This is the story of how Nepal’s geography is finally being weaponized as its primary commercial advantage.

From Subsistence to Spreadsheets: The New Economics of the Mid-Hills

The decision to replace a field of maize with an orchard of avocados is not an emotional one; it is a cold, rational calculation of value per unit of land. The economic logic is so overwhelmingly compelling that it is fundamentally altering the perception of agricultural land, from a low-yield legacy asset to a high-performance one. The core concept driving this is “value density”—the ability to generate dramatically higher revenue from the same finite parcel of land. A ropani of land (approximately 5,476 square feet) cultivated for maize might yield an annual gross revenue of NPR 15,000 to NPR 20,000. That same ropani, once a kiwi orchard reaches maturity in 5-7 years, can generate upwards of NPR 250,000 annually, a more than tenfold increase in revenue productivity.

This differential rewrites the entire financial model of farming. Traditional agriculture is a game of thin margins and high volume, a model ill-suited to Nepal’s fragmented landholdings. High-value horticulture, however, thrives on this very constraint. It allows an investor to achieve commercial scale and significant revenue from a relatively small, consolidated land area of 50 or 100 ropanis. This makes the daunting task of land acquisition or leasing manageable. Investors aren’t buying entire districts; they are creating focused, high-density profit centers. This economic reality has triggered the most critical activity in the sector: land aggregation. Since Nepal’s land laws and fragmented ownership make outright purchase of contiguous plots nearly impossible, the dominant model is the long-term lease. Visionary entrepreneurs are approaching hundreds of smallholder farmers in a target area and offering them a 30-to-40-year lease. For the farmer, this converts an underperforming, labor-intensive asset into a source of stable, passive annual income, often exceeding what they could earn from farming it themselves, all while freeing them from the risks of crop failure and volatile market prices. For the investor, it provides the scale necessary for a commercial orchard, the security of a long-term tenure to justify capital expenditure, and a powerful barrier to entry for competitors.

Furthermore, the labor dynamics of orchard-based models are uniquely suited to Nepal’s modern rural economy, which is heavily shaped by youth out-migration and remittance inflows. Subsistence farming demands constant, year-round labor—a resource increasingly scarce in villages populated by the elderly and children. An orchard, by contrast, has intense labor requirements during specific phases: initial planting, annual pruning, and seasonal harvesting. These peaks can be managed by hiring skilled, mobile teams of workers, a far more scalable and efficient model than relying on a dwindling pool of household labor. An investor can systematically manage a portfolio of orchards across different locations using professional teams, whereas a family is tied to a single plot. This structural alignment with Nepal’s demographic reality is a silent but powerful enabler of this entire transition.

The Gravitational Pull of the Indian Palate

While the supply-side economics are compelling, the true engine of this boom is the insatiable and evolving demand from the south. The Indian market, with its 1.4 billion consumers and a rapidly expanding middle class, represents one of the single greatest commercial opportunities for Nepal. The strategy for kiwi and avocado is not to compete with India’s own vast agricultural output, but to service a premium, niche demand that India itself cannot easily meet. This is a classic case of exploiting a competitive advantage rooted in geography and climate, a concept we can term “agro-climatic arbitrage.”

Nepal’s mid-hills, with their temperate climate, cool winters, and well-drained soil, are ideal for growing fruits like kiwi, which require significant “chilling hours” that the hot, tropical plains of Uttar Pradesh, Bihar, and West Bengal cannot provide. Similarly, specific varieties of avocado, like the lucrative Hass, thrive in these sub-tropical highland conditions. India’s domestic production of these fruits is nascent and geographically limited, creating a massive supply-demand gap that is currently filled by expensive, long-distance imports from New Zealand, Chile, or Mexico. A container of kiwi from New Zealand takes weeks to reach an Indian consumer, incurring substantial costs in shipping, cold storage, and import tariffs. A truckload of kiwi from Dhankuta can reach Siliguri or Kolkata in less than two days.

This proximity is a game-changing strategic asset. It translates into a lower cost structure, a fresher product with a longer shelf life, and a more resilient supply chain, insulated from the vagaries of global shipping. For an Indian importer or supermarket chain, sourcing from Nepal is not just cheaper, it is faster and more reliable. The open border and the provisions within the South Asian Free Trade Area (SAFTA) framework, although imperfectly implemented, offer a preferential trade corridor that competitors from other continents cannot match. Seeing a “Product of Nepal” sticker on a kiwi in a Delhi supermarket is becoming a symbol of this powerful cross-border synergy. It represents a shift from competing with India on commodities to complementing its market with premium goods it desires but cannot produce at scale.

This dynamic places Nepalese producers in an enviable position. They are not price-takers in a flooded commodity market; they are price-setters in a supply-constrained premium market. The demand is not just for any fruit, but for produce associated with health, wellness, and aspirational lifestyles—a marketing narrative that resonates deeply with India’s urban, upwardly mobile consumers. The success of Bhutan in capturing a significant share of the Indian market for apples and cardamom serves as a powerful precedent. Bhutan leveraged its unique growing conditions and a strong “brand” of purity to dominate a niche. Nepal is now positioned to do the same, but with a different, and potentially even more lucrative, portfolio of fruits.

De-Risking Nature: The Rise of Ag-Tech and Patient Capital

Agriculture is inherently risky, subject to the whims of weather, pests, and disease. For traditional investors accustomed to the predictable cash flows of real estate or manufacturing, this volatility is a major deterrent. The “smart money” entering the high-value fruit sector is not ignoring these risks; it is systematically mitigating them through a combination of technology, financial structuring, and a portfolio-based approach. This marks a departure from the fatalism of traditional farming to the proactive risk management of modern agribusiness.

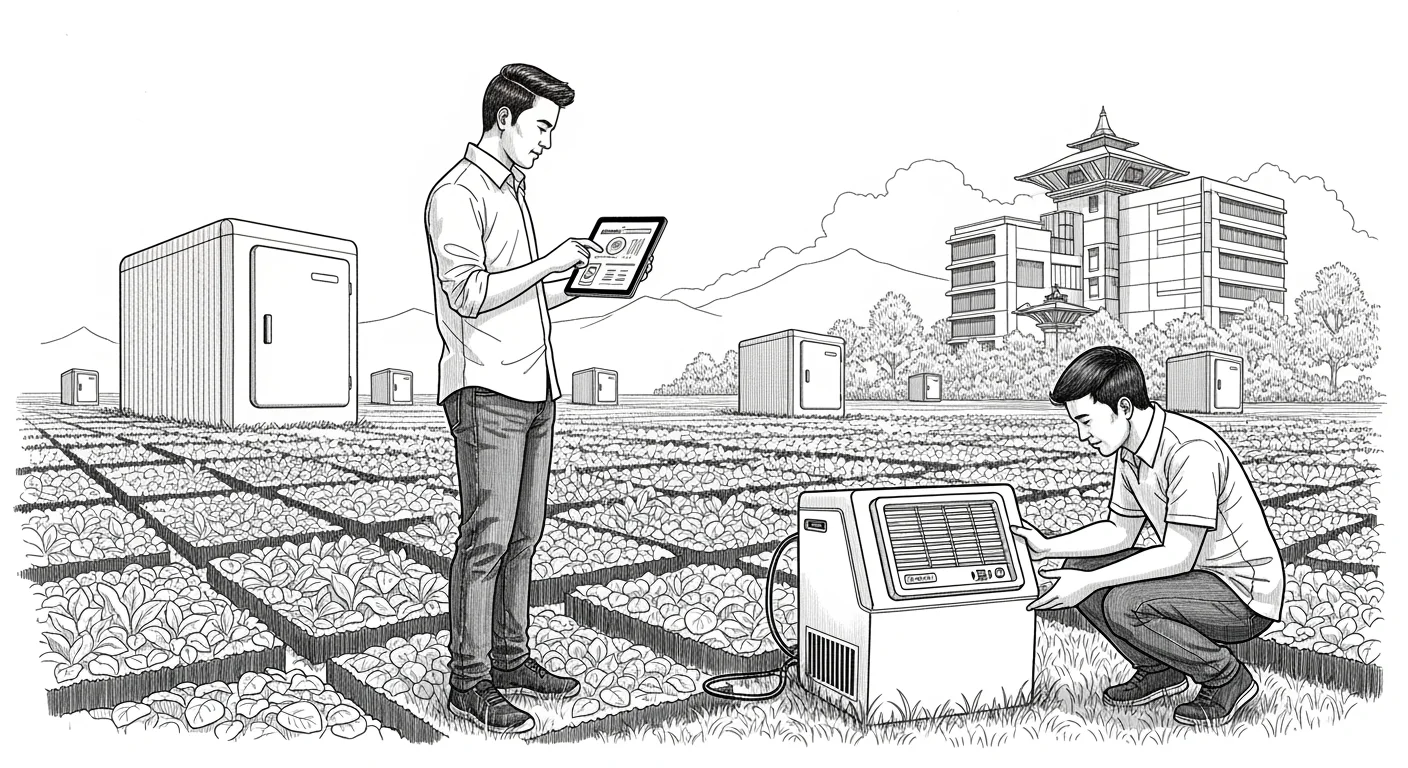

The first pillar of this de-risking strategy is the adoption of an “ag-tech stack.” Instead of relying on monsoon rains, commercial orchards are engineered with Israeli-designed drip irrigation systems, delivering precise amounts of water directly to the roots of each plant. This not only conserves a scarce resource but, more importantly, decouples the farm’s viability from the unpredictability of rainfall, neutralizing the threat of drought. Soil moisture sensors, automated weather stations, and drone-based monitoring provide a constant stream of data, allowing farm managers to move from reactive problem-solving to predictive intervention. Fertilizer and pesticide application becomes a precise science, driven by data on nutrient deficiencies and pest probability, rather than guesswork. Crucially, investors are paying premiums for tissue-cultured, disease-resistant saplings from certified national and international nurseries, ensuring genetic quality and higher survival rates from day one. This initial capital outlay on technology and superior genetics is an insurance premium against future failure.

The second pillar is the financial structure itself. This sector is not for speculators seeking a quick return. The ROI horizon is long and J-curved. An orchard requires significant upfront investment and will not generate meaningful revenue until years 5-7, only reaching peak profitability after a decade. This reality excludes traditional bank financing, which is typically short-term and collateral-based. Instead, the sector is being built with “patient capital”—investment from high-net-worth individuals, family offices, and private funds that understand the long game. These investors are not looking for a 2-year payback; they are looking to build an asset that will generate stable, annuity-like cash flows for 20-30 years. This alignment between the investment horizon and the crop’s natural lifecycle is fundamental to the sector’s current growth.

Finally, sophisticated players manage risk through portfolio diversification. They are not betting everything on a single 100-ropani farm in one location. They are building a portfolio of orchards spread across different districts and even provinces—a farm in Mustang, another in Dhankuta, perhaps a third in Kavre. This geographic diversification mitigates localized risks. A hailstorm in one valley will not wipe out the entire year’s potential revenue. A pest outbreak in one district can be contained without jeopardizing the entire enterprise. This portfolio approach, common in financial markets but revolutionary in Nepalese agriculture, transforms a series of high-risk individual projects into a single, moderate-risk, high-return investment platform.

The Strategic Outlook

The trajectory of Nepal’s high-value fruit sector is at a critical inflection point. The confluence of favorable economics, immense market pull, and new investment models has created a window of opportunity. The future, however, will be determined by how the ecosystem navigates the path from nascent boom to mature industry. Two distinct scenarios lie ahead.

In the most optimistic scenario, supportive policy acts as a powerful accelerant. If the government streamlines and digitizes land-leasing regulations, creating a transparent national registry of long-term agricultural leases, it would drastically reduce the friction and risk for investors. Paired with targeted public investment in farm-to-market roads, cold storage hubs at key collection points, and accredited quarantine labs at border crossings, this could unleash a torrent of domestic and foreign investment. The mid-hills could transform into a designated “Himalayan Fruit Belt,” creating tens of thousands of skilled rural jobs in horticulture, logistics, and food processing, and firmly establishing “Produce of Nepal” as a premium brand in the regional market.

Conversely, a scenario of stagnation and bust remains plausible. If bureaucratic inertia continues to plague land aggregation, and if critical infrastructure like cold chains and rural roads remains neglected, the sector will be confined to a handful of well-connected early movers. The entire industry remains highly vulnerable to a systemic shock, such as the arrival of an invasive pest like the South American fruit fly. Without a coordinated, rapid-response national plant protection framework, a single outbreak could devastate orchards across the country, vaporizing investor confidence for a generation. In this future, the promise of an agricultural revolution fizzles into a cautionary tale of squandered potential.

The Hard Truth: The most immediate and insidious threat to this burgeoning sector is not policy or pests, but the risk of its own success. The high profits of the pioneers will inevitably attract a wave of “copycat” investors and farmers, many of whom will lack the technical expertise, an ag-tech stack, or the patient capital required. They will plant cheaper, inferior-quality saplings, neglect proper soil management, and cut corners on orchard care. In five to seven years, this could lead to a glut of low-grade, inconsistent-quality fruit hitting the market simultaneously. This would not only crash domestic prices but, more disastrously, would erode the “Brand Nepal” reputation for quality in the crucial Indian export market before it is even fully established. The strategic race, therefore, is not just to plant more trees. It is to urgently establish and enforce national standards for quality, certification (e.g., “Nepal Good Agricultural Practices”), and branding. Without a robust quality assurance framework, the very forces driving the boom could sow the seeds of its collapse, turning a golden harvest into a bitter one for all.