Nepal, a developing country whose economy relies heavily on agriculture and remittances from migrant workers1, faces a range of economic challenges. Among them is moderate gross domestic product (GDP) growth, projected at 4.5% in fiscal year (FY) 2025.3, inflation pressure reached 6.05% in mid-December 20244, and a persistently large trade deficit.5In this context, the National Bank of Nepal (NBN), as the country’s central bank, plays a key role in maintaining macroeconomic stability. Its efforts are aimed at managing foreign exchange reserves, controlling inflation, and promoting economic growth through monetary policy.7

Foreign exchange reserves (FER) are vital for a developing economy like Nepal. They serve as a buffer against external economic shocks, provide credibility to the national currency, the Nepalese rupee, and ensure the country’s ability to finance imports, especially of critical items such as fuel, medicines, and industrial raw materials. Monetary policy, in turn, is the NRB’s primary tool for achieving price stability, managing liquidity levels in the economy, and influencing credit conditions to stimulate or, if necessary, restrain economic activity.

The objective of this study is to comprehensively analyze the current status of Nepal’s foreign exchange reserves, the latest monetary policy of the NRB adopted for FY2024/25, and assess how the central bank is trying to balance the often conflicting objectives of import control and domestic production promotion. The paper is structured to include an analysis of the foreign exchange reserves dynamics, a detailed discussion of key aspects of monetary policy, an assessment of its balancing role in the economy, and a discussion of the challenges and risks involved. The final section will present key findings and offer recommendations.

1. Status and Dynamics of Nepal’s Foreign Exchange Reserves

An analysis of Nepal’s foreign exchange reserves shows that they have grown significantly in recent years, providing a certain margin of safety for the country’s economy.

- Current volume, composition and trends of changes in international reserves

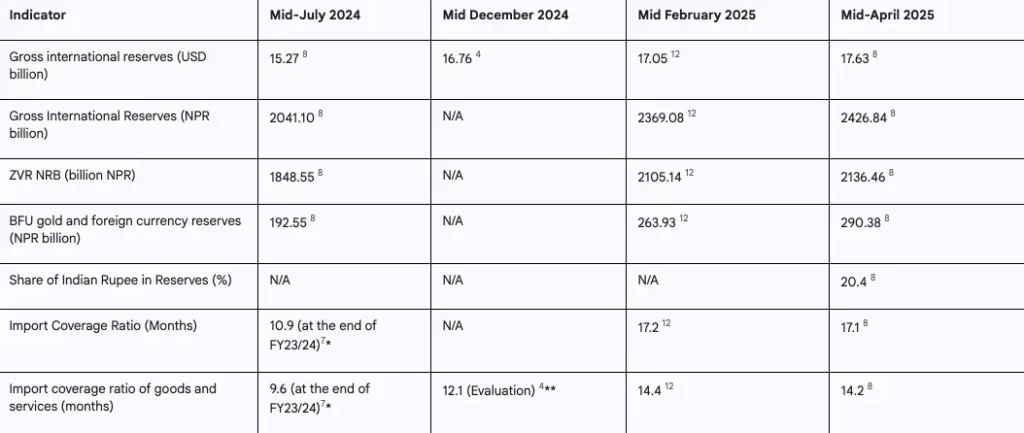

As of mid-April 2025, Nepal’s gross foreign exchange reserves reached US$ 17.63 billion.8 This represents an increase of 15.4% compared to US$ 15.27 billion in mid-July 2024.8 In domestic currency terms, the reserves increased to Nepalese Rupee (NPR) 2426.84 billion.8 The bulk of these reserves, NPR 2136.46 billion, were held directly by the NRB, while the reserves of commercial banks and other financial institutions (CFIs) amounted to NPR 290.38 billion. Importantly, the share of the Indian rupee in total reserves as of mid-April 2025 was 20.4%8, reflecting the country’s close economic ties with India.

Data from other sources confirm this trend, with some variability due to different reporting dates. For example, reserves were estimated at US$16.76 billion as of mid-December 20244,4 and at US$15.2 billion as of February 2025.10 Despite some volatility, the overall trend over FY2024/25 is towards increasing reserves.

- Reserve adequacy analysis

One of the key indicators of the adequacy of foreign exchange reserves is the import coverage ratio. As of mid-April 2025, Nepal’s banking sector foreign exchange reserves were sufficient to cover 17.1 months of projected imports of goods and 14.2 months of imports of goods and services.8These figures significantly exceed the traditionally considered safe level of 3-6 months and the target of the NRB itself, set in the monetary policy at the level of 7 months of import coverage.11Previously, as of mid-February 2025, these figures were 17.2 months for imports of goods and 14.4 months for imports of goods and services.12Such a high level of coverage indicates a comfortable situation with external liquidity at present.

- Key factors influencing the level of IVR

The dynamics of Nepal’s foreign exchange reserves are determined by several key factors:

- Money transfers: They are the dominant source of foreign exchange inflow. During the first nine months of FY2024/25 (mid-July 2024 to mid-April 2025), remittance inflows from Nepalese migrant workers working abroad increased by 10.0% year-on-year to reach NPR 1191.31 billion (equivalent to US$ 8.74 billion).8In 2022, remittances covered 56.6% of Nepal’s trade deficit and accounted for about a quarter of the country’s GDP.16The main source countries for these transfers have traditionally been the Gulf States and Malaysia.17

- Trade balance: Nepal has a structurally high trade deficit. In the first ten months of FY2024/25 (to mid-April 2025), the country’s trade deficit exceeded NPR 1.25 trillion.5The import volume during this period amounted to NPR 1474.1 billion, while exports amounted to only NPR 217.91 billion.5Despite the significant growth in exports (by 72.71% over the period), their volumes are still significantly lower than imports. Data for February 2025 also indicate a trade deficit of US$992.9 million.6

- Balance of Payments (BoP): Despite the large trade deficit, Nepal’s balance of payments remained in surplus, amounting to NPR 346.23 billion (US$2.55 billion) in the first nine months of FY24/25.8The current account of the balance of payments also showed a surplus of NPR 210.22 billion (US$1.55 billion).8This positive result is largely due to the high and stable inflow of remittances, which offset the negative trade balance.

- Capital movement: Net capital inflows amounted to NPR 7.71 billion during the first nine months of FY2024/25. Foreign direct investment (FDI), measured only in equity, reached NPR 8.96 billion during the same period.8

Table 1: Key Indicators of Nepal’s Foreign Exchange Reserves (2023-2025)

*Note: * Data as of mid-July 2024 (end of FY2023/24) from Monetary Policy 2024/25.

This table clearly demonstrates the positive dynamics and current high level of Nepal’s foreign exchange reserves, as well as their sufficiency to cover the country’s import needs.

Despite the current comfortable level of international reserves, their structure and sources of formation reveal certain vulnerabilities. High dependence on remittances makes Nepal’s economy sensitive to changes in countries receiving Nepali migrants, as well as to global economic and geopolitical factors that may affect the flows of these remittances. The decline in remittances observed in the first half of FY2024/25, due in particular to a reduction in the number of migrants going to Malaysia [18], is a reminder of such vulnerability. If the trade deficit, which requires significant financing, is not offset by sufficient remittance inflows, this could quickly lead to a deterioration in the state of international reserves and the balance of payments.

The export growth of 72.71% in FY24/25 over ten months [5] is certainly a positive sign. However, its base remains low compared to import volumes. The export-to-import ratio is around 1 to 6.7. Moreover, a significant portion of this growth is in relatively low-value-added products or even re-exports such as soybean oil and sunflower oil produced from imported feedstock. [1, 19, 20, 21] This indicates that the structural problems of Nepal’s exports, such as low diversification and lack of competitiveness of domestic production, persist. Increased exports of high-value-added domestically produced goods and services are needed to sustainably improve the trade balance and reduce dependence on external revenues.

In the context of reserve adequacy, the decision of the NRB, taken within the framework of the Monetary Policy (MP) for FY2024/25, to increase the limits on imports through telegraphic transfer (TT), as well as through documents against payment (DAP) and documents against acceptance (DAA) [7, 11], indicates that the central bank feels quite confident about the current level of gold and foreign exchange reserves. Such a decision may be aimed not so much at strict import control, but at stimulating economic activity by ensuring business access to necessary goods and raw materials, as well as supporting the fiscal needs of the government by increasing the collection of customs duties. Indeed, in a situation where the government is facing difficulties in mobilizing revenues, and customs revenues form a significant part of them [22, 23, 24, 25], facilitating imports can be seen as a way to replenish the treasury.[11] This reflects the difficult balance that the NRB is forced to maintain: using a comfortable level of gold and foreign exchange reserves to support other economic and fiscal goals, and not just to preserve them.

2. Review and Analysis of the NRB’s Latest Monetary Policy (for FY2024/25)

NRB Monetary Policy for the 2024/25 Financial Year, released on July 26, 20247, was formed in conditions of gradual economic recovery after previous shocks, but with the persistence of certain challenges.

- Main objectives of monetary policy for FY2024/25.

The main objective of the NRB, according to its mandate, is to maintain price stability and balance of payments stability to ensure sustainable economic development.7 For FY 2023/24, the inflation target was set at 6.5%.7 The actual average inflation for the eleven months of that year was 5.62%, and the annual inflation as of mid-June 2024 declined to 4.17%.7 However, by mid-December 2024, annual inflation accelerated again to 6.05%.4 The inflation forecast for 2025 is about 4.9%.

The fiscal year 2024/25 monetary policy was described as “cautiously accommodative” and aimed at stimulating production, job creation and a general revival of economic activity. The key quantitative target was to expand private sector lending by 12.5%.7 The policy is also intended to support the achievement of the 6% economic growth target set out in the government budget for fiscal year 2024/25.

- Key policy instruments.

To achieve its goals, the NRB uses a number of tools:

- Interest rates (interest rate corridor): Steps were taken to ease monetary conditions. The bank rate, which is the upper limit of the interest rate corridor, was reduced by 50 basis points (bp) to 6.5%.7The repo rate (the key policy rate) was also reduced by 50 bps to 5.0%.7At the same time, the overnight deposit rate, which serves as the lower limit of the corridor, was left unchanged at 3.0%.11These changes are aimed at reducing the cost of borrowing in the economy and stimulating the lending activity of banks.

- Reserve Requirement Ratios (CRR) and State Liquidity Ratios (SLR): These standards for banks were left unchanged.7This indicates that the NRB is currently not resorting to these instruments to directly influence the volume of liquidity in the banking system, preferring to act through interest rates.

- Open market operations: The NRB announced that it would continue to conduct automatic and rules-based open market operations in order to maintain the weighted average interbank interest rate close to the target level of the repo rate.7

- Interim (semi-annual) review of monetary policy (February 2025).

In February 2025, the NRB conducted a semi-annual review of the DCT, based on the results of which some adjustments were made:

- Key interest rates (bank, repo and deposit) were maintained at the previous level: policy rate – 5%, deposit rate – 3%, bank rate – 6.5%.28

- One of the significant changes was reduction of the loan loss provision for good loans from 1.10% to 1.0%.28 The rationale for the move is said to be the need to help banks increase profitability and make it easier to manage growing volumes of problem loans. The move could free up some of the banks’ capital, which could be used for lending or to improve their financial performance.

- Changes were made to the regulation of car loans: a single maximum Loan-to-Value (LTV) ratio has been set at 60% for personal cars, including all types of electric vehicles (EVs). Previously, more favorable conditions were in place for electric vehicles, and LTV could reach 80%.28While no clear rationale for the change is given, it may be related to concerns about rising car imports or an assessment of credit risks in the segment.

- It was also announced that microfinance organisations will be required to set interest rates on their loans based on the base rate from May/June 2025, which is aimed at ensuring fairer pricing for borrowers.29The NRB said the measures are intended to support the expansion of economic activity and help achieve the government’s economic growth targets.28

Table 2: Main instruments and targets of the NRB monetary policy for FY2024/25

This table summarizes the key parameters of the monetary policy, reflecting its easing direction and the adjustments made during the financial year.

The NRB’s monetary easing comes amid rising non-performing loans (NPLs), which reached 4.0% by April 2024 [30] and 4.9% by the end of the first half of FY2024/25.[18] The International Monetary Fund (IMF) has previously advised Nepal to maintain a prudent monetary policy and has drawn attention to the vulnerabilities of the financial sector.[31] In this context, the NRB’s moves to cut interest rates and reserve requirements for good loans [28, 29] may indicate that in the current environment, priority is given to stimulating economic growth, the target of which the government has set at 6% [27], even if this is associated with some increase in risks to financial stability. Such a decision may be dictated by the need to revive the economy after a period of slow growth (1.95% in FY2022/23 [32]) or the NRB’s assessment that the existing risks are manageable.

The change in the LTV ratio for car loans, especially the tightening of conditions for electric vehicles (reduction from 80% to 60%) [28, 29], looks like a step that may be aimed at curbing the growth of imports of consumer durables. Cars, including electric vehicles, are a significant import item. Reducing the LTV makes buying a car on credit less affordable, which could potentially reduce demand for them and, accordingly, import volumes. This decision may also be associated with an attempt by the NRB to redirect limited credit resources to more productive sectors of the economy or with credit risk management, if there was an increase in overdue debt on car loans.

The NRB’s stated target of 12.5% private sector lending growth in FY2024/25 [7, 27] may prove difficult to achieve. Despite lower interest rates and excess liquidity in the banking system [27], actual private sector lending growth was moderate, amounting to 8.3% year-on-year as of mid-April 2025. [8] High NPL levels force banks to be more cautious in issuing new loans and focus on repaying existing problem loans. [23, 33] In addition, business demand for loans may remain low due to overall economic uncertainty and the slow pace of economic recovery. [18] Thus, achieving the target lending growth will require a significant improvement in the business environment and a reduction in credit risks.

3. Balancing Import Controls and Domestic Production Promotion

The National Bank of Nepal faces a delicate balance in its monetary policy between maintaining adequate levels of foreign exchange reserves, which often requires import controls, and creating conditions for domestic production growth, which involves stimulating lending and investment.

3.1. NRB policy in the field of import management

- Currency control measures for import operations.

In the FY2024/25 Monetary Policy, the NRB has taken steps that can be interpreted as easing rather than tightening import procedures. Specifically, the limit for import of goods through Draft/Telegraphic Transfer (TT) has been increased from US$ 35,000 to US$ 50,000. Similarly, the limit for import through Documents Against Payment (DAP) and Documents Against Acceptance (DAA) has been increased from US$ 60,000 to US$ 100,000.7 Additionally, for government procurement under the Public Procurement Law, the foreign exchange transaction limit for payment through Draft/TT has been abolished and multiple modes of payment have been allowed.7 The list of goods for which back-to-back letters of credit can be provided has also been expanded, in line with the Nepal Trade Integration Strategy.7

These measures, taken against the backdrop of a fairly high level of gold and foreign exchange reserves, are probably aimed at ensuring an uninterrupted supply of the domestic market with necessary goods and raw materials, supporting economic activity and, possibly, increasing government revenues from import duties, which is indirectly confirmed by statements about the need to collect revenues through import taxation.

- Assessing the impact of these measures on import volumes, trade deficit and the state of international reserves.

External trade data show a mixed picture. Total merchandise imports for the eleven months of FY23/24 fell by 1.8% to NPR 1,453.70 billion.7However, in the first ten months of the current 2024/25 fiscal year, imports, on the contrary, grew by 13.11%.5In its forecast for 2024/25 FG, the NRB expects positive dynamics of import growth, linking this to lower interest rates, available liquidity, the government’s plans for capital expenditures and economic growth targets.7Such growth in imports, in turn, may lead to some slowdown in the growth rate of international reserves.7Nepal’s trade deficit remains structurally high5, and easing import procedures can help maintain it or even increase it if export growth does not significantly outpace import growth.

- The role of customs duties in budget revenues and their indirect impact on imports.

Nepal’s government budget relies heavily on import-related revenue. Customs revenue, which includes import duties, excise duties on imported goods, and VAT levied on imports, accounted for about 40% (39.71% to be precise) of the total government revenue in FY23/24, reaching NPR 420.16 billion.23 More broadly, customs revenue accounts for about 44% of total government revenue and 50% of total tax revenue, with customs duties directly accounting for 20% of tax revenue.

This high fiscal dependence on imports creates a difficult dilemma for the authorities: any measures to significantly restrict imports, aimed at protecting gold and foreign currency reserves or stimulating domestic production, will inevitably lead to a reduction in budget revenues. In this context, the easing of some import restrictions by the NRB 11 can be seen as an attempt to support fiscal revenues, especially in conditions when gold and foreign currency reserves are at a comfortable level.

3.2. Policy of the NRB to stimulate domestic production

In parallel with import management, the NRB is implementing measures aimed at supporting and stimulating various sectors of the domestic economy.

- Targets for lending to priority sectors.

The FY2024/25 DCP envisages a revision of the existing credit limit of NPR 10 million for micro, cottage, small and medium enterprises (MCMEs). It also plans to revise the provision that the premium on the base interest rate for loans up to NPR 20 million for MCMEs should not exceed 2.0%. This revision will include expanding the list of sectors eligible for concessional terms to include industries related to domestic production such as agricultural ancillary industries, farm tool manufacturing, information technology and tourism.7

Statistics show that as of mid-June 2024, Nepal’s commercial banks allocated 13.2% of their total loans (NPR 582.49 billion) to the agriculture sector. The share of the power sector was 7.9% (NPR 350.74 billion), and the MSP sector was 9.2% (NPR 407.28 billion).7 Data as of mid-April 2025 shows that lending to manufacturing increased by 9.6% and to the construction sector by 11.4% during the period under review.

- Mechanisms for preferential lending and refinancing.

Monetary policy includes a number of measures to facilitate access to financing for specific categories of borrowers and sectors:

- Facilitating access to credit to stimulate youth entrepreneurship.7

- Introducing a mechanism to provide unsecured loans to individuals holding work permits abroad, with the guarantee of transferring remittances to their bank accounts in Nepal.7

- Simplification of procedures for lending secured by certain agricultural products.7

- Assistance in obtaining loans for education in specialties in demand on the domestic market, such as medicine, engineering, information technology and accounting.7

- To support the construction sector, which is experiencing a decline, special measures are envisaged: extension of the terms of repayment of the principal amount of debt and interest on loans until mid-December 2024; temporary moratorium on the inclusion of construction companies in the “black list” solely on the basis of unpaid checks; special conditions on the limits of off-balance sheet liabilities (guarantees) for construction companies.7

- Analysis of the dynamics of lending to the private sector and its sectoral structure.

In the first nine months of FY24/25, private sector lending by BFIs increased by 7.1%, or NPR 361.03 billion.8 In annual terms, the growth was 8.3% as of mid-April 2025.8 This growth rate is below the monetary policy target of 12.5%.7

An analysis of the collateral structure of BFI loans shows that 14.6% of total loans are secured against current assets (including agricultural and non-agricultural products), while 65.2% of loans are secured against land and buildings.8 This structure may indicate that a significant portion of lending continues to be channelled into real estate and trade-related sectors rather than directly into productive sectors, a long-standing problem in Nepal.

- The problem of non-performing loans (NPL) and its impact on the lending activity of banks.

The asset quality of Nepal’s banking system is a major concern. The non-performing loans (NPL) ratio of commercial banks has shown an alarming upward trend, increasing from 1.3% in June 2022 to 4.0% by April 202430 and reaching a record 4.9% by the end of H1 FY2024/25 (mid-December 2024).18

The NRB and the IMF recognize the rising NPLs as a key vulnerability of Nepal’s financial system and a serious challenge to its stability.21 High NPLs force banks to make significant loan loss provisions, reducing their profitability and limiting their ability to extend new loans. Banks are becoming more conservative in their lending policies, especially towards riskier productive sectors. The reduction in the provisioning ratio for “good” loans undertaken by the NRB in the mid-year Monetary Policy Review 28 is an attempt to alleviate this pressure on the banking sector.

- The Impact of Remittances on Domestic Demand, Inflation and Competitiveness (Dutch Disease).

The large and sustained inflow of remittances, which constitute about 21-25% of Nepal’s GDP16 and are the main source of income for more than half of households38, has a multifaceted impact on the economy. These funds are predominantly spent on consumption16, including imported goods, which maintains high demand for imports and contributes to the persistence of the trade deficit.

This situation creates risks of developing symptoms of “Dutch disease”, which include:

- Reduced competitiveness of sectors producing traded goods (agriculture, industry). This may occur due to the strengthening of the real exchange rate of the national currency (although there are no direct indications of its significant strengthening in the materials provided, high dependence on imports is an indirect sign) and/or the growth of domestic costs.

- The flow of resources, primarily labor, from manufacturing sectors to services and non-manufacturing activities financed by remittances. It is noted that Nepal’s agriculture suffers from labor shortages, one of the reasons for which is mass labor migration.40

- The outpacing growth of the services sector, whose share in Nepal’s GDP reached 62.90% in FY2023/24.32This growth may be partly due to domestic demand generated by remittances.

- Underinvestment in productive sectors, as capital can be directed to faster-return sectors related to consumption and imports, as well as real estate.37Academic research confirms some of these symptoms in Nepal, pointing out that the influx of remittances and foreign aid can have a negative impact on output in the primary (agriculture, mining) and secondary (industry) sectors, while stimulating growth in the services sector, which is characteristic of the “Dutch disease”.39Other studies show that while remittances have a positive impact on household spending on food, education and health, they do not always support investment in productive assets.16

Table 3: Trends of lending to Nepal economy by sectors and NPL level (2023-2025)

*Note: Data on the sectoral structure of BFU loans as of mid-April 2025 are presented as growth rates for the period, rather than absolute values or shares.

This table allows us to assess how successfully the NRB directs credit resources to priority production sectors and how this dynamic is affected by overall credit activity and the quality of banking assets.

3.3. Evaluation of the effectiveness of the balancing policy of the NRB

Analysis of successes and failures in achieving set goals.

The NRB has achieved some successes in its activities, but has also faced serious challenges. Successes include maintaining a high level of gold and foreign exchange reserves and overall balance of payments stability, which is ensured mainly by a significant inflow of remittances.4 It has also managed to keep inflation close to target levels in certain periods, although its recent rise to 6.05% as of mid-December 2024 is a cause for concern.

Among the setbacks and remaining challenges is the sluggish growth of private sector credit despite monetary easing measures.8 The sharp rise in non-performing loans (NPLs) to record levels of 18 poses a serious threat to financial stability. The economy remains highly dependent on imports and remittances, and progress in stimulating diversified domestic production and competitive exports remains slow.2 Government programmes aimed at modernising key sectors, such as the Prime Minister’s Agricultural Modernisation Project (PMAMP), have yet to yield the tangible results expected.

The view of international financial organizations on the policy of the NRB

The IMF generally supports the NRB’s efforts but recommends continuing to pursue a prudent and data-driven monetary policy to maintain price and external stability. The Fund emphasizes the importance of amending the NRB Law to strengthen its governance, independence, and accountability. The IMF also calls for a proactive approach to addressing growing vulnerabilities in the financial sector, including aligning the regulatory framework with international standards, conducting a planned review of banks’ loan portfolios, and developing a comprehensive strategy to resolve distressed savings and credit cooperatives. The IMF identifies weak capital expenditure execution, financial sector vulnerabilities, and political instability as key risks to Nepal’s economy.

The World Bank projects Nepal’s economy to continue to grow at a robust pace (4.5% in FY25 and averaging 5.4% in FY26-27), driven primarily by domestic trade, hydropower development, and rising rice production.3 However, the Bank also points to significant risks associated with global geopolitical uncertainty, potential asset quality deterioration in Nepal’s financial sector, policy inconsistency due to frequent bureaucratic reshuffles, and delays in capital budget execution.3 The World Bank emphasizes the critical importance of stimulating private sector growth to create jobs and the need for structural reforms.

Position of the Nepalese business community.

Nepal’s private sector representatives, particularly the Federation of Nepal Chambers of Commerce and Industry (FNCCI) and the Confederation of Nepal Industries (CNI), have generally welcomed the monetary easing for FY2024/25, viewing it as “accommodative” and aimed at stimulating economic activity after two years of tight measures.27Positive changes were noted for contractors and MSMEs.27At the same time, some experts expressed concern about the possible compromise on financial sector stability due to the relaxation of certain prudential rules, such as those related to credit loss provisions.27FNCCI consistently emphasizes the importance of constructive public-private dialogue to implement economic reforms and improve the investment climate in the country.44

The analysis of the balancing policy of the NRB reveals deep interrelations and dilemmas. One of them is the contradiction between the need to replenish the state budget and the desire to control imports. The high dependence of the budget on customs duties23means that import restrictions to preserve gold and foreign currency reserves or support local producers directly reduce treasury revenues. Easing import restrictions in the 2024/25 DCT7against the backdrop of high gold and foreign exchange reserves can be interpreted as an attempt to support fiscal revenues and economic activity, even if this leads to some increase in imports. Thus, the NRB balances not only between import control and production stimulation, but also indirectly between import control and the government’s fiscal sustainability.

Another difficult point is the risk of a “liquidity trap” and the insufficient effectiveness of monetary policy to stimulate the real sector. Despite the reduction in interest rates and the presence of excess liquidity in the banking system27, credit growth in manufacturing sectors remains sluggish and NPL levels are rising. This may indicate that Nepal’s domestic production problems have deeper roots than just credit availability. These include structural problems in agriculture and industry, an unfavorable investment climate, shortages of skilled labor, and infrastructure constraints.45In such circumstances, simply lowering rates may not lead to the desired growth of investment in the real sector. The effectiveness of monetary policy in stimulating domestic production is limited without addressing these fundamental structural problems.

Finally, the phenomenon of “Dutch disease” poses a systemic challenge to the NRB’s efforts to balance. A large and sustained inflow of remittances, while supporting foreign exchange reserves and domestic consumption, can simultaneously undermine the competitiveness of domestic production, especially in agriculture and industry, and complicate efforts to stimulate it.37The NRB’s policy of making credit cheaper for productive sectors may not be sufficient to overcome this structural distortion if profitability in these sectors is low due to import competition and other problems exacerbated by the effects of the “Dutch disease”. Thus, the NRB’s task is not simply the technical management of imports and credit, but counteracting deep structural distortions in the economy.

4. Key Challenges and Risks to Monetary Stability and Economy of Nepal

Despite some success in macroeconomic stabilization, Nepal faces a number of serious challenges and risks that may affect its monetary stability and economic development.

- Inflation risks and managing expectations.

Recent acceleration of inflation to 6.05% (annualized as of mid-December 2024)4, particularly noticeable in the food segment (up 9.99%), where vegetable prices jumped by 43.05%4, poses a significant challenge. The easing of monetary policy and the expected growth in credit could increase inflationary pressures if aggregate supply growth, that is, domestic production, lags aggregate demand growth. In addition, Nepal’s high dependence on imports, including food and energy, makes the economy vulnerable to global inflation and exchange rate fluctuations.

- Vulnerabilities of the financial sector.

The asset quality of the banking system is a major concern, with the sharp rise in the non-performing loans (NPL) ratio to 4.9% by the end of the first half of FY24/25.18is an alarming signal. Both the NRB and the IMF point to this as one of the key vulnerabilities of the financial system.21The deterioration in asset quality is putting pressure on banks’ capital adequacy ratios, although on average they remain above regulatory minimums (for example, the average capital adequacy ratio of commercial banks was 12.84% at the end of FY23/24).33). Reduction of the reserve ratio for “good” loans28may temporarily improve banks’ financial performance, but does not address the fundamental problem of their asset quality. Additional risks to financial stability create problems in the savings and credit cooperative sector.31Nepal’s inclusion in the FATF grey list also requires the authorities to take urgent and effective measures to strengthen its anti-money laundering and counter-terrorism financing (AML/CFT) system.31

- High dependence of the economy on external factors.

Nepal’s economy remains highly dependent on external conditions:

- Money transfers: As has been noted many times, their reduction can seriously affect the state of the international reserves, the balance of payments, the level of domestic demand and social stability in the country.18

- World prices for raw materials: Being a net importer of oil and many other commodities, Nepal is sensitive to fluctuations in world prices of these resources.

- Geopolitical and trade uncertainty: The World Bank highlights these factors as key external risks to the Nepalese economy.3

- Structural constraints on growth of domestic production and exports.

Efforts to stimulate domestic production and exports run into a number of deep structural problems:

- Low agricultural productivity due to the prevalence of traditional farming methods, lack of irrigation systems, poor mechanization, and problems with farmers’ access to quality seeds and fertilizers.2

- A high degree of fragmentation of land holdings makes it difficult to apply modern agricultural technologies and commercialize agriculture.48

- Underdevelopment of the industrial sector and lack of basic infrastructure, including energy capacity and transport networks.40

- A challenging investment climate characterized by bureaucratic red tape, corruption, political instability and frequent changes in government policy.2

- A shortage of skilled labour in many sectors, exacerbated by the mass labour migration of young people abroad.40

- Problems with the effectiveness of government support programs such as PMAMP40, and subsidy distribution systems that often fail to reach the real producers in need.73

Rising levels of non-performing loans (NPLs) constrain banks’ willingness to lend to the economy, especially for riskier manufacturing projects. This, in turn, dampens investment activity and economic growth. Monetary easing by the NRB may not have the desired effect if banks are preoccupied with cleaning up their balance sheets and do not see enough quality borrowers in the market. A vicious circle may thus arise where slow economic growth exacerbates the NPL problem and high NPLs impede economic growth. Nepal’s high dependence of the government budget on import duties may exert subtle but significant pressure on the NRB in making decisions on foreign exchange control measures. The government’s need for stable fiscal revenues may limit the central bank’s room to maneuver in tightening import restrictions, even if such measures would be advisable from the standpoint of managing foreign exchange reserves or promoting import substitution. This phenomenon can be described as “fiscal dominance” of monetary policy, where fiscal considerations override monetary decisions. The analysis shows that monetary policy alone, whether through interest rate cuts or targeted lending programs, has limited effectiveness in stimulating sustainable growth in domestic output in Nepal. This is due to the deep structural problems listed above. Without comprehensive structural reforms in agriculture, improvement of the investment climate, infrastructure development, and human capital development, the NRB’s efforts are likely to have only temporary or marginal effects. For monetary policy to be more effective in stimulating domestic output, a coordinated government effort to undertake broad structural reforms is needed, as has been repeatedly pointed out by both the IMF and the World Bank.3

5. Conclusion and Recommendations

The conducted analysis of the status of Nepal’s foreign exchange reserves and the latest monetary policy of the National Bank of Nepal (NBN) allows us to draw a number of key conclusions and formulate recommendations.

- The main conclusions of the analysis.

Nepal’s foreign exchange reserves are currently at a relatively high level, providing a significant cushion to cover the country’s import needs. However, their stability largely depends on the continued inflow of remittances from migrant workers, creating some vulnerability to external shocks.

The monetary policy of the NRB for the 2024/25 financial year is characterized by easing with the main goal of stimulating economic growth. This is manifested in the reduction of key interest rates and some regulatory relaxations for the banking sector. At the same time, such a policy is implemented against the backdrop of significant risks, the main ones being the growth of non-performing loans (NPL) in the banking system and the potential increase in inflationary pressure.

The NRB has been making efforts to balance the objectives of import control and domestic production promotion. However, the effectiveness of this balancing policy is limited by deep structural problems of the Nepalese economy, such as high dependence on imports and remittances, low productivity and competitiveness of domestic industries, and dilemmas related to fiscal dependence on import duties and potential Dutch disease.

- Recommendations for NRB.

To enhance the effectiveness of monetary policy in achieving balanced economic development while maintaining macroeconomic stability, the following steps can be recommended to the National Bank of Nepal:

- Strengthening risk-based supervision of the financial sector: With NPLs rising and monetary policy easing, it is critical to ensure stricter and more proactive supervision of banks’ asset quality and lending practices. The IMF’s planned comprehensive review of the banking system’s loan portfolio should be carried out31to identify systemic risks and develop measures to mitigate them.

- Application of a differentiated approach to import control: Instead of general restrictions that could negatively affect economic activity, it would be appropriate to consider using more targeted measures. Such measures could be aimed at limiting imports of non-critical consumer goods, while facilitating the import of raw materials, components and equipment needed to develop domestic production and export-oriented industries. This requires close coordination with the government’s fiscal policy.

- Development and implementation of a strategy to mitigate the negative effects of the “Dutch disease”: Given the significant impact of remittances on the economy, measures are needed to sterilize part of the excess foreign exchange earnings, create incentives for investing remittances in productive assets (and not just in consumption and real estate), and implement programs to improve the competitiveness of tradable sectors of the economy, primarily agriculture and industry.

- Improving mechanisms for targeted lending: It is important to ensure that soft loans and other support measures actually reach small and medium-sized manufacturing enterprises and are not diverted to other, lower-priority sectors. Monitoring of the effectiveness of such programmes should be strengthened and the impact of major initiatives such as the Prime Minister’s Agricultural Modernisation Project (PMAMP) should be reviewed.40, with the aim of optimizing them.

- Increasing the transparency and predictability of monetary policy: Clear and consistent communication by the NRB regarding policy objectives, risk assessment and rationale for decisions taken is critical to building trust among economic agents and effectively managing inflation expectations.

- Strengthening the institutional independence of the NRB: In accordance with the IMF recommendations, it is advisable to continue work on amending the Law on the NRB, aimed at strengthening its operational independence, accountability and improving corporate governance.31

- Forecast estimates.

In the short term, Nepal’s foreign exchange reserves are likely to remain adequate, provided current levels of remittance inflows are maintained. However, to ensure long-term stability of foreign exchange reserves and reduce the economy’s external vulnerability, it is necessary to diversify sources of foreign exchange earnings, primarily by increasing exports of high-value-added goods and services (e.g., information technology, tourism, niche agricultural products48) and attracting sustainable flows of foreign direct investment.

Inflation may remain a challenge for the NRB, especially amid the easing of monetary policy and continued dependence on imports. The IMF’s inflation forecast for 2024/25 is around 5.5%.30

Nepal’s economic growth could accelerate in FY2024/25 (various forecasts range from 4.5% to 5% 3). However, achieving sustained and high rates of economic growth that can significantly improve living standards will require addressing deep structural problems and implementing comprehensive reforms.

Clearly, the short-term stability of foreign exchange reserves, largely secured by remittances, should not lead to complacency. The NRB, together with the government, should formulate and consistently implement a long-term strategy aimed at strengthening the country’s export potential and attracting productive investment. This will reduce dependence on unstable external sources of financing and improve the overall resilience of the Nepalese economy.

The key to achieving balanced economic development is close coordination of the NRB’s monetary policy with the government’s fiscal and structural policies. The central bank’s efforts to stimulate domestic production or control imports will have limited impact without corresponding support from the government in the form of improving the investment climate, developing the necessary infrastructure, implementing reforms in the agricultural sector, increasing the efficiency of public expenditure, and diversifying sources of government revenue. Only a comprehensive and coordinated approach will enable Nepal to overcome the existing challenges and achieve sustainable and inclusive growth.

Source used

- agriculture – Investment Board Nepal

- Economy of Nepal – Wikipedia

- Nepal’s Economy Expected to Remain Resilient in Face of …

- Current Macroeconomic and Financial Situation – English (Based on Five Months Data of 2024/25) – Nepal Rastra Bank

- Nepal’s Foreign Trade Reaches Rs 1692 Billion in 10 Months of FY 2024/25 – ShareSansar

- Nepal Trade Balance [Up-to-date Chart & Data] | 1974 – 2025 – CEIC

- Monetary Policy for 2024/25 – Nepal Rastra Bank

- Current Macroeconomic and Financial Situation – English (Based on Nine Months Data of 2024/25) – Nepal Rastra Bank

- Rs. 1,191 billion remittance received in nine months – The Rising Nepal

- Nepal Foreign Exchange Reserves, 2002 – 2025 | CEIC Data

- Key Highlights of Nepal’s Monetary Policy for FY 2024/25 – Nepal Economic Forum

- Current Macroeconomic and Financial Situation – English (Based on Seven Months Data of 2024/25) – Nepal Rastra Bank

- Nepal Receives remittances over 1,191 billion in nine months | New Spotlight Magazine

- Nepal records Rs 7.42 billion in remittance outflow in the first nine months – CESLAM

- Current Macroeconomic and Financial Situation of Nepal

- The Role of Remittances in Household Spending in Rural Nepal – MDPI

- Trends and Destinations of Foreign Labour Migration in Nepal

- Nepal Development Update, April 2025 – World Bank

- Nepal’s agricultural trade within BIMSTEC – Sawtee

- Nepal’s exports surge by 57% – The Rising Nepal

- In-Depth Analysis of the Economic Situation & Business Opportunities in Nepal. Forecast 2025-2030

- The Relation of Direct and Indirect Taxes on Government Revenue collection of Nepal

- Customs revenue accounts for 40 percent of Nepal’s total revenue in FY 2023/24

- Government of Nepal Ministry of Finance Fiscal Policy Statement for Fiscal Year 2023/24 I. Introduction 1. Budget for fiscal y

- Revenue shocks & fiscal response – The HRM Nepal

- Nepal Inflation Rate Outlook, Average Consumer Prices (I:NIRA5NJM) – YCharts

- Accommodative Monetary Policy to spur the economy – The HRM Nepal

- Monetary policy mid-term review: policy rates maintained at 5 pc, vehicle loan ratio lowered to 60 pc – Business 360°

- NRB unveils mid-term monetary policy review, Slashes loan …

- Nepal: Fourth Review Under the Extended Credit Facility Arrangement-Press Release; Staff Report; and Statement by the Executive Director for Nepal in: IMF Staff Country Reports Volume 2024 Issue 225 (2024) – IMF eLibrary

- IMF Executive Board Completes the Fifth Review under the …

- Current Macroeconomic and Financial Situation of Nepal – Nepal Rastra Bank

- Increasing NPL and accumulation of non-banking assets are major challenges of banks: NRB – myRepublica

- Nepal Rastra Bank, Financial Stability Report 2024

- Nepal Non Performing Loans Ratio, 2003 – 2024 | CEIC Data

- Financial Institutions Supervision Report – 2023/24 – Nepal Rastra Bank

- Remittance inflows pose Dutch Disease risk in Nepalese economy – CESLAM

- An Analysis of Causal Relationship between Remittances and Imports in Nepal

- Symptoms of Dutch Disease in Nepal

- Modernising Agriculture – The Rising Nepal

- Export and Import of Food Products in Nepal (Rs Billion) – ResearchGate

- 107 billion rupees spent on agricultural subsidy in five fiscal years | The Farsight Nepal

- Nepal: World Bank Group’s New Country Partnership Framework Prioritizes Jobs and Resilience

- NIES:-Nepal International Economic Summit 2025 – FNCCI

- (PDF) COMMERCIALIZATION OF AGRICULTURE: FORMS …

- Why Nepal Struggles to Adopt Better Technology, And Alternative Routes to Development

- A homegrown vision of commercial agriculture in Nepal that puts small-scale farmers at its heart | International Institute for Environment and Development

- sectoral profile – agriculture – Investment Board Nepal

- Nepal Production – International Production Assessment Division (IPAD)

- Revolutionizing Agriculture in Nepal with Modern Technology – Living CARE

- statistical information on nepalese agriculture, 2079/80 [2022/23]

- Assess the Adoption of Improved Maize Production Technologies in Gulmi, Nepal

- Assessment of Maize Production and Adoption of Improved Maize Seeds in Tanahun District of Nepal – International Journal of Applied Sciences and Biotechnology (IJASBT)

- An overview of agricultural mechanization in Nepal – Kathmandu University Open Journal Systems

- Agricultural Mechanization in Nepal – IFPRI South Asia

- Irrigation Farming in Nepal – The Borgen Project

- Effect of irrigation canal conveyance efficiency enhancement on …

- (PDF) Impact of Irrigation Method on Water Use Efficiency and Productivity of Fodder Crops in Nepal – ResearchGate

- Modern Technology and Scope of Precision Agriculture (PA) – International Journal of Social Sciences and Management (IJSSM)

- Effect of Adopting Agricultural Technology on Farm Income of …

- Effect of Adopting Agricultural Technology on Farm Income of Commercial Vegetable Growers in Bagamati Province of Nepal – ResearchGate

- ADOPTION OF RIVERBED FARMING TECHNOLOGIES IN KAMALA …

- (PDF) Constraints on the use and adoption of information and communication technology (ICT) tools and farm machinery by paddy farmers in Nepal – ResearchGate

- Visualising adoption processes through a stepwise framework: A case study of mechanisation on the Nepal Terai – PubMed Central

- Nepal still awaits chemical fertilizer factory after four decades of delay – myRepublica

- Situation Report on Nepal’s Agrifood Systems June 2024 | Bulletin Number 19

- Status of fertilizer and seed subsidy in Nepal: review and recommendation

- Status of fertilizer and seed subsidy in Nepal: review and …

- Does subsidizing seed help farmers? Nepal’s rice seed subsidies | Request PDF – ResearchGate

- Nepal – Food and Agriculture Organization of the United Nations

- angoc.org

- Land Tenure and Taxation in Nepal – Pahar

- When Help Hurts – GMC Nepal

- Does Subsidizing Seed Help Farmers? Pulte Study Examines Nepal’s Rice Seed Subsidies

- Relationship between Agriculture Subsidy and Agricultural Production in Nepal. – Nepal Journals Online

- Minister Adhikari claims Rs107.66 billion in agricultural subsidies over five years

- agricultural support policy of nepal: cases of subsidies – International …

- FinMin Presents Economic Survey, Projects 4.61pc growth for current FY

- Nepal expects 4.61-pct growth for 2024-25 – Xinhua