The evolution of banking in Nepal, like many countries around the world, is characterized by a rapid shift from traditional service models to digital technologies. The introduction of mobile and internet banking, the rise of digital wallets and QR payments are dramatically changing customer expectations and the operating environment for financial institutions.1The concept of “Digital First” is becoming not just a trend but a new reality, forcing banks to rethink the role and functions of their physical branches. However, it is important to understand that “Digital First” does not always mean “Digital Only”, especially in the context of Nepal with its unique socio-economic and cultural characteristics.

Nepalese banks face a difficult dilemma: on the one hand, the need to reduce operational costs and follow global digitalization trends dictate the optimization and even reduction of branch networks. On the other hand, maintaining a physical presence remains critical to serve certain customer segments, provide sophisticated products, and maintain trust and loyalty in a culture where personal relationships play a significant role.4

This study aims to comprehensively analyze the current relevance and necessity of physical bank branches for Nepalese customers in the context of rapid digitalization. The main objectives include assessing the changing customer needs, analyzing the status and challenges of the existing branch network, and developing strategies for transforming physical branches to maintain customer loyalty and ensure profitability of banking business in Nepal. The study will review global and local trends in branch transformation, including smart branch and phygital approaches, and offer practical recommendations for the banking sector in the country.

The report is structured to cover key aspects of the issue in a sequential manner. Chapter one will analyze the profile of the Nepalese banking customer in the digital era, their needs and expectations. Chapter two will focus on the current status and challenges of the physical banking network. Chapter three will propose specific strategies for branch transformation. Chapter four will look at how transformation can help maintain loyalty and ensure profitability. Finally, Chapter five will formulate recommendations for the Nepalese banking sector and conclude with a summary of the findings.

Nepali Banking Customer in the Digital Age

Penetration and Usage of Digital Banking Services in Nepal

Nepal has shown significant progress in adopting digital banking technologies, which is fundamentally changing the financial services landscape in the country. In recent years, there has been a steady increase in the number of users of various digital channels.

Statistics and dynamics:

As of March 2025, the number of mobile banking users in Nepal has exceeded 27 million 7 , demonstrating the widespread reach of this channel. As recently as 2024, the Nepal Central Bank (NRB) reported over 9 million active mobile banking users 2 , and by the end of the fiscal year (mid-July 2024), the number was estimated to have reached 24.6 million. 7 This rapid growth is underscored by other sources, which indicate 23 million users 8 and 26.5 million by mid-January 2025. 9 The number of internet banking users is also significant, although smaller than mobile banking, at around 2.14 million users. 10

Digital wallets such as eSewa, Khalti and IME Pay have become an integral part of the financial lives of many Nepalis. By mid-2023, the total number of wallet users has exceeded 18.9 million11, and by April 2025 it reached 26.37 million.7Some platforms are showing impressive numbers: eSewa, a market pioneer, has over 8-10 million users and over 12 million app downloads by 202411, Khalti – over 5 million users13, and IME Pay is also around 5 million.13The total transaction volume through digital payment systems in Nepal is projected to reach $6.1 billion by 2028.14

The exponential growth of QR payments deserves special attention. From 2021/22 to 2023/24, the volume of QR code transactions increased by an average of 230% annually, and their value by 210%.15In the 2023/24 financial year, transactions worth NPR 500 billion were conducted through QR codes.15Fonepay, one of the leading payment networks, processed over 1 million QR transactions worth Rs 2.62 billion in a single day on March 30, 2025.16The number of QR codes issued by banks and financial institutions for merchants increased from 282,000 in mid-July 2021 to 2.34 million by mid-January 2024.15

NRB’s efforts play a key role in promoting digital payments, including the development of the National Payment Systems Development Strategy and the implementation of the Regulatory Sandbox for FinTech Innovations.1

Comparative analysis and challenges:

Despite the impressive overall performance, there is a significant digitalisation gap between urban and rural areas in Nepal.2 While internet penetration in Nepal as a whole was 55.8% in early 2025, it is significantly lower in rural areas (17.4% of households had internet access in rural areas versus 79.3% in the Kathmandu Valley, according to NLSS 2022/23 19). Internet accessibility issues, especially in remote and mountainous areas, and low digital literacy levels among the population are significant barriers to the widespread adoption of digital banking services.20 As of 2024, digital literacy in Nepal remained low, despite more than 80% of the population having access to the internet.25 This creates a situation where access does not always translate into active and confident use of digital financial instruments.

Impact of the COVID-19 pandemic:

The COVID-19 pandemic has had a catalytic effect on accelerating the adoption of digital payments and banking services in Nepal, as movement restrictions and social distancing requirements have driven a shift to remote channels of interaction.1

Table 1: Digital Banking Channel Usage Statistics in Nepal (2023-2025)

Note: Data from different sources may vary slightly due to methodology and collection period. The table aggregates available information to provide a general picture.

This chart provides a clear indication of the scale and dynamics of digitalization in Nepal’s banking sector. It confirms the relevance of the Digital First strategy and simultaneously serves as a starting point for analyzing the continued role and need for transformation of physical branches, especially given the uneven penetration of digital services.

Nepalese Customers’ Needs and Expectations from Banking Services

Understanding the needs and expectations of Nepalese customers is key to developing effective banking strategies that combine digital and physical channels.

Customer Satisfaction Factors (CSAT):

Nepalese banking customer satisfaction (CSAT), which averages moderate (70-80%)5, is determined by a combination of factors. Key among these are the speed and security of transactions, and the quality of customer support.5 Research shows that digital banking services often have higher CSAT scores5 due to their convenience and efficiency for routine transactions. However, beyond these basic aspects, satisfaction is also influenced by the quality of the product or service itself, price competitiveness (especially in the price-sensitive Nepalese market), cultural awareness of the bank, quality of after-sales service, brand reputation, availability of services (both physical and online), clarity and timeliness of communications, personalization of offers, and technological integration of services.5

Cultural aspects and their influence on preferences:

Nepalese culture has a profound influence on consumer behavior and banking expectations.

- Personal relationships and trust: In Nepal, personal relationships and trust built over long-term interactions are highly valued.4For many customers, especially older generations or those less familiar with digital technologies, personal contact with a bank employee is an important factor in building trust.32This is especially true when making important financial decisions or when problems arise.

- “Saving face” and hierarchy: The cultural concept of “face-saving”4and the respect for hierarchy inherent in Nepalese society4may influence how customers express their dissatisfaction or ask questions for clarification. Some customers may feel more comfortable discussing sensitive issues or expressing disagreements in person in a branch rather than through impersonal digital channels or in a public space. This creates a “latent” demand for tactful and empathetic service in physical branches where issues can be discussed confidentially. Banks should create safe and discreet feedback channels with this in mind.5

- Collectivism and Word of Mouth Marketing (WOMM): Nepalese society is characterized by a high degree of collectivism.5The opinions of reference groups (family, friends, colleagues) and word of mouth play a huge role in decision-making, including the choice of bank and banking products.35A positive in-branch service experience based on quality personal interactions can be a powerful catalyst for positive WOMM, while a negative experience can quickly spread and damage a bank’s reputation.

Demand for personal service:

Despite the growing popularity of digital channels, the need for physical branches remains, especially for certain types of services and customer categories.

- Complex products and consultations: For processing complex banking products such as mortgage loans38, large business loans or receiving investment advice, clients often prefer personal communication with banking specialists.40This is due to the need for detailed discussion of conditions, risk assessment and receiving personalized recommendations.

- Problem solving and non-standard situations: Physical branches remain an important channel for escalating and resolving issues that could not be effectively resolved through digital platforms or call centers. The ability to personally contact a bank employee gives customers a sense of confidence and control over the situation.

- Financial Literacy and the Digital Divide: A large portion of Nepal’s population, especially in rural areas and among the older generation, still has limited access to digital technologies or low levels of financial and digital literacy.26For these types of customers, bank branches are often the primary, if not the only, channel for accessing financial services and receiving the support they need. Even among digitally active young people, as their financial needs become more complex (e.g., first mortgage, investments), they may need expert advice that is more convenient to obtain in a branch.41

High satisfaction rates with digital services can sometimes mask unmet needs for empathy, personalized service, or assistance with non-routine requests that are traditionally associated with service in physical branches. If digital channels cannot fully deliver these aspects, there remains a “latent” demand for high-quality personal service.

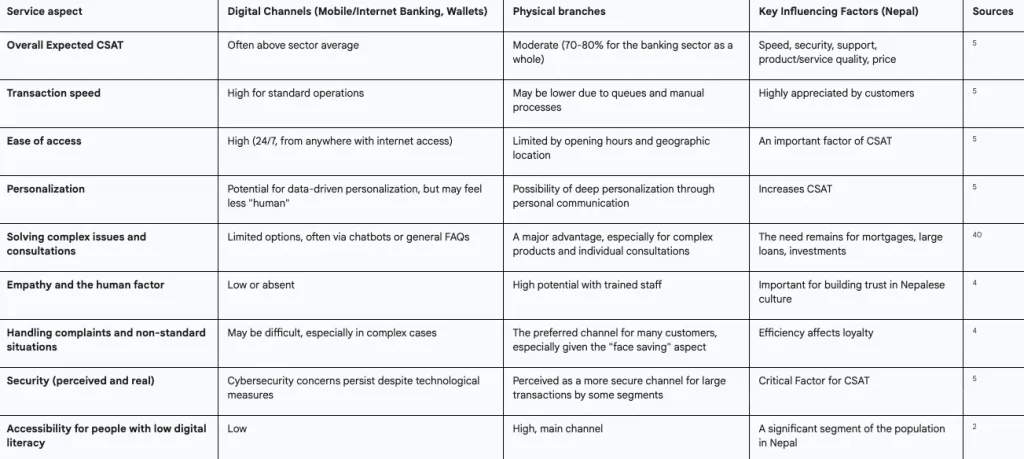

Table: Comparative Analysis of Customer Satisfaction (CSAT) between Digital and Physical Banking Channels in Nepal

This table highlights that despite the advantages of digital channels in speed and convenience for routine transactions, physical branches remain important in Nepal due to their ability to provide face-to-face interactions, resolve complex issues, provide personalized support, and cater to customers with varying levels of digital literacy. This provides the basis for developing a balanced phygital strategy where both types of channels complement each other.

Current Status and Challenges of Physical Banking Network in Nepal

Overview of the existing branch network

The physical banking network in Nepal has undergone significant changes in recent years, largely driven by regulatory policies and the push for financial inclusion.

Quantity and distribution:

As of mid-January 2025, there were 107 licensed banks and financial institutions (BFIs) in Nepal, including 20 commercial banks.43 The total number of branches of all BFIs (including microfinance institutions) reached 11,545 by January 202544 and 11,505 as of 10 months of FY2024/25.45

The largest commercial banks have extensive networks:

- Global IME Bank: According to various sources, from 261 to 440 branches and service points.46For example, as of January 2025, there were 354 branches and 68 additional cash desks.46

- Nabil Bank: About 268 branches and 320 ATMs.49

- NIC Asia Bank: More than 360 branches51, according to some data – 363+.52

- National Banijya Bank: Expanded the network to 307 branches by June 2025.53

NRB Policy on Financial Inclusion:

The Central Bank of Nepal (NRB) has been actively pursuing financial inclusion policies, with a target of having at least one commercial bank branch in each of the country’s 753 local government levels.44 This initiative, launched in 2017, was largely completed by 2025 with the opening of the last branch in the remote Saipal municipality.44 To encourage branch opening in remote areas, the NRB has used various measures, including a rotation system and a lottery system for distributing responsibility among banks44, as well as providing financial incentives such as covering the initial losses of new rural branches and providing them with working capital.54

Accessibility issues in remote areas:

Despite the success in expanding the network, opening and operating branches effectively in remote and rural areas poses significant challenges. These include the lack of basic infrastructure such as roads, stable electricity supply and reliable internet access, as well as security issues.6 These factors not only increase the cost of running such branches, but also limit the range of services provided.

Cost-effectiveness and profitability of traditional branches

The traditional banking branch model faces increasing challenges in terms of cost efficiency.

- High operating costs: Maintaining physical branches involves significant fixed costs, including rent, staff salaries, security costs, utilities and equipment maintenance.

- Reducing transaction flow: With the growing popularity of digital channels, the volume of routine transactions (such as cash withdrawals, bill payments, simple transfers) carried out directly in branches is decreasing.15This results in expensive branch infrastructure being used less intensively.

- Profitability of rural branches: The profitability of branches in rural areas is a particular problem. Low population density, limited volume of financial transactions and lower average income of clients often prevent such branches from reaching the break-even point, despite their social importance and regulator requirements to ensure accessibility.55Historically, even as the network expanded into rural areas, deposit mobilization by such branches remained low and lending was more accessible to customers with existing deposits and collateral.56

Main problems and challenges

Transforming and maintaining the effectiveness of the physical banking network in Nepal faces a number of systemic challenges.

- Infrastructure limitations: The insufficient level of development of telecommunications infrastructure, especially in rural and mountainous areas, limits the possibilities of implementing modern digital solutions in branches and the stability of their work.57Frequent power outages are also a major obstacle.

- Cybersecurity: The integration of digital technologies into branch operations increases the risk of cyber attacks and requires significant investments in data and transaction protection systems.59Recent cyber attacks on financial institutions in Nepal highlight the urgency of this issue.59

- Personnel issues: There is a shortage of qualified personnel with the necessary digital skills, the ability to advise clients on complex products and work in new, technology-intensive service formats.67This requires banks to invest in retraining and developing existing employees, as well as attracting new specialists.

- Bureaucracy and organizational culture: Internal barriers related to bureaucratic procedures and resistance to change within banks can slow down the process of branch network transformation.71In addition, cultural characteristics such as “afno manche” (a system of personal connections and favoritism)33, can influence management decision-making and the effectiveness of strategy implementation.

NRB’s policy to ensure 100% local coverage of bank branches44creates a unique situation. Banks may be forced to maintain potentially unprofitable branches, which limits their ability to simply downsize their network to improve profitability. This, in turn, increases the need to transform such branches into more efficient and multifunctional centers focused not so much on transactions, but on advice, financial education, and support for digital products.

The high non-performing loan (NPL) ratio in Nepalese banks is also a significant factor. As of the third quarter of the 2024/25 financial year, the average NPL rate in commercial banks reached 4.83%.73, and for some banks this figure approached 8%.75This creates financial pressure on banks and may limit their resources to invest in costly branch network upgrades.76Consequently, banks are forced to look for cost-effective and step-by-step transformation models.

Infrastructure problems in rural areas44not only make it difficult for traditional branches to operate, but also limit the effectiveness of some smart solutions that rely on stable internet and electricity supply. This means that transformation strategies need to be differentiated: more technologically advanced solutions may be relevant for urban areas, while hybrid models with an emphasis on human interaction and basic digital tools that can operate in low-connectivity conditions are appropriate for rural areas.

Table 2: Number of bank branches and ATMs of leading commercial banks in Nepal (as of 2024-25)

Note: Data on the number of ATMs for some banks may be missing from the sources provided or may require clarification as of the latest date. “N/A” means “no data”.

This table shows the current scale of physical presence of the major players in the Nepalese banking market. The significant number of branches highlights the importance of branch transformation to remain competitive and profitable in the digital era. Differences in the number of ATMs may also indicate different self-service strategies.

Strategies for Transforming Physical Banking Network in Nepal

With rapid digitalization and changing customer preferences, Nepalese banks are facing the need to transform their physical networks. Branchless banking is not a viable strategy for most banks given the country’s cultural background, financial literacy levels, and infrastructural realities. Instead, rethinking the role and functions of branches, integrating them with digital channels, and adapting to new customer needs is becoming a key focus.

Smart Branch Concept and its Adaptation to Nepalese Realities

The Smart Branch concept is about strategically improving the customer experience through the integration of digital technologies and optimizing personal interactions.83It is not just a set of high-tech devices, but a holistic approach to omnichannel integration of financial services, providing a seamless experience for the customer at all touchpoints.83

Key technology elements of a smart branch include:

- Artificial Intelligence (AI) and Machine Learning (ML): These technologies can be used to personalize offers, gain in-depth analysis of customer data, assess credit risks, and automate routine tasks.84For example, Nabil Bank is already actively implementing AI and data analytics into its digital strategy.88AI-powered chatbots can provide 24/7 customer support, answering routine queries and reducing the workload on staff.86

- Self-Service Kiosks (SSK): Allows customers to perform many routine operations on their own, such as depositing and withdrawing cash, paying bills, printing statements, requesting balance certificates, resetting PINs for mobile banking.89NIC Asia Bank, for example, is introducing kiosks for check deposit, account number verification and other services.91This reduces wait times and allows branch staff to focus on more complex tasks.

- Interactive Teller Machines (ITMs): Provides the ability to video chat with a remote cashier, combining the convenience of self-service with the ability to receive expert advice.40

- Tablets for bank employees: Provides mobility for employees within the branch and allows for more interactive interaction with customers, demonstrating products and services.83

- Biometric authentication: Using fingerprints or other biometric data improves security and ease of access to services by eliminating the need to remember passwords or present identification documents.90

- Video banking: Provides customers, especially in remote areas, with the opportunity to receive advice from a bank expert via video link without visiting the central office.90

- Digital submission of documents: Reduces paperwork and simplifies processes, such as opening an account or applying for a loan.90

Adaptation to Nepalese conditions:

Directly copying Western models of “smart” branches in Nepal is ineffective without taking into account local specifics. It is necessary to consider:

- Level of digital and financial literacy: A significant portion of the population still requires assistance when using digital devices.2The kiosk and app interfaces should be intuitive, in Nepali, possibly with voice support.

- Infrastructure limitations: Unstable internet connection and power outages in some areas44require the presence of backup systems and the ability to operate some services in offline mode.

- Cultural preferences: The importance of personal communication and trust4means that technology should complement, not completely replace, human interaction. A smart branch should offer a balance between digital convenience and human support.

Rethinking the functional purpose of departments

The transformation of the physical network involves not so much a reduction in the number of branches, but rather a change in their role and functionality.

- Consulting hubs: Branches must evolve from places where routine transactions take place to hubs for financial advice and planning.40Customers are increasingly turning to branches for expert advice on complex products such as mortgages, jumbo loans, investment strategies and insurance.

- Financial Literacy Centers: Banks can use their branches to conduct educational programs, seminars and individual consultations on personal finance management, which is especially important for raising the general level of financial culture of the population and involving vulnerable groups.41

- Servicing complex transactions: Transactions that require physical presence, enhanced customer identification or handling large volumes of cash will continue to be carried out in branches.40

- Strengthening the brand and engaging with the community: Branches remain an important point of physical contact with the bank’s brand. They can be used to host events, support local initiatives and strengthen community ties, which helps to increase loyalty.5

- “Universal Banker”: Implementation of the “universal banker” model, where one employee can provide a wide range of services and consultations, from opening an account to assistance in choosing a credit product, and, if necessary, refer the client to a specialist or digital channel.41This improves service efficiency and customer satisfaction. However, in Nepal, this may face the problem of shortage of personnel with the required set of competencies, which will require significant investment in training.

Optimization of the branch network

Optimizing your network doesn’t mean mindlessly cutting it down. It’s about taking a strategic approach to its structure and formats.

- Streamlining and Transformation: Instead of simply closing branches, banks should analyze their efficiency and potential. An example is the experience of Regions Bank in the US, which closed three outdated branches and opened one modern, innovative, consolidating service in its place.83

- Differentiated formats: It is necessary to implement different branch formats depending on the location and target audience. These could be fully functional flagship branches in large cities, compact mini-offices in shopping centers, specialized consultation points or even mobile branches to serve remote areas.

- Location Analysis: Using geo-analytics and customer behavior data to determine the optimal location of new branches and relocation of existing ones, taking into account demographic trends, economic activity and digital penetration levels.

The Phygital Approach: Creating a Seamless Omnichannel Customer Experience

The Phygital strategy involves the harmonious combination of physical and digital channels to create a single, seamless customer experience.5

- Channel integration: The client should be able to easily switch between different channels of interaction with the bank (mobile application, website, ATM, kiosk, branch), starting a transaction in one channel and completing it in another without losing data or having to re-enter information.

- 360-degree customer view: Implementation of modern CRM systems (Customer Relationship Management)5 allows you to collect and analyze customer data from all touchpoints. This makes it possible to create personalized offers, anticipate needs, and provide proactive support.

- Example Nabil Bank: Nabil Bank’s digital strategy based on AI, data analytics and the multifunctional nBank mobile app88, is a prime example of the move towards a phygital model. Positioned as a “super app,” nBank’s app offers a wide range of services, including remote account opening and KYC, which reduces the burden on physical branches and integrates the digital experience into the overall service system.100It is important to note that in the Nepalese context, where trust is often built on personal interactions,32, digital channels should organically complement, and not completely replace human contact. The role of branches here is to be a guarantor of the reliability and physical accessibility of the bank.

Preparing staff for new roles

The success of branch transformation largely depends on the readiness of staff to work in the new conditions.

- Training and skill development: Banks need to invest in comprehensive employee training programs aimed at developing digital competencies, skills in advising on complex financial products, sales techniques, empathy, cultural sensitivity and effective problem solving for customers.5

- Empowerment: Empowering frontline staff to resolve customer issues on the spot improves service speed and customer satisfaction.5

- Formation of a customer-oriented culture: It is necessary to cultivate a customer-oriented approach in the organization, in which each employee is focused on maximum satisfaction of the client’s needs and building long-term relationships.5

Implementing these strategies will require Nepalese banks not only to invest in technology but also to make deep organizational changes and adapt to the country’s unique socio-cultural and economic context.

Maintaining customer loyalty and ensuring profitability through transformation

Transformation of the physical banking network is not an end in itself, but a tool for achieving two key strategic objectives: maintaining and increasing customer loyalty, and ensuring long-term profitability of operations. In the Nepalese context, where tradition and modern technology intertwine, these objectives require a special approach.

Mechanisms to increase loyalty of Nepalese customers

Customer loyalty in Nepal’s banking sector is built at the intersection of quality service, trust, and cultural sensitivity. Transformed branches can play a key role in strengthening these aspects.

- Improving Customer Experience (CX):

- Personalization: Adaptation of products, services and communications to the individual needs of each client becomes possible thanks to the collection and analysis of data through CRM systems5and the use of AI.3Transformed branches, equipped with the right technology and trained staff, can offer customers the exact solutions they need, taking into account their financial situation, goals and even cultural preferences.5Nabil Bank’s nBank app strives for such personalization by offering customized dashboards and services.100

- Convenience and speed: Reducing waiting times in branches through the introduction of appointment systems, the use of self-service kiosks for routine transactions and the efficient work of universal bankers has a direct impact on customer satisfaction.5Clients value their time, and fast but high-quality service leaves a positive impression.

- Empathy and Problem Solving: Despite the growth of digital channels, the ability of branch staff to show empathy, listen carefully to a customer’s problem and offer an effective solution remains a key driver of loyalty, especially in a culture that values human relationships.4Trained staff in transformed departments must be able to do more than just perform operations, they must be able to build relationships.

- Building Trust:

- Transparency and clarity of communications: Clear and timely communication to customers about product terms, rates, any changes and the status of their requests in a language they understand (including Nepali) is the foundation of a trusting relationship.5

- Safety: Ensuring a high level of security for both physical branch transactions and integrated digital transactions (data protection, fraud prevention) is critical to maintaining customer trust.5

- Consistency and reliability: The bank must demonstrate stability and reliability in the provision of services, fulfilling its promises and providing predictably high quality of service at all points of contact.5

- Adaptation to cultural peculiarities:

- Respect for elders and hierarchy: Showing special attention and respect to elderly clients, providing them with comfortable waiting conditions and personal assistance when performing transactions.

- Language support: Providing services in Nepali and, where necessary, other languages commonly spoken in the region.5

- “Saving Face”: Create a non-confrontational, respectful environment in branches where clients can feel comfortable asking questions or discussing problems. Provide discrete channels for resolving difficult or sensitive situations.5

- Loyalty programs and word of mouth promotion:

Implementation of well-thought-out loyalty programs that reward customers for long-term relationships and active use of the bank’s services.5Quality service and positive customer experience in the transformed branches naturally stimulate positive word of mouth, which in Nepal is a powerful tool for attracting new customers.35

Ensuring the profitability of the transformed network

The transformation of the physical network must not only be customer-oriented, but also economically feasible.

Reducing operating costs:

- Automation of routine operations: Transferring the maximum number of standard transactions (payments, transfers, cash withdrawals/deposits) to self-service channels – new generation ATMs, kiosks, mobile and Internet banking – reduces the workload on branch staff and reduces the need for a large number of operating windows.40

- Optimization of space use: New branch formats focused on consultations and sales of complex products can be more compact than traditional transaction halls. It is possible to share space with other services (for example, coffee shops, as in the experience of Capital One41), which reduces rental payments.

- Energy efficiency and resource conservation: The introduction of modern energy-saving technologies in branches (lighting, climate control) and the reduction of paperwork due to digitalization also contribute to a reduction in operating costs.

Increased profitability:

- Focus on sales of complex and high-margin products: The staff of the transformed branches, freed from routine operations, can focus on consulting and selling more complex and profitable products, such as investment funds, insurance policies (bancassurance115), mortgage and business loans. This area is especially promising, given that such products require confidential personal communication.

- Attracting and retaining more profitable customer segments: High net worth individuals (HNWIs) and small and medium enterprises (SMEs) often value a personalised approach, quality advice and the opportunity to discuss their financial strategies with an experienced manager. Transformed branches offering this level of service could be attractive to these segments.

- Cross-selling and up-selling: A deep understanding of the client’s needs, formed through personal communication and supported by data from CRM systems, creates favorable conditions for cross-selling and offering additional services relevant to a specific client.110

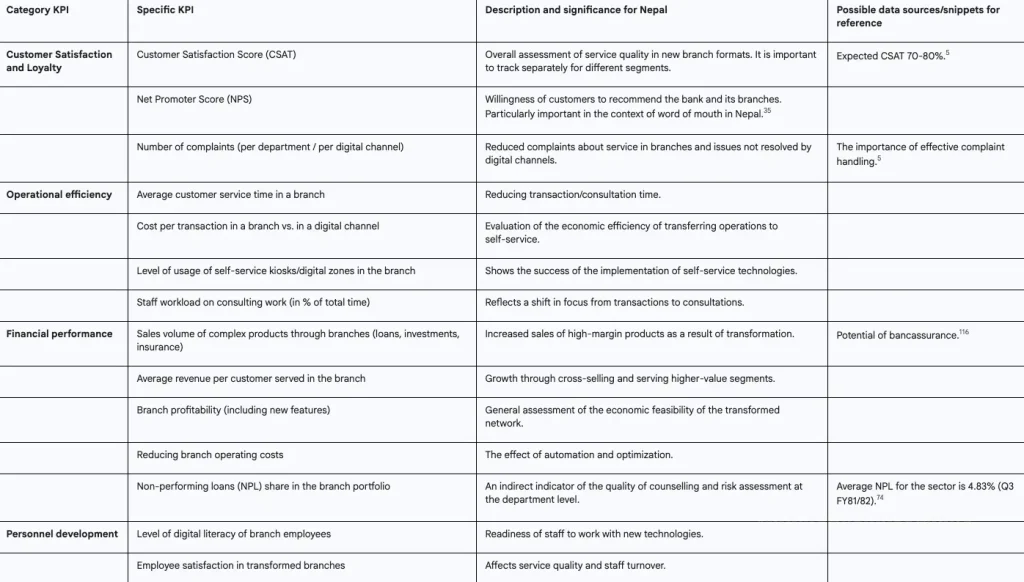

Table 3: Key Performance Indicators (KPIs) for Assessing the Success of Branch Network Transformation

Successful physical network transformation will not only enable Nepalese banks to adapt to the Digital First era but also strengthen their market position by increasing customer loyalty and finding new sources of profitability based on a deeper understanding and satisfaction of the Nepalese consumer.

Recommendations for the Nepalese Banking Sector

To successfully navigate the Digital First era and effectively transform the physical network, Nepal’s banking sector requires a comprehensive strategy that takes into account both global trends and local specifics. The key recommendations are presented below, categorized into short-term and long-term steps, priority investment areas, and suggestions for adapting the regulatory environment.

Short-term and long-term strategic steps to modernize the branch network:

Short-term (1-2 years):

- Deep audit of the existing network: Conduct a comprehensive analysis of the current branch network in terms of profitability, customer flow, types of operations performed, and compliance with local community needs. Use the data to identify branches requiring immediate transformation, repurposing, or relocation.

- Pilot projects of “smart” branches: Launch pilot projects to implement “smart” technologies (self-service kiosks, video banking, tablets for consultants) in several branches of different types (urban, rural, SME-oriented). Carefully monitor KPIs (see Table 3) and collect feedback from customers and employees.83

- Development of basic personnel training programs: Begin training employees in the basics of working with new technologies, consulting skills and customer-oriented service, with an emphasis on cultural sensitivity.5

- Improving existing digital channels: Ensure stable operation and intuitive interface of mobile and internet banking, as they are the basis for the “phygital” strategy.

Long-term (3-5+ years):

- Scaling up successful pilot projects: Based on the results of pilot projects, develop and implement standardized models of transformed branches for various segments and regions.

- Building a full-fledged omnichannel platform: Ensure seamless integration of all service channels (branches, ATM, kiosks, mobile banking, internet banking, call center) with a single CRM system for a 360-degree customer view.5

- Developing a culture of continuous learning and innovation: Create a system for continuous staff development and incentives for initiatives to improve customer experience and operational efficiency.

- Strategic partnership with FinTech companies: Actively collaborate with fintech startups to implement advanced solutions and accelerate digital transformation.128Global IME Bank is already collaborating with IFC to develop digital banking and fintech.128

- Lobbying for improved infrastructure: Work together with other market participants and government agencies to improve the quality of Internet connections and electricity supply in the regions.

Priority investment areas:

- Technologies for departments:

- Self-service kiosks and ITM: To automate routine operations and reduce the workload on staff.89

- CRM systems: To collect and analyze customer data, personalize offers and improve CX.5There are various CRM solutions available in Nepal including international (Salesforce, Zoho) and local ones.94Nest Nepal is an authorized partner of Zoho CRM.96

- AI and data analytics: To improve scoring, fraud detection, personalization and anticipating customer needs.84Nabil Bank actively uses AI and analytics.88

- Video banking systems: To provide remote expert consultations.

- Digital infrastructure of the bank:

- Reliable and scalable Core Banking Systems.

- Development of mobile applications and internet banking: Improved UX/UI, expanded functionality, security. Nabil Bank nBank is positioned as a super app.100

- Cybersecurity: Constantly updating cybersecurity systems.59NRB releases cyber resilience guidance for 202322

- Staff training and development:

- Retraining programs: For cashiers and tellers to become universal bankers and consultants.

- Development of soft skills: Communication, empathy, problem solving, customer focus.5

- Training in digital tools and products.

- Physical infrastructure of the branches:

- Modernization of existing premises: Creation of comfortable and functional areas for waiting, self-service and consultation.

- Ensuring accessibility for people with disabilities.

Proposals for adapting the regulatory environment (taking into account NRB directives):

- Support for innovative branch formats: The NRB could consider introducing more flexible regulatory requirements for smart or small branch pilot projects, particularly in rural areas.

- Promoting financial literacy: Strengthening coordination between NRB, banks and educational institutions to develop and implement national programs to improve financial and digital literacy of the population.2The NRB already has a 2022 Financial Literacy Framework.22

- Development of a regulatory sandbox: Actively using and expanding the NRB regulatory sandbox to test innovative banking products and service models, including those related to branch transformation.1In March 2025, NRB launched the Digital Finance Innovation Hub.18

- Standardization and interoperability: Assistance to NRB in developing standards for new technologies (e.g., a unified QR code15) and ensuring interoperability between various payment systems and banking platforms through the National Payment Switch (NPS).3

- Regulation of Neo-banks: Developing clear regulatory frameworks for the operation of fully digital (neo) banks, which may impact traditional banks’ strategies regarding physical networks.134The government announced the creation of a neobank in the 2025/26 FY budget.134The NRB has already issued guidelines on digital payment security, including VPN and data storage requirements.135

Strategies to overcome the digital divide and improve financial literacy:

- Targeted educational programs: Banks, together with government and public organizations, should develop and implement financial and digital literacy programs adapted to different target groups (rural population, elderly people, women, youth). Use branches as platforms for such programs.

- Simplified digital interfaces: Developing banking applications and kiosk interfaces that take into account the needs of users with low levels of digital literacy (large fonts, voice prompts, support in Nepali).

- Available devices and internet: In collaboration with telecommunications companies and the government, promote access to affordable smartphones and accessible internet in rural and remote areas.

- The role of the “human interface”: Branch staff and banking agents (including branchless banking systems)46) should play an active role in educating customers on how to use digital services and providing initial support.

Implementing these recommendations will enable Nepalese banks to not only successfully transform their physical networks but also make significant contributions to financial inclusion and the development of the country’s digital economy, while maintaining customer loyalty and ensuring sustainable profitability.

Conclusion

A study on the role of bank branches in Nepal in the Digital First era clearly shows that the physical presence of banks remains relevant and necessary despite the rapid growth of digital channels. The future of bank branches in Nepal is not their disappearance, but a profound transformation aimed at integrating with digital technologies, rethinking the functionality, and adapting to the unique needs and cultural characteristics of Nepalese customers.

Key findings of the study:

- The Nepalese customer is becoming increasingly digital but still needs personal interaction. The growth in the use of mobile banking, digital wallets and QR payments is undeniable, especially in urban areas and among young people.15However, for complex financial products, personalized advice and solutions to non-standard problems, clients still prefer to contact branches.40Cultural factors such as the importance of personal relationships, trust and “saving face” also support demand for physical channels.4

- The existing branch network requires modernization and optimization. Despite NRB’s efforts to ensure banking services are available across the country,44, many traditional branches face challenges of high transaction costs, declining routine transaction flow and infrastructure limitations, especially in rural areas.55High levels of non-performing loans (NPL) in the sector75It may also limit banks’ resources for large-scale investment in transformation.

- Transformation strategies must be comprehensive and tailored. Implementation of the concept of “smart” branch using AI, self-service kiosks and video banking40, reorientation of branches to consulting services and financial education41, optimizing branch formats and locations, and implementing a phygital approach to ensure a seamless omnichannel experience5, are key areas. It is important that these strategies take into account the local context, including the level of digital literacy and infrastructural capabilities.

- Branch transformation is the path to increased loyalty and profitability. The enhanced customer experience through personalization, convenience and empathy provided at the transformed branches has the potential to strengthen the trust and loyalty of Nepalese customers.5At the same time, automation of routine processes and focus on selling high-margin products will reduce operating costs and increase the profitability of the physical network.40

Development forecast and key success factors:

Physical service channels in the Nepalese banking sector will not disappear, but their role and form will evolve. The success of this transformation will depend on several key factors:

- Customer focus: Deep understanding and meeting the changing needs of different segments of Nepalese customers.

- Technological adaptation: Reasonable and gradual implementation of technologies corresponding to the level of infrastructure development and digital literacy of the population.

- Staff development: Investments in training and development of employees capable of working in new formats and providing high-quality consulting services.

- Flexibility and innovation: The willingness of banks to experiment with new branch models and quickly adapt to market changes.

- Supportive regulatory environment: NRB policies that promote innovation, financial literacy and digital infrastructure development.

Ultimately, banks that can effectively integrate their physical and digital channels, creating value for customers and streamlining their operations, will not only remain relevant in the Digital First era, but will also secure a sustainable competitive advantage and long-term profitability in the Nepalese market.ant factors for sustainable economic growth and improving the quality of life of the people of Nepal.

Sources used

- Digital Financial Services in Nepal – International Finance Corporation

- THE IMPACT OF DIGITAL TRANSFORMATION ON BANKING SERVICES AND CUSTOMER EXPERIENCE: A STUDY OF THE NEPALESE BANKING SECTOR – Theseus

- Digital 2025: Nepal — DataReportal – Global Digital Insights

- Development in Digital Capitalism: Challenges and Prospects of Nepal

- FY 2023/24 – Nepal Rastra Bank

- NRB Introduces New Rules for Digital Payment Security – Beemapost.com

- Nepal Rastra Bank launches digital finance innovation hub to boost fintech

- Connecting the Unconnected: Bridging the Digital Divide through Grassroot Initiatives in Sri Lanka and Women’s Empowerment in Nepal – NetMission.Asia

- Digital 2024: Nepal — DataReportal – Global Digital Insights

- Financial Technology Adoption in Nepal – Hamzah Academy

- QR code drives Nepal’s digital payment boom – The Kathmandu Post

- Bring Law To Promote Neobanking – The Rising Nepal

- Non-performing loans of commercial banks: How AI can revolutionise their management

- NPRC Journal of Multidisciplinary Research Artificial Intelligence in Microfinance: Enhancing Customer Experience at ESAF Bank

- FinMin Presents Economic Survey, Projects 4.61pc growth for current FY

- Nepal expects 4.61-pct growth for 2024-25 – Xinhua

- Nepal’s Economy Expected to Remain Resilient in Face of Economic Shocks, says World Bank

- Nepal Development Update, April 2025 – World Bank

- In-Depth Analysis of the Economic Situation & Business Opportunities in Nepal. Forecast 2025-2030

- Nepal’s Economy Will Likely To Grow By 4.4 In Fiscal Year 2025: ADB

- World Bank projects Nepal’s economic growth at 4.5 percent – myRepublica

- Nepal and the IMF

- Nepal Inflation Rate Outlook, Average Consumer Prices (I:NIRA5NJM) – YCharts

- Nepal Inflation Rate – Trading Economics

- Macroeconomic Snapshot of 9 Months: Inflation at 3.39%; Foreign Reserves Reach USD 17.63 Billion; Remittance Surges 10% – || ShareSansar ||

- Current Macroeconomic and Financial Situation – English (Based on Nine Months Data of 2024/25) – Nepal Rastra Bank

- Rs. 1,191 billion remittance received in nine months – The Rising Nepal

- Current Macroeconomic and Financial Situation – English (Based on Seven Months Data of 2024/25) – Nepal Rastra Bank

- Nepal Receives remittances over 1,191 billion in nine months | New Spotlight Magazine

- Nepal records Rs 7.42 billion in remittance outflow in the first nine months – CESLAM

- Current Macroeconomic and Financial Situation of Nepal

- The Role of Remittances in Household Spending in Rural Nepal – MDPI

- Trends and Destinations of Foreign Labour Migration in Nepal

- Remittance inflows pose Dutch Disease risk in Nepalese economy – CESLAM

- Publication: Nepal Development Update, April 2024: Nepal’s Economy on a Recovery Path but Private Investment Remains Low

- Nepal’s long-term growth may stall below 4 percent, World Bank warns

- Access to Financial Services in Nepal – World Bank Open Knowledge Repository

- Nepal Economy Update – April 2025 – CARE Ratings

- NRB’s Third Quarter Monetary Policy Review: Risk Weight on Share Mortgage Loans Reduced From 125% to 100%, Foreign Reserves Strengthen – || ShareSansar ||

- Total Number of Tourist arrival in Nepal in year of 2025 is 5,01,264

- Nepal News Evening Economic Brief – June 8, 2025

- IMPLEMENTATION OF THE GLOBAL COMPACT FOR MIGRATION IN NEPAL – International Trade Union Confederation

- BOP remains at surplus of Rs 210.22 billion in last nine months of current FY

- NRB monetary policy review: Current account at surplus of Rs 210.22bn, BOP at surplus of Rs 346.23bn – Business 360°

- Nepal Foreign Exchange Reserves, 2002 – 2025 | CEIC Data

- 2025 Monitoring Report – the United Nations

- Top 20 Influencers in Nepal in 2025 – Favikon

- Foreign exchange reserves surpass Rs 2426 billion – myRepublica

- An Analysis of Causal Relationship between Remittances and Imports in Nepal

- Symptoms of Dutch Disease in Nepal

- Contact NIC ASIA Bank

- Sensitive Data of Nepal’s PM’s Office Allegedly for Sale – Cyber Press

- April 2025: Major Cyber Attacks, Ransomware Attacks and Data Breaches

- The State of the Industry Report on Mobile Money 2025 – GSMA

- Nepal’s Foreign Trade Reaches Rs 1692 Billion in 10 Months of FY 2024/25 – ShareSansar

- April 2025 Analysis – CESIF Nepal

- Bank Stability and its Determinants in the Nepalese Banking Industry – Nepal Rastra Bank

- Taking banking access to rural Nepal – The Annapurna Express

- Delving into Q3 2081/82: Performance Analysis of Leading Commercial Banks with Key Financial Insights – || ShareSansar ||

- Banks set aside Rs 35.07bn for loan losses in Q3 | The Annapurna Express

- Non-Performing Loans of Commercial Banks Reach 4.83% in Q3 of FY 2081/82

- Nepal: Fourth Review Under the Extended Credit Facility Arrangement-Press Release; Staff Report; and Statement by the Executive Director for Nepal in: IMF Staff Country Reports Volume 2024 Issue 225 (2024) – IMF eLibrary

- Increasing NPL and accumulation of non-banking assets are major challenges of banks: NRB – myRepublica

- Nepal Rastra Bank, Financial Stability Report 2024

- Financial Institutions Supervision Report – 2023/24 – Nepal Rastra Bank

- Monetary Policy for 2024/25 – Nepal Rastra Bank

- Key Highlights of Nepal’s Monetary Policy for FY 2024/25 – Nepal Economic Forum

- NRB unveils mid-term monetary policy review, Slashes loan …

- Current Macroeconomic and Financial Situation of Nepal – Nepal Rastra Bank

- Monetary Policy 2024/25: Bank rate and deposit collection rate lowered – The Rising Nepal

- NEPSE sheds 5.21 points despite NRB announcing flexible policy in loans against shares

- Breaking The Cycle Of Brain Drain – The Rising Nepal

- Brain Drain and Its Effects on Livelihood: An Analysis of Phalewas Municipality, Nepal

- Nepal’s Labor Market Dilemma: Bridging the Gap Between Workers and Employers

- How economic inequality is driving youths abroad – The Annapurna Express

- Credit expansion rises 7.1 percent in nine months – The Annapurna Express

- Current Macroeconomic and Financial Situation – English (Based on Five Months Data of 2024/25) – Nepal Rastra Bank

- Six Months – Current Macroeconomic and Financial Situation of Nepal

- Enhancing Customer Satisfaction in Nepalese Banks and Financial Institutions: The Influence of Service Quality on Different Dim – ResearchGate

- (PDF) Service Quality and Customer Loyalty in Nepalese Commercial Banks: A Mediating Role of Customer Trust – ResearchGate

- Rastriya Banijya Bank Expands with 10 New Branches, Strengthening Financial Inclusion Across Nepal – || ShareSansar ||

- Nepal’s Economy at a Crossroads: Can the New Governor Unlock Confidence in the Banking Sector, Lenders and Credit? – || ShareSansar ||

- The Nepalese Bureaucracy: A Historical Perspective – Prachanda’s Knowledge Share

- Vulnerability Profile of Nepal – the United Nations

- Nepal: World Bank Report Outlines Key Reforms to Boost Growth, Create Jobs

- The World Bank in Nepal: Lessons on building institutions and Influencing policy

- Nepal ranking in the Global Innovation Index 2024 – WIPO

- Co-development of vulnerability and risk assessment framework and methodology for Nepal

- MULTI-SECTORAL RISK ASSESSMENT OF SIX GROUND CROSSING POINTS ALONG THE NEPAL-INDIA BORDER

- Multi-sectoral Risk Assessment of Six Ground Crossing Points Along the Nepal-India Border

- What is Last Mile? Complete Guide on Challenges & Future Trends – FarEye

- Navigating Last Mile Chaos – Logistics Business® Magazine

- datareportal.com

- Adoption of Digital Banking in Nepal: An Analysis of Customer Perceptions and Behaviors

- Nepal’s Dilemma Over Social Media Regulation – The Diplomat

- Cultural Considerations in Nepal – Rivermate

- Nepal’s Workplace Culture “A blend of Respect, Relationships, and Reform” – Learn-Moodle

- A Guide to Business Etiquette in Nepal | ClickUp™

- Afno Manche | PDF | Social Network – Scribd

- SWOT Analysis of eSewa: What to Know in 2025

- Khalti and IME Pay Merger: A threat to eSewa? – GadgetByte Nepal

- Khalti Digital Wallet app crosses 1 million downloads on Google Play; emerges as one of the preferred digital wallet services within 3 years – || ShareSansar ||

- Fonepay Sets Record with Over 1 Million QR Transactions in a Single Day

- Fonepay Breaks Records: Over 1 million+ QR transaction in Single-Day – Our Blogs

- Digital transactions surge at 210% annually – myRepublica

- eSewa Pioneering Digital Payments in Nepal – B360 – Business 360°

- ESewa to Global IME Bank 2024-11-22 | PDF – Scribd

- Khalti Marks Seven Years of Digital Transformation with Exciting Anniversary Offers

- Prospects and Challenges of Digital Payment in Nepal

- Transaction Limits – Fees, Limits & Types – Khalti

- Financial Literacy and Digital Payment System in Nepal – ResearchGate

- ictframe.com

- Nabil Bank conferred ‘The Bankers Technology Award-2025’ – Insurance Khabar

- nBank on the App Store

- nBank on the App Store

- NIC Asia Bank partners with Khalti to facilitate digital payments – :: Business 360°

- Wallyt Partners with NIC ASIA Bank to launch WeChat Pay and UnionPay Mobile Payment in Nepal

- Global IME Bank Partners with IFC to Advance Digital Banking and Fintech in Nepal

- Global IME Bank launches card-based global payment gateway – Spotlight Nepal

- FinTech innovations: Transforming Nepal’s banking landscape – Onlinekhabar English

- Social Media Marketing in Nepal: Trends & Opportunities

- Number of electronic transaction increases, while transaction amount falls by Rs 10 billion

- Nepal: Fifth Review Under the Extended Credit Facility Arrangement and Request for Modification of a Performance Criterion-Press – IMF eLibrary

- The Slow Rise of AI in the Banking Sector: Challenges and Opportunities

- The Use of Artificial Intelligence and Machine Learning in the Nepalese Financial Sector

- Nabil Bank wins ‘The Banker’s Technology Award 2025’ for Asia Pacific region

- IMF Executive Board Completes the Fifth Review under the …

- Best Data Science Courses in Nepal – Stamford College Kathmandu

- What jobs come from data science courses in Nepal – IABAC

- Most Trending IT Courses in Nepal: What’s Hot in 2025 – Presidential Graduate School

- The Global Demand for MBA Talent: Top Industries Hiring in 2025 – MIT Nepal

- 38176-015: Skills Development Project | Asian Development Bank

- IVR Banking Service | NIC ASIA BANK LIMITED

- Exploring Sustainability in Cloud Computing Adoption among SMEs in Nepal: A Conceptual Model – Human Resource Management Academic Research Society

- Global law enforcement action in Asia nets large infrastructure seizure, 32 arrests