This report analyses the profound transformation of Nepal’s remittance market driven by the rapid adoption of digital financial services (DFS) and fintech innovations. There is a clear shift from traditional, often informal, remittance channels to more formalised, digital and efficient methods.

Key findings indicate that ‘new generation remitters’ – the younger, more tech-savvy generation of Nepali diaspora and recipients in the country – are increasingly using mobile banking, digital wallets (such as eSewa, Khalti, IME Pay) and QR payments to send and receive remittances. This trend is supported by the rapid growth in user numbers and transaction volumes on these digital platforms.1

The digital transformation of the remittance sector offers significant opportunities for Nepal’s commercial banks. These include expanding their customer base, especially among the younger generation, creating new revenue streams by offering additional digital services, significantly improving operational efficiency, and the potential to deepen financial inclusion across the country.

At the same time, commercial banks face a number of challenges. The main ones are increased competition from agile fintech companies, the critical need to ensure reliable cybersecurity measures to protect transactions and customer data, the need to overcome the gap in the level of digital literacy of the population, and the difficulty of adapting to a dynamically changing regulatory environment.3

The report formulates key strategic recommendations for commercial banks to capitalize on emerging opportunities and minimize risks. These strategies focus on introducing innovations in service delivery, developing strategic partnerships with fintech companies, maintaining a customer-centric approach, and using data analytics to make informed decisions and personalize offers.

The emergence of the “new generation remitter” represents more than just a demographic shift, but a fundamental change in financial consumer behavior. This demographic expects remittance services to be not only fast and cost-effective, but also transparent and easy to use. These expectations are forcing a rethink of the traditional banking models that have long dominated the remittance market. Younger generations, having grown up in the digital age, are inherently more comfortable using digital tools.5This comfort translates into an expectation that financial services will be as seamless and instantaneous as other digital interactions. Traditional methods of remittances, often associated with physical agents and long processing times, are becoming less attractive. The success and rapid adoption of digital wallets such as eSewa and Khalti1, vividly illustrate this change in consumer preferences.

While fintechs are driving innovation in the remittance sector, commercial banks have a significant advantage in terms of established customer trust and existing physical and financial infrastructure. By strategically leveraging these assets, through proactive digital transformation and smart partnerships, banks can not only maintain but also expand their share of the dynamic remittance market. Fintechs are characterized by agility, lean operating models, and a strong focus on user experience.1However, the basis of all financial services, especially in the socio-cultural context of Nepal, where personal relationships and established reputation are highly valued11, trust remains. Commercial banks, due to their long-standing presence, regulatory compliance, and often larger capital base, typically inspire greater confidence when conducting large or mission-critical financial transactions. The strategic challenge for these banks is to synergize their existing capital of trust with the convenience, speed, and innovation that fintech offers. This can be achieved through direct partnerships with fintech firms.14or by accelerating the development and improvement of our own advanced digital platforms.16

Transformation of the Remittance Market in Nepal

The Indispensable Role of Remittances in Nepal’s Economy

Remittances play a vital role in Nepal’s economy, being one of its cornerstones.

- Macroeconomic significance: Remittances constitute a significant portion of Nepal’s gross domestic product (GDP), often exceeding 20-25%.18For example, in 2022, remittances covered 56.6% of Nepal’s trade deficit and became the most important component of the country’s balance of payments.20Nepal consistently ranks high in the world in terms of remittances to GDP ratio.20This dependency underscores the critical importance of efficient and accessible remittance channels. As of the nine-month period of FY2024/25, remittance inflows increased by 10.0% in Nepalese rupees to reach INR 1191.31 billion (equivalent to US$8.74 billion).22

- Impact on poverty reduction and household consumption: Remittances make a significant contribution to poverty reduction and support household spending on essential goods and services such as food, education and health care.20In particular, their role in improving nutrition and developing human capital in recipient families is noted.20The World Bank also notes that remittances supported private consumption in the first half of fiscal year 2024.24

- Contribution to foreign exchange reserves: A steady and substantial inflow of remittances is the basis for maintaining Nepal’s foreign exchange reserves. These reserves are critical to covering import bills, managing external debt, and ensuring overall macroeconomic stability.25As of mid-April 2025, gross foreign exchange reserves reached NPR 2426.84 billion, which is enough to cover imports of goods for 17.1 months.22

Profile of the ‘new generation remittance’: changing demographics and expectations

- Demographics: The “new generation remittance” is typically younger, more educated and digitally literate people, often Gen Z and millennials, working abroad.5The significant outflow of Nepalese youth to work abroad is a well-documented trend.28, which forms the core of this remittance base. In 2024, 1.674 million Nepalese migrated abroad, of which 66,835 were permanent residents.29

- Digital Literacy: This demographic demonstrates high rates of smartphone and internet service adoption, making them receptive to digital financial solutions.30Nepal’s internet penetration rate to reach 55.8% by early 202530, while a significant portion of users actively use social networks.

- Expectations: This group demands faster, more cost-effective, convenient and transparent remittance services. They are less tolerant of the delays and opacity of traditional remittance processes and highly value user experience and digital accessibility.33

Large and persistent reliance on remittances, while providing critical economic support, can produce symptoms consistent with the “Dutch disease”.20“Dutch disease” describes the phenomenon whereby large inflows of foreign exchange (such as from natural resource exports or, in the case of Nepal, remittances) cause the real exchange rate to appreciate. This makes the country’s exports less competitive and imports cheaper, potentially hurting domestic productive sectors such as agriculture and manufacturing.35While remittances certainly boost household consumption and well-being20, if these funds are predominantly channeled into consuming imported goods rather than investing in domestic production or value-added creation, the long-term productive potential of the Nepalese economy could be undermined. The increasing digitalization of these remittance flows, making funds more accessible and faster37, could paradoxically exacerbate this risk if incoming funds are not strategically directed toward productive domestic investment. This presents a strategic challenge for commercial banks, but also an opportunity to develop products that encourage remittance income to be invested in local productive enterprises.

The cohort of “new generation remittances” is heterogeneous. Their preferences, digital capabilities, and adoption rates for different remittance channels will vary significantly depending on factors such as their country of employment (and its digital ecosystem), income level, access to technology for both themselves and their recipients, and their innate digital literacy. This heterogeneity requires financial institutions to offer nuanced and segmented services. While the overall trend toward digitalization is clear, the specific context of both the sender and recipient matters greatly. A sender in a highly developed digital economy such as South Korea or Europe, with easy access to sophisticated online banking services and low-cost digital transfers, will exhibit different behaviors and expectations than a sender in a Gulf country with potentially more limited or expensive digital access. Similarly, recipients in urban centers in Nepal with reliable internet and high smartphone penetration39will interact with digital money transfers differently than those in remote rural areas who face infrastructure challenges and low literacy levels.39Therefore, commercial banks should avoid a one-size-fits-all approach and instead segment this “new generation” to effectively tailor their digital products for money transfers, marketing and support services.

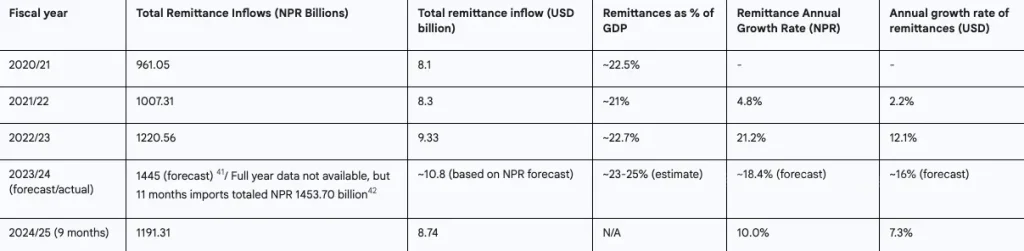

Table 1: Contribution of Remittances to Nepal’s Economy (FY2020/21 – FY24/25)

Sources: Remittance inflow data:.22 GDP data and calculations % of GDP: 18 and estimates based on available data. Data for 2020/21 and 2021/22 are taken from earlier NRB and IMF reports, the exact references to which are not in the current set of snippets, but the general trend is confirmed.134

Note: GDP and % of GDP figures are approximate due to differences in reporting periods and sources. Forecast for FY2023/24 is based on data.41

This table clearly demonstrates the critical importance and scale of remittances to Nepal’s economy, providing a basis for understanding the significance of transformations in this market.

Digital Wave: Fintech and New Channels Transform Money Transfers

The remittance market in Nepal is undergoing a fundamental change driven by digital technology and fintech innovation. Traditional methods are giving way to faster, more convenient and often cheaper digital alternatives that are being embraced by both senders and recipients.

The rise of digital wallets (eSewa, Khalti, IME Pay) and mobile banking

- User base growth and market penetration: Mobile banking has seen explosive growth, with the number of users increasing from 11.4 million in mid-July 2020 to 26.5 million by mid-January 2024.43Digital wallet users are also showing exponential growth; eSewa reported over 12 million app downloads by 20248 and claims 8+ million users6, while Khalti reports over 5 million users.6IME Pay also has a significant user base of 5 million.6The total number of digital wallet accounts in Nepal is significant, reaching 25.8 million by mid-January 2025.44This demonstrates a strong preference and rapid adoption of mobile-first financial solutions.

- Transaction volumes and costs: The transaction volumes through these platforms are indicative of their growing integration into everyday financial life. Transactions through mobile banking stood at Rs 374.66 crore in the mid-October to mid-November period (year-on-year from Rs 218.3 crore), while transactions through e-wallets rose to Rs 37.31 crore from Rs 20.24 crore during the same period.10Fonepay, a major QR network, processed over 1 million QR merchant payments in a single day (March 30, 2025) worth Rs 2.62 billion.45This demonstrates the potential and acceptance of these platforms to facilitate high volume, lower value transactions, which is increasingly relevant for domestic P2P transfers and potentially for small money transfers.

- Diversification of services: These platforms are no longer just for P2P transfers; they offer a range of services including utility bill payments, mobile top-ups, online shopping, ticket bookings, and increasingly integrated money transfer services.1This creates a sustainable ecosystem that encourages regular use.

- Competitive Impact: The ease of use and variety of digital wallet offerings are creating a growing competitive challenge for traditional banks in the digital payments space.4This competition extends to money transfers as these wallets expand their cross-border capabilities.

The spread of QR payments and their cross-border prospects

- Explosive internal growth: QR code-based payments have seen phenomenal growth, with transaction volumes growing at a CAGR of 230% and transaction values at a CAGR of 210% between FY21/22 and FY23/24.43The number of QR codes issued by BFI to merchants increased from 282,000 in mid-July 2021 to 2.34 million by mid-January 2024.43The transaction value increased from Rs 20.28 billion in FY21/22 to Rs 500 billion in FY23/24.43

- Cross-border QR potential: A major milestone was the launch of cross-border digital payments with India through UPI acquiring services, which processed Rs 1.41 billion in 519,039 transactions by mid-February 2024.43Similarly, payments through Alipay+, UnionPay and WeChat for transactions with China during the same period amounted to Rs 101.21 million.43This is a critical step in formalising the significant remittance flows from India, traditionally dominated by informal channels.

- Regulatory support: NRB is actively promoting the use of unified QR codes through platforms like Fonepay QR, Smart QR and their integration through Nepal Clearing House Limited (NCHL)2, striving for interoperability, which is the key to widespread adoption.

The emergence of API banking and open banking initiatives

- Creating an ecosystem: Commercial banks in Nepal are increasingly providing API (application programming interface) access to third-party fintech companies, allowing them to integrate banking services, including payment initiation and account information, into their own applications.2

- Stimulating innovation: NRB actively promotes partnerships between banks and financial institutions (BFIs) and fintechs.2This collaborative approach is in line with global trends towards open banking and is expected to drive innovation in the remittance space, offering users more choice, a better integrated experience and potentially lower costs. This could lead to the emergence of ‘remittance plus’ services, where sending money is linked to other financial activities.

The Potential of Neobanks and Fully Digital Banking

- New banking paradigm: Neo-banking, characterized by fully digital transactions without physical branches, is a new concept in Nepal. It promises cost-effective, customer-centric financial services accessible through mobile apps and websites.5

- Political support: The Government of Nepal has signalled its intention to support this evolution by making announcements in the FY2025/26 budget regarding the establishment of a neobank.5This points to a policy direction that favours purely digital banking models.

- Addressing financial exclusion: Neobanks have the potential to significantly improve financial inclusion by reaching the approximately 18% of Nepal’s population currently unbanked, and by addressing the specific needs of SMEs through tailored digital accounts and credit products.5

- Innovation hub and regulatory sandbox: Creation of the NRB Innovative Hub of Digital Finance in March 202547and its plans to launch a regulatory sandbox37are critical to testing and developing such innovative banking models, including neobanks, in a controlled environment prior to full-scale implementation.

The rapid adoption and expansion of QR payments, particularly cross-border initiatives with India (UPI), represent a significant potential shift in the formalization of traditionally informal remittance corridors. This transformation has the potential to dramatically improve traceability, strengthen anti-money laundering and counter-terrorism financing (AML/CFT) measures, and provide more accurate data on remittance volumes and their economic impact. A significant portion of remittances, particularly small, frequent transfers from India, have historically flowed through informal channels such as hundis due to convenience, established networks, and perceived lower costs. Adopting interoperable QR payment systems43, especially those related to India’s UPI, directly addresses the convenience aspect. If these formal digital channels can also compete on cost and user experience, they can capture a significant share of these informal flows. Such formalization will result in more transactions going through the regulated financial system, which will enhance the ability of authorities to monitor AML/CFT compliance (as per concerns raised in48) and will provide economists and policymakers with more reliable data on actual remittance inflows and their contribution to the economy.

Simultaneous promotion of neobanks5and development of API/open banking infrastructures2foreshadow a future in which remittance services are increasingly integrated into broader digital ecosystems, rather than operating as standalone offerings. This evolution will force commercial banks to fundamentally rethink their service delivery models and integration strategies to remain competitive. Neobanks are inherently digital and often build their services around a seamless, integrated user experience.5API banking allows third-party developers, including other fintechs or even non-financial service providers, to embed banking functionality (such as payment initiation for money transfers) directly into their platforms.2This means that users can initiate money transfers from social media, e-commerce platforms or gig economy portals used by migrant workers. Commercial banks will need to adapt, either by providing robust and secure APIs for such integrations or by developing their own comprehensive “super apps” (like Nabil Bank’s nBank concept, described in50), which offer a similar integrated and convenient experience. This goes beyond traditional branch transactions or simple online banking portals for money transfers.

Table 2: Growth of Digital Payment Instruments and Users in Nepal (Mid-July 2020 – Mid-January 2025)

Sources: NRB Payment Systems Oversight Reports 51, NRB Current Macroeconomic Reports 43, and platform-specific data where applicable and reliable.6

Note: Some 2020 data is estimated due to lack of precise figures in the provided materials for all categories. Growth is calculated based on available comparable periods.

This table clearly illustrates the rapid expansion of the digital financial ecosystem in Nepal, providing evidence for the thesis of a “digital wave” transforming remittances.

Drivers of Remittance Ecosystem Transformation in Nepal

The transformation of the remittance market in Nepal is driven by a combination of interrelated factors, including technological advancements, proactive regulatory stance, and changing consumer expectations. These drivers are creating an enabling environment for the shift from traditional channels to digital solutions.

Increasing Internet and Smartphone Penetration

- Current status: The internet penetration rate in Nepal reached 55.8% of the total population by early 2025, with 16.5 million internet users.30This is a significant increase compared to previous years, although there was a slight decline (-0.2%) between January 2024 and January 2025. Mobile broadband is the predominant way to access the internet.39

- Smartphone Distribution: The number of active cellular mobile connections at the start of 2025 was 39.0 million, equivalent to 132% of the total population, indicating high levels of mobile phone ownership, often with multiple SIM cards. According to GSMA Intelligence, 80.5% of these connections can be considered broadband (3G, 4G or 5G).30This ubiquitous mobile access is a key factor driving the growth of mobile money transfer services.

- Meaning: The growing digital footprint, especially through mobile devices, creates fertile ground for the adoption and scaling of digital money transfer solutions as users are increasingly equipped with the necessary hardware.

Proactive Regulatory Position: NRB Stimulating Digital Financial Services and Innovation

- Strategic vision: The Central Bank of Nepal (CBN) clearly recognizes that the future of financial services lies in digitalization and is acting as a catalyst for innovation in this area.37

- Political framework: The successful implementation of the National Payment Systems Development Strategy and the Retail Payments Development Strategy with the support of the IFC has played a decisive role in promoting low-cost, fast and secure digital payment methods.37

- Licensing and incentives: The NRB has issued licenses to numerous payment system operators (PSOs) and payment service providers (PSPs) – by mid-January 2024, there were 9 PSOs and 25 PSPs.51The Central Bank actively encourages the use of mobile wallets, e-banking and QR payments to promote financial inclusion and move towards a less cash-based society.37

- Support mechanisms: The introduction of electronic KYC guidelines simplifies digital inclusion in financial services.2The National Payment Gateway (NPS), operated by NCHL, facilitates interoperability between various payment systems.2

- Promoting Innovation: Establishment of the Digital Finance Innovation Hub in March 202547and ongoing preparations for the launch of the regulatory sandbox37demonstrate the NRB’s commitment to creating a structured environment for fintech companies to test innovative solutions, including those related to money transfers.

- Coherence of monetary policy: Monetary policy for FY2024/25 supports these digital initiatives and aims to improve lending to productive sectors, which could be complemented by effective remittance channels.42

Evolution of consumer preferences: demand for speed, convenience and low costs

- User expectations: The “new generation of remitters” and their recipients, being more digital in nature, have higher expectations of financial services. They demand speed, convenience and cost efficiency, reflecting their experience with other digital platforms.5

- Departure from traditional methods: Traditional money transfer channels are often perceived as cumbersome, slow and sometimes opaque in terms of fees.54Digital channels, by contrast, offer faster transaction speeds, 24/7 availability and potentially lower costs due to less reliance on physical infrastructure and intermediaries.33

- User experience value: A seamless and intuitive user experience is a critical factor driving the adoption of digital remittance services, as fintech companies often excel in this area.

The proactive regulatory approach of NRB, in particular the establishment of the Digital Finance Innovation Hub and the planned regulatory sandbox, is a major catalyst for the development of the digital remittance ecosystem in Nepal.flexibility and efficiencyregulatory frameworks to accommodate rapidly emerging fintech models (such as neobanks or complex cross-border payment solutions) will be critical to supporting innovation. Lengthy approval processes or ambiguous guidelines may inadvertently stifle innovation or channel it into less regulated, potentially riskier areas. While the NRB’s supportive stance is clear37, practical implementation of new frameworks for such new entities as neobanks5, or advanced cross-border payment systems, requires clear, timely and adaptable guidelines. If the regulatory path from sandbox testing to full operational licensing is unclear or overly burdensome, this could discourage innovators or force them to operate in regulatory grey areas, thereby increasing systemic risk. Digital Finance Innovation Hub47— this is a positive step, but its ultimate success will depend on its ability to provide clear paths and timely feedback to innovators, ensuring that viable and safe solutions can effectively reach the market.

Consumer demand for “speed, convenience, and lower costs” in remittance services is not just a preference, but a powerful competitive force. Fintechs are cleverly exploiting these demands to disrupt traditional financial players. Commercial banks that fail to meet these changing expectations in their remittance offerings risk losing significant market share not only to other banks but, more importantly, to non-bank payment service providers and digital wallet operators. Today’s consumers, especially the younger, digitally savvy generation, are increasingly looking to expand their reach and expand their reach.5, are highly selective and quick to adopt services that offer higher value and better user experience.33Rapid adoption and adoption of digital wallets in Nepal1demonstrate this. If commercial banks’ digital remittance services are perceived as clunky, expensive, or slow compared to fintech alternatives, both senders and recipients of remittances will naturally gravitate toward more efficient options. This isn’t just a loss of remittance market share; it’s a potential loss of broader customer relationships, since remittances often serve as an entry point to other financial services.

Impact Analysis: How Digitalization is Changing Remittance Flows

Digitalization is having a multifaceted impact on the remittance ecosystem in Nepal, leading to tangible improvements in the speed, cost and transparency of transactions, as well as opening up new avenues for financial inclusion.

Improving transaction speed, cost efficiency and transparency

- Speed: Digital channels inherently provide faster transaction processing compared to traditional manual systems. Real-time or near-real-time transfers are becoming the norm for digital financial institutions, significantly reducing waiting times for recipients.37

- Economic efficiency: Digital-first players such as neobanks5 and digital wallets often have lower transaction costs (no extensive branch networks, automated processes). This structural advantage can lead to lower transaction fees for consumers, making money transfers more accessible.

- Transparency: Digital transactions create an auditable trail. This increases transparency for both senders and recipients, allowing them to track funds and verify transactions. It also helps regulatory oversight, especially for AML/CFT purposes.48, and reduces the risk of funds being lost or delayed without clear tracking.

Expanding Accessibility: Bridging the Rural-Urban Gap?

- Reach Potential: Mobile banking and digital wallets could theoretically extend financial services, including money transfers, to geographically remote and underserved areas that may lack a physical bank branch presence.51Nepal has made progress in ensuring the presence of bank branches at all local levels55, but digital channels can further deepen financial inclusion and convenience.

- Persistent issues: Despite this potential, there are significant differences in digital infrastructure (internet connectivity, reliable electricity supply)56and digital literacy58remain serious problems, especially in rural areas. Internet penetration is lower in rural areas.61

- Role models: Initiatives like GeoKrishi, using SMS and offline community clinics (e-Chautari) for agricultural advisory services62, demonstrate models for reaching less connected populations that can be adapted for financial services.

Contributing to financial inclusion

- Entry point into the formal financial system: Digital remittance channels can become an entry point for previously unbanked or underserved populations into the formal financial system.37Receiving money transfers directly to a mobile wallet or bank account encourages further use of the CFS.

- NRB’s focus on financial inclusion: NRB pays special attention to increasing financial accessibility through the Central Financial Services.37

- Existing gap: Despite progress, 18% of the population remains unbanked5, and a significant portion relies on informal financial mechanisms.54

Formalizing remittances through digital channels could lead to more accurate measurement of Nepal’s GDP and foreign exchange earnings, potentially impacting economic policy and international rankings. Historically, a significant portion of remittances, especially from India, have been through informal channels. Digital channels, especially through e-KYC2and traceable transactions, bring these flows into the formal economy. This increased formal inflow will be better reflected in the national accounts25, which will lead to a more accurate picture of the economy’s strength and its dependence on external revenues. This could affect investor perceptions and credit ratings.

While digital channels are increasing accessibility, the last mile problem remains critical. Even if funds are received digitally, converting them into cash or using them for everyday needs in areas with limited digital payment acceptance points can be a hurdle. This highlights the need to develop a holistic ecosystem, not just P2P capabilities. Receiving a remittance on a mobile wallet is convenient.1However, if local merchants in rural areas do not accept QR payments or if the networks of cash pick-up agents are sparse, the usefulness of this digital money transfer is reduced. The success of digital money transfers depends on the wider acceptance and ease of use of DFS for everyday transactions.64This implies the need for banks and PPUs to actively develop retail networks and agency banking, especially in underserved regions.

Table 3: Comparative Analysis of Remittance Channels in Nepal (Traditional and Key Digital Options)

Sources: Synthesis based on general knowledge of these channels, supported by information from fragments discussing the functions of the CFU37and the problems of traditional banking.54Explicit cost/time data for Nepal in the fragments is sparse, so some data may be based on general industry knowledge and presented as ‘typical’ or ‘potential’.

This table clearly illustrates the benefits of digital channels, reinforcing the thesis on the reasons for transformation and highlighting areas where banks can compete or improve.

Opportunities for Commercial Banks in the New Era of Remittances

The digital transformation of the remittance market opens up a wide range of strategic opportunities for commercial banks in Nepal. Adaptation to new realities and active use of innovations will allow banks not only to strengthen their positions but also to enter new market segments, offering customers more modern and in-demand services.

Strategic imperatives: developing and integrating proprietary digital money transfer solutions

Commercial banks need to move beyond basic online transfers to create feature-rich and user-friendly digital platforms for remittances. An example is Nabil Bank’s nBank app, which includes the nRemit feature for international transfers.67The key is to focus on a flawless user experience (UX/UI design) that can compete with the offerings of fintech companies.34Investments in the concept of “smart branches” (Smart Branch)69can complement digital offerings by providing customers with assisted digital services, including for money transfers.

The Power of Collaboration: Fintech Partnerships and Ecosystem Building

Partnering with existing digital wallets and payment system operators (PSOs) can expand their reach and offer integrated services by leveraging the flexibility of fintechs. An example of such collaboration is Global IME Bank’s partnership with IFC to develop digital banking and fintech capabilities.15, as well as NIC Asia Bank’s cooperation with Khalti and Wallyt.14The use of API banking opens up opportunities for third-party integration to create innovative money transfer solutions.2Creating a comprehensive ecosystem that brings together money transfer, bill payment, savings and credit products available through a single platform is becoming a strategic objective.

Product Innovation: Adapting Services for Digital Remitters and Recipients

Banks may offer additional services linked to remittance accounts, such as microinsurance, savings schemes or investment products.73Personalized offers and financial advice based on analysis of remittance patterns and recipients’ needs can significantly increase customer loyalty.75Developing solutions tailored to the specific needs of senders from specific countries or recipient segments is also a promising direction.

Beyond Remittances: Leveraging Digital Channels for Greater Financial Inclusion

Accounts that receive remittances can serve as gateways for offering other banking products (loans, insurance, investments) to previously unbanked or underbanked individuals and their families.37Offering financial literacy programmes alongside digital money transfer services helps build capacity and confidence.40

Data Analytics: Unlocking Customer Information for Competitive Advantage

Using transaction data from digital money transfers to understand customer behavior, preferences and financial needs.67Develop targeted marketing campaigns and personalized product recommendations.75Improving credit scoring models for remittance recipients, potentially opening up access to credit for this category of clients.82

The “unbundling” of banking services by fintechs offering separate payments or remittance products is both a threat and an opportunity. Banks can respond by “reassembling” services in a more customer-centric digital format, with remittances as the anchor product. Fintechs often focus on a specific niche, such as payments (e.g. eSewa, Khalti1). This may attract customers from banks for this particular service. However, banks offer a wider range of products. If banks can create an attractive digital experience where money transfers are seamlessly linked to savings, loans, insurance74and investment opportunities, they will be able to offer a more holistic value proposition that individual fintechs will have a hard time competing with. This requires strong digital platforms and potential partnerships.

The data generated by digital remittances is a largely untapped gold mine for Nepalese banks. Beyond AML/CFT, this data can inform product development, credit risk assessment for the traditionally data-poor segment, and targeted financial inclusion initiatives. Every digital transaction creates a data point.79For remittance recipients who may have limited formal financial history, their remittance inflow patterns can provide valuable information about their financial potential and stability. Banks can use this data (ethically and with consent) to offer pre-approved microloans, individual savings products, or insurance, thereby deepening financial inclusion and creating new sources of income.82This requires investment in data analytics capabilities.

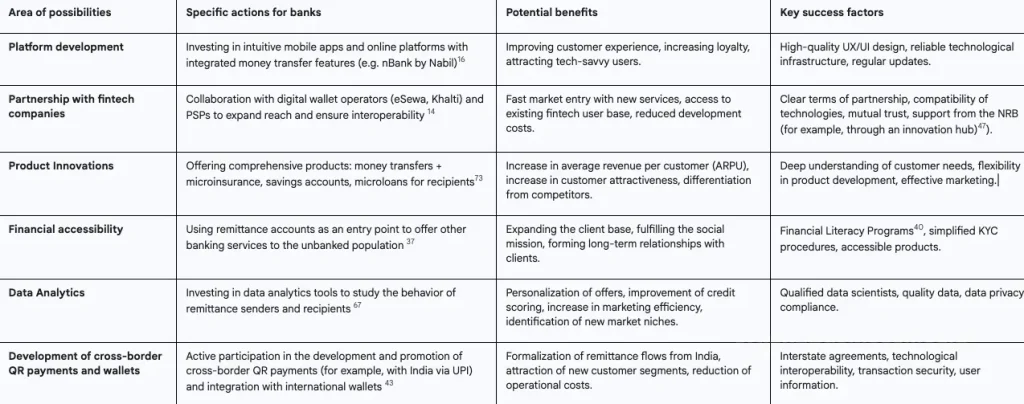

Table 4: Opportunities for Commercial Banks in Nepal’s Digital Remittance Market

This table provides a structured overview of actionable opportunities, directly addressing the core of the user’s query and moving from analysis to strategic directions.

Overcoming Challenges: Obstacles for Commercial Banks

Despite the opportunities, Nepal’s commercial banks face significant challenges in digitizing the remittance market. Successfully navigating this complex environment will require not only technological investment but also strategic flexibility and a deep understanding of changing market conditions.

Increased competition from agile fintech players and digital wallets

Fintech companies like eSewa, Khalti and IME Pay have a large user base and are innovating quickly.30Their lower overhead costs may allow them to offer more competitive pricing. Banks need to match the speed of innovation and quality of user experience offered by these agile competitors. Given that digital wallets are already posing a threat to traditional banking in terms of digital offerings4, their entry into the money transfer market with cheaper and more convenient solutions is a direct competitive threat.

The Cybersecurity Imperative: Protecting Digital Transactions and Customer Trust

The growth of digital transactions increases cybersecurity risks, including phishing, digital fraud and data breaches.87Past incidents in Nepal (Foodmandu hack, Vianet hack, NIC Asia Bank SWIFT hack, NEPS hack) highlight these vulnerabilities.87Building and maintaining customer trust in digital security is of paramount importance.34Banks must actively invest in robust security infrastructure and communicate these measures transparently. NRB releases 2023 Cyber Resilience Guidelines38and rules for the security of digital payments95, compliance with which is mandatory.

Bridging the Digital Divide: Literacy and Infrastructure Challenges

Significant disparities in access to digital technologies and infrastructure remain between urban and rural areas.39Although internet penetration is 55.8%30, a significant portion of the rural population may not have reliable access to the internet or smartphones. Low levels of digital literacy among certain segments of the population, particularly older generations and in rural areas, hinder implementation.23The national financial literacy rate is 57.9%.60Banks need to invest in financial and digital literacy programs, possibly in partnership with local organizations.

Navigating the Changing Regulatory Landscape and the Burden of Compliance

While the NRB encourages innovation, new regulations in the areas of digital financial services, data protection and consumer protection may increase compliance costs and complicate the operations of banks.48The need to comply with AML/CFT rules in a digital context, especially in cross-border transactions, requires sophisticated monitoring systems.48Nepal’s inclusion in the FATF grey list adds to this pressure.48

The problem of digital literacy is not just about knowing how to use an app; it is about understanding digital security risks and managing finances in a digital context. Banks have both a social responsibility and a business interest in addressing this issue, as a more literate customer base is less susceptible to fraud and more likely to use a wider range of digital services. Low levels of digital literacy40makes users vulnerable to fraud.4This not only hurts customers, but also undermines trust in digital platforms, impacting adoption rates across all players, including banks. By investing in digital and financial literacy, banks can create a safer ecosystem, reduce fraud-related losses, and build a more confident customer base for their digital money transfers and other DFS. This could be a key differentiator from less-resourced fintechs.

The “cost of compliance” of new digital regulations, while a burden, can also be a competitive advantage for established banks over smaller fintechs if they can manage it effectively. Strong compliance can enhance trust, which is a key currency in financial services. Fintech startups may face a lack of resources to comprehensively comply with evolving regulations (e.g. AML/CFT, data privacy48). Banks with established compliance departments and experience are better prepared to meet these requirements. If banks can effectively communicate their commitment to security and compliance, this can build customer trust.13, making them the preferred choice for sensitive transactions such as money transfers, despite potentially slightly higher costs compared to some fintech companies.

General Nepalese context: influencing factors

The remittance market transformation in Nepal is not happening in a vacuum. It is significantly influenced by the country’s macroeconomic situation, the unique cultural characteristics of its population, and the monetary policy of the central bank. Understanding these factors is essential for commercial banks to formulate adequate strategies for digital remittances.

Macroeconomic climate: GDP growth, inflation and financial sector stability (NPL)

- Nepal GDP Growth: Forecasts for FY2025 vary: World Bank sees growth at 4.5%96, Asian Development Bank (ADB) – 4.4%98, and the IMF – 4.0%.100The Nepal government has projected growth of 4.61% for FY2024/25.101These moderate growth rates may affect overall economic activity and, as a result, the volume and frequency of remittances.

- Inflation: The NRB’s inflation target is around 5-5.5%.103According to the latest data for mid-April 2025, annual consumer price inflation was 3.39%.105Controlled inflation is important to maintain the purchasing power of received remittances.

- Financial sector stability: The rising level of non-performing loans (NPL) is a concern. The average NPL of commercial banks reached 4.83% in Q3 FY24/25.107The NRB report on financial stability also notes this as a problem area.110High levels of NPLs may impact banks’ creditworthiness and risk appetite, including with regard to investments in new digital money transfer products.

Cultural Dimension: Trust, Word of Mouth and Business Relationships (Afno Manche) in the Digital Age

- Trust: Trust is the cornerstone of Nepalese culture and business.113Digital services must actively build and maintain this trust, particularly in matters of security and reliability.34

- Word of Mouth Marketing (WOMM): In Nepal, WOMM is extremely effective due to strong community ties.11Positive or negative experiences with digital money transfer services will spread quickly.

- Afno Manche Culture: The Afno Manche (literally, “our people”) culture, which emphasizes informal networks and favoritism115, can influence the adoption of digital services if trusted individuals or community leaders endorse them. It can also be a barrier if it leads to resistance to impersonal digital systems. Banks need to understand how to use these networks ethically.

- Hierarchy and communication: Hierarchical structures and indirect communication styles113mean that customer service and marketing of digital money transfers must be culturally sensitive.

NRB Monetary Policy and Its Impact on Digital Finance

- General course: Monetary policy for FY2024/25 is described as “cautiously accommodative”.42Reduction of interest rates (bank rate 6.5%, open market rate 5%)118aimed at stimulating economic activity and lending.

- Lending: Focus on lending to productive sectors, including SMEs and agriculture.42This could indirectly support remittance recipients employed in these sectors.

- Import regulation: Revision of import limits through drafts/telegraphic transfers and documents against payment/acceptance42may affect the outflow of foreign currency, balancing the inflow of remittances.

- Support for the banking sector: Reduction of reserve requirements for “good” loans to 1% as part of the medium-term review of monetary policy121potentially frees up banks’ capital for investment, including in digital technologies.

The situation with high levels of non-performing loans (NPL)103may make banks more risk-averse. This could potentially slow investment in innovative, but perceived risky, fintech projects or new digital money transfer products unless clear ROI and risk mitigation strategies are demonstrated. High NPL levels put pressure on banks’ profitability and capital adequacy.110In such an environment, banks may prioritize strengthening existing loan portfolios and managing distressed assets over investing in new, potentially unproven technologies or remittance partnerships. This creates a contradiction: the market demands digital innovation, but internal financial constraints may limit the ability to deliver it.

Afno Manche Culture116, although often seen as a source of favoritism, can be used positively by banks for digital adoption. Partnering with trusted local leaders or influencers in communities (similar to micro-influencers11) to promote digital remittance services may be more effective than general mass marketing. Nepalese society highly values personal relationships and recommendations from trusted sources.113Instead of viewing Afno Manche solely negatively, banks could identify and engage with respected community figures or local agents who are part of these trusted networks. Their endorsement of a digital money transfer service could significantly accelerate its adoption in their communities, overcoming skepticism about new technologies. This is a culturally-focused application of influencer marketing.

Table 5: Key Macroeconomic Indicators of Nepal (Forecasts/Actual Data for FY2024/25)

This table provides necessary context for the economic environment in which banks operate and make decisions regarding digital money transfer strategies.

Strategic Recommendations for Commercial Banks

With the rapid digitalization of the remittance market in Nepal, commercial banks need to adopt a proactive and innovative stance to remain competitive and seize emerging opportunities. Key policy recommendations are provided below.

Embracing customer-centric digital transformation

- Investments in platforms: Developing and improving user-friendly mobile banking applications and online platforms with seamless money transfer functions, following the example of nBank from Nabil Bank.67Priority should be given to an intuitive user interface (UI) and user experience (UX).34

- Multi-channel support: Providing customer support through various channels (AI-powered chatbots79, social networks, call centers and assistance in branches), focusing on different levels of digital literacy of the population.12

- Personalization: Offering personalized services and products based on analysis of customer data and their money transfer patterns.75

Forming strategic partnerships with fintech companies

- Cooperation: Engage with digital wallet operators and payment service providers (PSPs) to expand reach, ensure interoperability and leverage their flexibility.14

- Specialized services: Exploring partnership opportunities to gain access to specialized services such as AI-powered fraud detection systems82or enhanced e-KYC procedures.

- Innovative environment: Active participation in the work of the NRB Digital Finance Innovation Hub and the regulatory sandbox for testing and joint development of solutions.37

Developing innovative value-added money transfer products

- Complex offers: Offering savings accounts, microinsurance products74, credit products or investment opportunities for recipients linked to remittances.

- Loyalty programs: Implementation of loyalty programs or preferential rates for frequent senders and recipients of money transfers.124

- Targeted solutions: Developing solutions for specific needs, such as paying for education abroad directly or paying for medical services for family members.

Investing in Cybersecurity and Building Trust

- Modern measures: Implementing advanced cybersecurity measures to protect customer data and transactions.87

- Transparency and training: Openly informing customers about security protocols and educating them on secure digital banking practices.

- Compliance with standards: Ensuring compliance with the NRB Cyber Resilience Guidelines38and AML/CFT requirements.48

Bridging the digital divide

- Educational programs: Invest in financial and digital literacy programs, especially in rural and underserved areas.59

- Hybrid models: Considering Hybrid Service Models: Smart Branches69or agent banking networks offering assisted digital money transfer services.

- Infrastructure support: Supporting initiatives aimed at improving digital infrastructure in rural areas.

Using data for strategic advantage

- Analytical capabilities: Invest in data analytics capabilities to understand the behavior and financial needs of remittance senders/recipients.67

- Application of insights: Using the data collected to develop targeted products, personalized marketing and improve credit risk assessment for remittance-dependent households.

Promoting a favourable regulatory environment

- Dialogue with the regulator: Active interaction with the NRB and industry associations (such as FNCCI, CNI117) to develop practical and innovative regulations in the field of digital money transfers.

Banks have the opportunity to position themselves not just as transaction intermediaries, but as “financial wellness partners” for families receiving remittances. They can offer a range of services, from secure receipt of funds to savings, lending, and insurance, all initiated through the digital remittance channel. Remittances are often the primary source of income for recipient families.20Instead of being just a channel for receiving cash, banks can use the digital touchpoint of receiving a remittance to offer integrated financial planning tools, automated savings plans linked to remittances, micro-insurance for family members74or small business loans based on remittance history. This holistic approach leverages the bank’s broader portfolio of services and meets the financial lifecycle needs of these families, creating deeper loyalty than a simple P2P transfer service.

Addressing the Digital Skills Gap23— is not just a corporate social responsibility activity, but a strategic investment for banks. A more digital and financially literate population will be more confident in using digital money transfer channels and other digital financial services, expanding the market for banks. Fear of fraud and lack of understanding are the main barriers to the implementation of digital financial services.4By investing in education, banks can reduce these concerns, increase the pool of potential digital customers, and reduce customer support costs associated with user errors. This creates a positive feedback loop: more literate users lead to more digital transactions, which in turn generates more data and opportunities for banks. In the long term, it can also improve the quality of the human resources available to banks themselves.

Conclusion: The Future of Remittances in Nepal – A Digitally Defined Horizon

The transformation of the remittance market in Nepal, driven by digitalization and fintech innovation, is an irreversible trend. This trend is fueled by technological advancements, regulatory support, and most importantly, changing consumer expectations, especially the “new generation remittances.”

While fintechs have been key catalysts for this change by offering flexible and user-centric solutions, Nepal’s commercial banks are uniquely positioned to not only adapt but also lead in this new landscape. Their established reputation, large customer base, and infrastructure capabilities, if strategically refocused on digital channels and innovative products, can be a powerful competitive advantage.

The future of the remittance market in Nepal is likely to be characterized by deeper collaboration between banks and fintechs, more sophisticated and personalized products, and a greater emphasis on leveraging digital channels to achieve greater financial inclusion. For commercial banks, this means being proactive, innovative, and at all times customer-centric. Success in this dynamic environment will not only ensure their own growth, but will also significantly contribute to a more efficient, inclusive, and sustainable financial ecosystem in Nepal.

The transformation of the remittance market is a microcosm of the broader digital transformation of Nepal’s economy. Success in digitalizing remittances can serve as a model and catalyst for broader adoption of DFS in other sectors. Remittances affect a significant portion of the population.20As users become accustomed to digital channels for this critical financial activity, their confidence and willingness to use DFS for other needs (payments, savings, loans) are likely to increase. The infrastructure, partnerships, and customer behavior models developed for digital remittances can be used for other financial products and services, accelerating Nepal’s overall transition to a digital economy.37

The long-term sustainability of digital remittance models will depend not only on technology and costs, but also on their ability to integrate into Nepal’s socio-cultural fabric. This is especially true in terms of building and maintaining trust through transparent practices and reliable customer support that understands local nuances. Technology is an enabler, but financial services are fundamentally based on trust.11In Nepal, where personal relationships and community ties are strong113, purely transactional digital interfaces may not be enough. Successful digital money transfer providers will need to combine digital efficiency with human-centric support and demonstrate a deep understanding of local customer needs and challenges, including providing support in local languages and culturally sensitive problem solving.12

Sources used

- Financial Technology Adoption in Nepal – Hamzah Academy

- FinTech innovations: Transforming Nepal’s banking landscape – Onlinekhabar English

- Nepal’s Economy at a Crossroads: Can the New Governor Unlock Confidence in the Banking Sector, Lenders and Credit? – || ShareSansar ||

- Digital banking in Nepal: A never-ending blessing or a curse? – OnlineKhabar English News

- Bring Law To Promote Neobanking – The Rising Nepal

- Khalti and IME Pay Merger: A threat to eSewa? – GadgetByte Nepal

- Khalti Digital Wallet app crosses 1 million downloads on Google Play; emerges as one of the preferred digital wallet services within 3 years – || ShareSansar ||

- eSewa Pioneering Digital Payments in Nepal – B360 – Business 360°

- Khalti Marks Seven Years of Digital Transformation with Exciting Anniversary Offers

- Digital payment is changing Nepal – The Kathmandu Post

- Word Of Mouth Marketing: A Great Way People Advertise Digital …

- Customer Satisfaction Score CSAT in Nepal | TCN

- (PDF) Service Quality and Customer Loyalty in Nepalese Commercial Banks: A Mediating Role of Customer Trust – ResearchGate

- NIC Asia Bank partners with Khalti to facilitate digital payments – :: Business 360°

- Global IME Bank Partners with IFC to Advance Digital Banking and Fintech in Nepal

- Nabil Bank conferred ‘The Bankers Technology Award-2025’ – Insurance Khabar

- nBank on the App Store

- agriculture – Investment Board Nepal

- Economy of Nepal – Wikipedia

- The Role of Remittances in Household Spending in Rural Nepal – MDPI

- An Analysis of Causal Relationship between Remittances and Imports in Nepal

- Rs. 1,191 billion remittance received in nine months – The Rising Nepal

- Nepal’s long-term growth may stall below 4 percent, World Bank warns

- Publication: Nepal Development Update, April 2024: Nepal’s Economy on a Recovery Path but Private Investment Remains Low

- Current Macroeconomic and Financial Situation – English (Based on Nine Months Data of 2024/25) – Nepal Rastra Bank

- Nepal Foreign Exchange Reserves, 2002 – 2025 | CEIC Data

- BOP remains at surplus of Rs 210.22 billion in last nine months of current FY

- How economic inequality is driving youths abroad – The Annapurna Express

- Breaking The Cycle Of Brain Drain – The Rising Nepal

- Digital 2025: Nepal — DataReportal – Global Digital Insights

- Digital 2024: Nepal — DataReportal – Global Digital Insights

- datareportal.com

- “Impact of customer satisfaction on commercial banks in Nepal: Insights from a survey-based study” – Business Perspectives

- CUSTOMER EXPERIENCE TOWARDS DIGITAL BANKING – TUCL Repository

- Remittance inflows pose Dutch Disease risk in Nepalese economy – CESLAM

- Symptoms of Dutch Disease in Nepal

- Digital Financial Services in Nepal – International Finance Corporation

- Digital Banking Adoption among Households in Nepal: An Empirical Analysis

- Development in Digital Capitalism: Challenges and Prospects of Nepal

- Adoption of Digital Banking in Nepal: An Analysis of Customer Perceptions and Behaviors

- Nepal records Rs 7.42 billion in remittance outflow in the first nine months – CESLAM

- Monetary Policy for 2024/25 – Nepal Rastra Bank

- QR code drives Nepal’s digital payment boom – The Kathmandu Post

- Digital transactions surge at 210% annually – myRepublica

- Fonepay Sets Record with Over 1 Million QR Transactions in a Single Day

- Fonepay Breaks Records: Over 1 million+ QR transaction in Single-Day – Our Blogs

- Nepal Rastra Bank launches digital finance innovation hub to boost fintech

- IMF Executive Board Completes the Fifth Review under the …

- AML/CFT Directives Archives – the official site of the Central Bank of Nepal

- nBank on the App Store

- FY 2023/24 – Nepal Rastra Bank

- Key Highlights of Nepal’s Monetary Policy for FY 2024/25 – Nepal Economic Forum

- Monetary Policy 2024/25: Bank rate and deposit collection rate lowered – The Rising Nepal

- Access to Financial Services in Nepal – World Bank Open Knowledge Repository

- Taking banking access to rural Nepal – The Annapurna Express

- Why Nepal Struggles to Adopt Better Technology, And Alternative Routes to Development

- Challenges and opportunities for implementing digital health interventions in Nepal: A rapid review – PMC

- Nepal’s Dilemma Over Social Media Regulation – The Diplomat

- Connecting the Unconnected: Bridging the Digital Divide through Grassroot Initiatives in Sri Lanka and Women’s Empowerment in Nepal – NetMission.Asia

- Baseline Survey on Financial Literacy in Nepal

- Nepal: Population Vulnerability and Resilience Profile – U.S. Census Bureau

- 237,3k 51,5k 97% – GSMA

- Foreign exchange reserves surpass Rs 2426 billion – myRepublica

- What is Last Mile? Complete Guide on Challenges & Future Trends – FarEye

- Navigating Last Mile Chaos – Logistics Business® Magazine

- THE IMPACT OF DIGITAL TRANSFORMATION ON BANKING SERVICES AND CUSTOMER EXPERIENCE: A STUDY OF THE NEPALESE BANKING SECTOR – Theseus

- ictframe.com

- Smart Branch Strategy and Enhanced Customer Experience in Banking – Fresh Consulting

- Advanced Self-Service Kiosks: The Path for Branch Transformation – TROY Group

- Branch transformation: 4 strategies to follow – ATM Marketplace

- Digital or Smart Branch – Global Bank Ethiopia

- Wallyt Partners with NIC ASIA Bank to launch WeChat Pay and UnionPay Mobile Payment in Nepal

- In-Depth Analysis of the Economic Situation & Business Opportunities in Nepal. Forecast 2025-2030

- Insurance Benefits of Nabil Dhukka Bachat Khata

- Customized E-Commerce Websites in Nepal: Boost Your Sales | Rewa Soft

- Social Media Marketing in Nepal: Trends & Opportunities

- Influencer Marketing in Nepal: Skyrocket Your Revenue – Digital Gurkha

- The Promise and Challenge of Personalization in E-Commerce – Digital CxO

- The Slow Rise of AI in the Banking Sector: Challenges and Opportunities

- The Use of Artificial Intelligence and Machine Learning in the Nepalese Financial Sector

- Nabil Bank wins ‘The Banker’s Technology Award 2025’ for Asia Pacific region

- Non-performing loans of commercial banks: How AI can revolutionise their management

- NPRC Journal of Multidisciplinary Research Artificial Intelligence in Microfinance: Enhancing Customer Experience at ESAF Bank

- Himalayan Bank Bancassurance

- “If I were a fintech entrepreneur in Nepal, I would start by mapping out the existing fintech landscape’ – B360 :: Business 360°

- Transaction Limits – Fees, Limits & Types – Khalti

- Sensitive Data of Nepal’s PM’s Office Allegedly for Sale – Cyber Press

- April 2025: Major Cyber Attacks, Ransomware Attacks and Data Breaches

- Global law enforcement action in Asia nets large infrastructure seizure, 32 arrests

- A brief study into Cyber attacks and preventive measures in Nepal – ResearchGate

- Nepal’s Digital Frontier: How Safe Are We from Cyber Attacks? – myRepublica

- Nepal Cybersecurity Job Market: Trends and Growth Areas for 2025

- Data Breaches in Nepal: Understanding the Risks and Solutions – myRepublica

- Enhancing Customer Satisfaction in Nepalese Banks and Financial Institutions: The Influence of Service Quality on Different Dim – ResearchGate

- NRB Introduces New Rules for Digital Payment Security – Beemapost.com

- Nepal’s Economy Expected to Remain Resilient in Face of Economic Shocks, says World Bank

- World Bank projects Nepal’s economic growth at 4.5 percent – myRepublica

- Nepal’s Economy Will Likely To Grow By 4.4 In Fiscal Year 2025: ADB

- ADB: Nepal To Grow By 4.4 Percent | New Spotlight Magazine

- Nepal and the IMF

- FinMin Presents Economic Survey, Projects 4.61pc growth for current FY

- Nepal expects 4.61-pct growth for 2024-25 – Xinhua

- Nepal: Fourth Review Under the Extended Credit Facility Arrangement-Press Release; Staff Report; and Statement by the Executive Director for Nepal in: IMF Staff Country Reports Volume 2024 Issue 225 (2024) – IMF eLibrary

- NRB’s Third Quarter Monetary Policy Review: Risk Weight on Share Mortgage Loans Reduced From 125% to 100%, Foreign Reserves Strengthen – || ShareSansar ||

- Nepal Inflation Rate – Trading Economics

- Macroeconomic Snapshot of 9 Months: Inflation at 3.39%; Foreign Reserves Reach USD 17.63 Billion; Remittance Surges 10% – || ShareSansar ||

- Delving into Q3 2081/82: Performance Analysis of Leading Commercial Banks with Key Financial Insights – || ShareSansar ||

- Banks set aside Rs 35.07bn for loan losses in Q3 | The Annapurna Express

- Non-Performing Loans of Commercial Banks Reach 4.83% in Q3 of FY 2081/82

- Increasing NPL and accumulation of non-banking assets are major challenges of banks: NRB – myRepublica

- Nepal Rastra Bank, Financial Stability Report 2024

- Financial Institutions Supervision Report – 2023/24 – Nepal Rastra Bank

- Cultural Considerations in Nepal – Rivermate

- Social Media Marketing and Brand Awareness of Customers: Evidence from Nepal

- A Guide to Business Etiquette in Nepal | ClickUp™

- Afno Manche | PDF | Social Network – Scribd

- Accommodative Monetary Policy to spur the economy – The HRM Nepal

- NRB unveils mid-term monetary policy review, Slashes loan …

- Nepal Policy Rate, 2003 – 2025 | CEIC Data

- Nepal Interest Rate – Trading Economics

- Monetary policy mid-term review: policy rates maintained at 5 pc, vehicle loan ratio lowered to 60 pc – Business 360°

- NRB monetary policy review: Current account at surplus of Rs 210.22bn, BOP at surplus of Rs 346.23bn – Business 360°

- Contact Customer Care – nic asia support

- Fonepoints x IMS Software: Redeem Discounts Instantly at 20000+ Counters Across Nepal

- Loyalty Meets Lifestyle: Discover Fonepoints Rewards in Nepal

- Loyalty App – Himalayan Java Coffee – Nepali Coffee Brand

- Rewardiz – Loyalty App & Digital Rewards Platform – Nepal

- NIES:-Nepal International Economic Summit 2025 – FNCCI

- At FNCCI’s 59th AGM inauguration, PM Oli emphasises collaboration with private sector for rapid development – Business 360°

- Budget formulation at final stage – The Rising Nepal

- NRB governor pledges to align monetary policy with fiscal goals – myRepublica

- NEFport 60 by Nepal Economic Forum – Issuu

- 38176-015: Skills Development Project | Asian Development Bank

- Current Macroeconomic and Financial Situation of Nepal