Navigating the 2025 Global Economy in an Uncertain World

In 2025, the global economy enters a qualitatively new stage of its development, which the International Monetary Fund (IMF) characterizes as a “new era” (1). This period is marked by unprecedented levels of uncertainty, with economic trajectories becoming increasingly intertwined with geopolitical dynamics and fundamental shifts in international politics. Investors will have to navigate a complex landscape, balancing the risks generated by growing geopolitical fragmentation with the opportunities created by structural economic transformations and technological breakthroughs. As Deloitte analysts note, numerous elections around the world and subsequent changes in policy courses in leading countries could have a significant impact on inflation expectations, borrowing costs, exchange rates, as well as global trade and capital flows (2).

After a period of relative stabilization following a series of powerful global shocks, the world economy has been showing what the IMF called “disappointing growth” (3). However, in 2025, the situation will again become more complicated due to the change in political priorities in key economies and the escalation of trade contradictions. This shift in the focus of risks – from reactions to external events to the consequences of targeted political actions, especially in the area of international trade and geopolitics – requires investors not so much to assess the overall resilience to shocks, but rather to be able to predict and adapt to changing “rules of the game”.

The current moment is rightly characterized as “critical” (3). This is not just a rhetorical figure, but an indication of a potential bifurcation point. On the one hand, the cumulative effect of delayed structural reforms, accumulated debt burden and new geopolitical tensions could push the global economy into protracted stagnation. On the other hand, provided adequate and coordinated political decisions are made, there is a chance to form a new, more sustainable model of global economic growth. In these conditions, flexible investment strategies based on a deep understanding of the interrelations between politics, economics and financial markets, as well as the ability to identify countries and regions that are taking the necessary steps to adapt and develop, are of paramount importance.

Global Economic Landscape 2025: Divergence and Subdued Growth

A. GDP Growth Forecasts: Uneven Recovery and Regional Contrasts

Forecasts for the global economy in 2025, presented by leading international financial institutions and analytical agencies, paint a picture of subdued and uneven growth. The general trend is either a slowdown in the recovery rates observed earlier or stabilization at relatively low levels, with the escalation of trade wars and protectionist measures becoming a significant factor influencing the forecasts.

Thus, the IMF’s April forecast for 2025 indicates a decline in global growth to 2.8% (5), which represents a significant decline from the January estimate of 3.3% (4), primarily due to the introduction of new trade tariffs. The World Bank, in its January report, “Global Economic Prospects” expects global economic growth to be 2.7% in 2025 and 2026, in line with 2024 growth rates (8). The Organisation for Economic Co-operation and Development (OECD) in March 2025 forecast a slowdown in global growth to 3.1% in 2025 (10). The most pessimistic forecast is given by the Fitch agency, which, due to the escalation of the trade war, lowered its estimate of global GDP growth in 2025 to less than 2% (12). S&P Global analysts expect global real GDP growth to be 2.2% in 2025 (14), PwC predicts 2.6% (16), and EY – 3.1% (17).

Table 1: Summary GDP growth forecasts for key regions and countries in 2025 (%)

Sources: Data are aggregated from IMF reports (4), World Bank (8), OECD (10), Fitch (13), S&P Global (14), PwC (16), EY (17), Deloitte (18), Morgan Stanley (19), KPMG (20). Note: Some forecasts are regional or not detailed to specific countries in the materials provided.

Such a wide range of forecasts, especially for the US and the global economy as a whole, reflects the high degree of uncertainty that is inextricably linked to US trade policy. Fitch Ratings, giving the most pessimistic estimate (less than 2% for global GDP), directly links this to the escalation of trade wars (12). Similarly, the sharp reduction in the IMF forecast in April was also due to tariff policy (6). This highlights the fact that in the current environment, it is geopolitics, and in particular trade conflicts, that are the key factor determining economic prospects, and not the other way around. Investors should primarily monitor trade relations and tariff policy, as this is where the main source of uncertainty and potential further deterioration in forecasts lies.

Amid a slowdown in China and instability in developed countries, robust growth in India and some other emerging markets such as Southeast Asian countries (1), may signal a continuing, albeit more fragmented, shift in the global economic center of gravity. So-called “connector economies,” which are able to build trade links between different geopolitical blocs, are gaining additional advantages (17). This implies that investment strategies focused solely on traditional growth centres may be less effective, and a more detailed analysis of individual emerging markets that are able to adapt to and benefit from the new geo-economic reality is required.

At the same time, developing economies as a whole face a “more difficult path,” as the World Bank notes (8). Their traditional growth drivers are weakening, while new challenges – high debt levels, the impacts of climate change, weak investment and productivity growth – are mounting. This poses long-term risks to global growth, especially given that emerging markets account for about 60% of global economic growth (8). Therefore, even if current growth forecasts for these countries look relatively optimistic, the longer-term outlook may be clouded by structural issues, requiring investors to take a deeper look at country risks and the sustainability of development models.

B. Inflation Dynamics: Persistent Pressures and Monetary Policy Dilemmas

The outlook for global inflation in 2025 remains challenging. While most forecasts point to a general trend of lower inflation pressures compared to the peaks of previous years, inflation in many countries, particularly core inflation, is expected to remain above central banks’ targets.

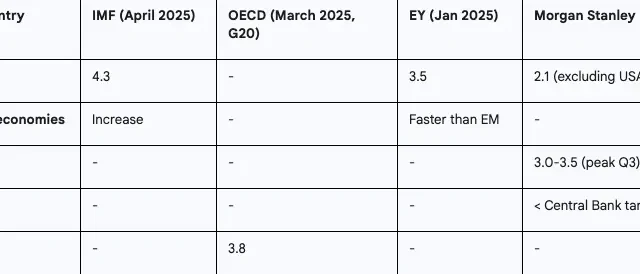

The IMF’s April forecast for global inflation in 2025 is 4.3%, falling at a slightly slower pace than expected in January. The fund notes a notable upward revision to its forecasts for advanced economies (5). The OECD also forecasts that inflation will be higher than previously expected, although it will continue to decline moderately; annual inflation in G20 countries is expected to reach 3.8% in 2025, with services inflation remaining elevated (10). EY analysts expect global inflation to decline to 3.5% in 2025, which is still above the pre-pandemic level of 3.1% in 2019 (17). Morgan Stanley forecasts global inflation (excluding the US) to slow to 2.1% in 2025, but the US is expected to accelerate to a peak of 3-3.5% in the third quarter of 2025 due to tariffs and immigration restrictions (19).

Table 2: Consolidated inflation forecasts for key regions for 2025 (%)

Sources: Data are aggregated from IMF reports (5), OECD (10), EY (17), Morgan Stanley (19). Note: Not all organizations provide detailed forecasts for all regions in their brief overviews.

The key factor supporting inflationary pressures are trade tariffs, which most analysts view as a pro-inflationary shock (1). Deloitte, for example, notes that the inflationary effect of tariffs will likely prevent the US Federal Reserve from cutting interest rates in 2025 (18). The OECD models that further tariff increases could push global inflation up by 0.4 percentage points a year (11). Tightness in labor markets also continues to support inflation in the services sector (10).

In this environment, central banks face a difficult dilemma: the need to combat inflation caused by supply shocks (such as tariffs) with standard monetary policy tools that primarily affect demand could worsen the economic downturn. This is especially true for the United States (18). If economic growth is already slowing due to the tariffs themselves and the associated uncertainty (6), then further tightening of monetary policy to combat “tariff inflation” could increase recessionary risks. Morgan Stanley (19) suggests the Fed will likely be more focused on containing inflation than on supporting employment for the rest of the year. That suggests the Fed is willing to slow economic growth to control prices, leaving investors at risk of a deeper downturn than its baseline scenarios suggest.

The divergence of inflation trends between developed countries (where service inflation and the impact of tariffs may be more pronounced) and developing economies (where the decline in inflation may be more noticeable, but pockets of high inflation remain in individual countries), as noted by Triodos (29) for Bolivia, Ghana and Turkey) creates both opportunities for interest rate arbitrage and the implementation of various currency strategies, and risks of unexpected shocks. The “stickiness” of core inflation above the target levels of central banks (10), particularly in developed countries, could mean that the period of high interest rates will last longer than markets expect. This will have a negative impact on the valuations of risk assets such as growth stocks and real estate, and will also increase the cost of servicing debt for governments and corporations.

C. Global Trade and Labor Markets: Adapting to New Realities

The state of global trade in 2025 is a matter of grave concern. Protectionism and geopolitical fragmentation are leading to a sharp slowdown in the growth of trade flows, and in some scenarios, to their reduction. Thus, the IMF’s April forecast for 2025 assumes growth in the volume of world trade in goods and services by only 1.7% (1), which is a significant decrease compared to the January forecast of 3.2% (30). The World Trade Organization (WTO) is even more pessimistic, forecasting a 0.2% decline in global merchandise trade in 2025, with North American exports potentially falling by 12.6%. In a worst-case scenario, with trade tensions escalating, the decline could be 1.5%. The WTO has also revised down the growth of services trade to 4.0% (31). The World Bank, by contrast, expects global trade growth to be around 3.1% in 2025-26, but acknowledges that this is below pre-pandemic averages and that the number of new trade restrictions in 2024 was five times the 2010-2019 average (8). Such a sharp divergence in forecasts highlights the extreme uncertainty and sensitivity of this sector to political decisions.

Labour markets are generally resilient, particularly in developed countries, where the OECD has cited tightness as a factor supporting services inflation (10). According to OECD data for March 2025, the unemployment rate in member countries remained stable at 4.9% (34). However, the global picture looks less optimistic. In May 2025, the International Labour Organization (ILO) revised its forecast for global job creation downwards by 7 million (from 60 to 53 million), expecting global employment growth to decline from 1.7% to 1.5%. The ILO also points out that about 84 million jobs in 71 countries are directly or indirectly linked to U.S. consumer demand and are at risk due to trade tensions (30). This suggests that the global labor market may not be as resilient as it seems, especially if trade wars lead to a decline in consumer activity in the US. The IMF’s unemployment forecasts for 2025 (based on WEO DataMapper data as of April 2025) for some key countries are: US – 4.2%, Eurozone – 6.4%, China – 5.1%, India – 4.9% (36).

Long-term structural changes in the labour market, such as an aging population, the impact of artificial intelligence and growing educational mismatch (3), are exacerbated by short-term geopolitical shocks. This creates a challenging environment for investment in human capital and requires more adaptive strategies from companies and governments. Disruption of migration flows due to political decisions (1), accelerating automation to reduce reliance on global supply chains, and worsening skills shortages are all consequences of the current turbulence. For investors, this means that companies that can effectively manage talent, invest in reskilling, and adapt to technological change amid geopolitical turbulence will have a significant competitive advantage.

Geopolitical Crucible: Key Challenges for Investors in 2025

A. Escalation of Trade Wars and Protectionism: Impact on Global Markets (Especial Focus on US-China Relations)

Escalating trade wars and rising protectionism, particularly in the context of tensions between the US and China, are the dominant challenge for the global economy and investors in 2025. The actions of the US administration, including the imposition of both general and specific import tariffs, have become a key source of uncertainty and risk (1). The IMF, in its April 2025 review, described the U.S. tariffs as raising effective rates to levels “not seen in a century” (1). While analysts at S&P Global see some easing of tariff-related risks following partial rollbacks, they stress that these risks have not gone away and the damage to confidence is likely to persist (14). The CEPR study shows that even a partial suspension of tariffs would lead to a sharp decline in trade volumes and significant welfare losses, especially for the US itself (26).

In response to the US measures, China and other countries are imposing retaliatory tariffs (1), which contributes to the fragmentation of world trade and the formation of competing economic blocs (17). EY describes this situation as “derisking in a fragmented universe” (17), and KPMG talks about “tectonic shifts in power centers, economic centers and trade” (42). A World Economic Forum poll found that 100% of chief economists surveyed expect the global economy to weaken due to U.S. trade policy and shifting global alliances (24).

The economic consequences of such policies are multifaceted. First, there is the direct decline in GDP: the IMF has lowered its global growth forecast by 0.8 percentage points because of the tariffs (6), and the OECD models a 0.3% drop in global GDP with further tariff increases (11). Secondly, there is the growth of inflation due to the increase in costs for producers and prices for consumers (10). Thirdly, this is the reduction in the volume of world trade predicted by the IMF and the WTO (1). Finally, there is high uncertainty for business (1), which is holding back investment and consumer spending. According to SHRM, 29% of CEOs see decoupling from China as the top geopolitical risk to their operations (41). Particularly vulnerable are sectors that are highly integrated into global value chains, such as electronics and transport equipment (26).

Table 3: Key geopolitical risks in 2025 and their potential economic impact

It is important to understand that the “trade war” is not just a question of tariffs. It also encompasses the fight for technological dominance, especially in artificial intelligence, as well as control over critical resources and infrastructure such as the Panama Canal (41) or deposits of rare earth metals (37). This means that the conflict has deeper roots and is likely to be more prolonged and multifaceted than just trade balance disputes. Investors need to consider not only the direct economic costs of tariffs (lower GDP, higher inflation), but also the indirect ones – through the “trust effect” (25). This effect could lead to delayed investment, lower consumer spending, and increased volatility in financial markets, even if actual tariffs are lower than originally announced.

While direct trade flows between the U.S. and China could be sharply reduced by tariffs, much of it will likely be rerouted through third countries – so-called “connector economies” (17). This will make global supply chains more complex, less transparent and potentially more expensive, but will not lead to complete “decoupling”.

B. Hot spots and conflicts: Regional instability with global implications (Ukraine, Middle East, Africa, Asia)

In addition to trade wars, a number of regional conflicts and hot spots continue to have a destabilizing effect on the global economy in 2025. The war in Ukraine continues to affect energy security (46), food markets (although the impact on some sectors is believed to be47, was partially offset by the adaptation of other producers) and regional stability in Europe (49). Attacks on Ukraine’s energy infrastructure and cuts in foreign aid are exacerbating the country’s humanitarian and economic hardships (46). The Stimson Center views the risks of a “bad deal” or the US withdrawing from the settlement process as significant (37).

Tensions remain high in the Middle East (17), posing risks to energy supplies and global trade, especially through the Suez Canal. Steptoe analysts highlight the danger of a collapse of the ceasefire in Lebanon and a power vacuum in Syria as potential triggers for further destabilization (48).

There are numerous conflicts in Africa, such as in the Democratic Republic of Congo and Sudan (48), as well as instability in the Sahel region (50), create humanitarian crises, create risks to the supply of raw materials (including rare earth metals, gold, gum arabic) and undermine regional stability (53). The Brookings Institution highlights the importance of Africa as a source of critical minerals and as an arena of competition between the US and China (51).

In Asia, tensions rise over Taiwan (17), disputes in the South China Sea (48), the situation on the Korean Peninsula (37), as well as the civil war in Myanmar (48) and Indo-Pakistani tensions in Kashmir (48) pose risks to global technology supply chains (especially semiconductors) and regional security. The overall rise in global instability is supported by Wellington Management’s data on 59 “active military conflicts” worldwide, the highest number since World War II (50).

It is important to note that the so-called “forgotten” or “smoldering” conflicts (48) carry significant escalation potential and can have unexpectedly significant impacts on the global economy. Investors often focus on headline news stories, missing other potential “black swan” events that could disrupt commodity supplies or destabilize entire regions. In addition, the links between conflicts and climate change are growing (50). Climate change exacerbates resource scarcity and migration, which can fuel conflicts, which in turn make it more difficult to combat and adapt to climate change, creating a vicious cycle and long-term systemic risks. Finally, the rise in conflicts is driving increased defense spending in many countries (19), which, on the one hand, can divert resources from productive investments, and on the other hand, create specific investment opportunities in the defense sector and related industries.

C. The Relationship between Geopolitics and Economic Stability: Supply Chains, Energy Security, Sovereign Debt

Geopolitical factors in 2025 have a direct and often destructive impact on key aspects of economic stability, including global supply chains, energy security and sovereign debt levels.

Supply chains are becoming increasingly fragmented and vulnerable. This is a result not only of trade wars, but also of regional conflicts, as well as the strategic desire of countries to “derisk” and reduce their dependence on potentially unreliable suppliers (17). Company leaders are actively planning changes in their supply chains to reduce risks and costs (41). SupplyChainDive expects another year of geopolitical upheaval affecting logistics (56), while Global Banking & Finance Review points to fluctuating oil prices, unpredictable inflation and changing trade policies as factors fundamentally altering the cost structure of global supply chains (39). Derisking and friend-shoring strategies, while intended to enhance resilience, may lead to duplication of investment, reduced overall efficiency and, paradoxically, to the emergence of new forms of dependency and vulnerability, as well as increased inflationary pressures in the medium term (43).

Energy security has come to the forefront of many countries’ agendas due to ongoing conflicts, particularly in Ukraine (46) and in the Middle East, as well as due to sanctions and the reorientation of global energy flows (7). Analysts at Resources for the Future (RFF) note that energy markets are undergoing profound changes (57). Shell’s scenarios consider options in which the development of energy technologies is hampered by problems with access to resources and trade security (7). Pursuit of energy security through diversification of sources and development of renewable energy (29) creates significant investment opportunities. However, this process also faces geopolitical obstacles, such as competition for critical minerals needed for green technologies and protectionist measures aimed at protecting domestic producers. Thus, the energy transition is becoming not only a technological and economic challenge, but also an arena for geopolitical rivalry.

Sovereign debt poses a growing threat to global economic stability. Global sovereign debt, particularly in developing countries, continues to rise amid rising interest rates, slowing economic growth and general geopolitical uncertainty, increasing the risk of debt crises (6). According to Clairinvest, citing the OECD, global debt could exceed $100 trillion in 2025, with 50% of OECD and major emerging market debt set to be refinanced by 2027 at significantly higher rates (58). The IMF predicts that global public debt could reach 100% of global GDP by the end of the current decade (59). The Stimson Center notes that 3.3 billion people live in countries that spend more on debt servicing than on health care and education (37). This growing crisis is exacerbated by geopolitical instability, which is restricting access to finance, increasing risk premiums and reducing the willingness of creditors to restructure debt. This could lead to a “lost decade” for many poor countries and create the risk of cascading defaults or prolonged periods of stagnation, which in turn would negatively affect global demand and could increase migration pressures and social instability.

Investment Opportunities in a Changing World: Strategies for 2025

A. Strategic Asset Allocation in Volatility Conditions

In the context of increased volatility and uncertainty that characterizes 2025, strategic asset allocation is of paramount importance. Diversification, selectivity and flexibility are key principles (28). HSBC analysts highlight the value of quality equities, high-quality credit instruments and alternative investments such as hedge funds and private credit (55). Franklin Templeton recommends a comprehensive portfolio approach that includes alternative and thematic investment ideas to complement traditional stock and bond portfolios (60).

There is an interesting divergence of views on the attractiveness of U.S. stocks. Traditional investment giants such as Goldman Sachs (65) и BlackRock (45), continue to favor the US market, citing its resilience and growth potential. At the same time, other experts, such as those from HSBC (55) and partially UBS (67), point to opportunities for diversification and a potential weakening of the US dollar, which could increase the attractiveness of other markets. Morgan Stanley also forecasts a significant depreciation of the dollar (69). This divergence is critical for investors, as the choice between continuing to bet on “American exceptionalism” or aggressively diversifying is a key strategic decision in 2025.

Growing interest in “quality” stocks (55) and alternative assets such as private credit and hedge funds (55), appears to be more than just a tactical maneuver, but a structural shift. It is a response to increased macroeconomic volatility and the declining reliability of traditional bonds as a diversification tool, as BlackRock points out (62). Classic 60/40 briefcase (61) is increasingly being questioned, and investors are actively looking for new ways to protect against risks and generate income.

Institutional investors are showing caution but also a willingness to seize opportunities. State Street data shows that risk appetite has stabilized in April 2025 after some jitters in March, with capital flowing out of stocks and cash into bonds, and out of the U.S. dollar into the euro (72). Adams Street Partners surveys (70) and Commonfund (71) indicate continued optimism about private equity, private credit, and venture capital, despite concerns about inflation and geopolitical risks. Notably, investor enthusiasm for ESG investing has waned in some markets (70), which could lead to a shift of capital into other “thematic” areas such as AI or infrastructure, which are perceived as less politicized and more pragmatic in the current environment.

B. Promising sectors: Technology (AI), healthcare, energy transition

Despite overall economic challenges, a number of sectors demonstrate significant growth potential in 2025, driven by long-term structural trends.

Technology and Artificial Intelligence (AI) remain a key driver of growth and investment interest. The OECD describes AI as a unique opportunity to revive productivity (10). Moody’s expects that in 2025, AI model developers will compete on new capabilities, making the technology more accessible and opening up new use cases, including autonomous AI agents (74). The emergence of cost-effective AI models such as DeepSeek in China is changing the technology landscape, reducing computing costs and accelerating AI adoption, which is particularly beneficial for the software and internet platform sectors (55). BlackRock calls AI a “mega-force” that could fundamentally change the economy (45), and UBS sees AI as a key driver of stock market returns (67). The AI ”arms race” between the US and China (41) will spur massive public and private investment, creating both opportunities for corporate growth and the risks associated with technology nationalism.

Healthcare continues to attract investors thanks to demographic trends (aging population) and technological innovations, including the use of AI. Aberdeen notes that the integration of AI into cancer research could lead to unprecedented advances, and healthcare stocks linked to AI and biotech should perform well (75). UBS highlights the topic of “Longevity” as one of the key ones, with a market opportunity of 2.2 trillion by 2030 (67). Synergy between AI and healthcare (67) has the potential to revolutionize approaches to disease treatment and drug development, opening up long-term investment horizons.

Energy Transition and Infrastructure also remain in focus. Investments in renewable energy, grid modernization and related infrastructure are relevant despite political uncertainty. Guidehouse points out that utility priorities include grid resilience, cybersecurity and digitalization (76). Triodos notes strong global demand for clean energy and growing investment in resource-rich emerging markets (29). UBS highlights that rising demand for electricity due to AI, electric vehicles and industrial electrification is creating opportunities across the electrification value chain (67). BlackRock estimates the required investment in the energy transition at $3.5 trillion per year in the current decade (45). The need to modernize and improve the resilience of energy infrastructure is becoming increasingly urgent not only due to climate goals, but also due to growing demand from new technologies and geopolitical risks for traditional energy sources, which creates a strong demand for investments in smart grids, energy storage and cybersecurity.

C. Regional Outlook: Resilience and Growth in Selected Emerging Markets (e.g. India, Mexico, Southeast Asia)

Amid global economic divergence, individual emerging markets (EMs) are showing potential for outperformance, attracting investor attention.

India stands out as one of the most promising markets. GDP growth forecasts for 2025 range from 6.2% (World Bank for South Asia8) to 6.4% (EY 17, OECD10) and “more than 6%” (PwC16). Analysts note strong domestic demand, benefits from the status of a “connector economy” (17), the Modi government’s prioritization of foreign investment and the potential from the AI boom and US-China decoupling (77). Franklin Templeton says “recovery is imminent and long-term prospects are compelling” (60).

Mexico benefits from the “nearshoring” trend (moving production closer to sales markets) and the USMCA (US-Mexico-Canada) trade agreement. EY classifies it as a “connector economy” (17), and Nomad Capitalist notes a boom in the manufacturing sector, particularly in the automotive and electronics industries (77). Triodos points to improvements in the country’s renewable energy infrastructure (29).

Countries of Southeast Asia (SEA) continue to attract foreign investment and benefit from diversified global supply chains. The IMF notes that Asia as a whole can improve economic resilience by strengthening regional ties (1), and EY names Southeast Asia as a leading destination for foreign direct investment among emerging markets (17).

Other emerging markets such as Georgia, Türkiye, Colombia and Kazakhstan, may also be of interest due to specific factors such as tourism development, strategic location, reforms, investments in AI and technology, and the availability of natural resources (77). The World Bank also notes growth potential in sub-Saharan Africa (4.1%) and the Middle East and North Africa (3.4%), provided reforms are implemented and opportunities for cross-border cooperation are taken advantage of (8).

The success of individual emerging markets will depend heavily on their ability to position themselves as reliable partners in the context of geopolitical fragmentation and to attract investment in new economic sectors (technology, green energy), rather than just on traditional factors such as cheap labor or availability of raw materials. The growth of large emerging markets such as India may partially offset the slowdown in China and developed countries, but global growth will still remain subdued due to the overall impact of protectionism and geopolitical uncertainty. Competition for investment and markets among emerging countries themselves will intensify, and countries that fail to adapt to new requirements (sustainability, technology, reliability) risk being left behind.

D. Analysis of investor sentiment and its impact on markets

Investor sentiment in 2025 is characterised by a complex mix of caution driven by geopolitical risks and inflation concerns, and optimism about specific sectors such as private markets and technology innovation.

Surveys of institutional investors paint a mixed picture, with Adams Street Partners finding growing optimism about a recovery in private markets activity, with inflation (86% of LPs), interest rates (83%) and geopolitical risks (83%) remaining the top concerns (70). A Commonfund survey found that institutional investors are split on the outlook for the U.S. economy (22% bullish and 22% bearish), with 68% expecting U.S. stock market returns to be weaker or negative. The top concerns are a trade war over tariffs (56%), geopolitical tensions (51%), and inflation/rates (43%). However, optimism remains around private markets and AI (71).

State Street data suggests institutional risk appetite has become balanced in April 2025 after some jitters in March. There has been an outflow of capital from stocks and cash into bonds, as well as from the US dollar into the euro, which could indicate a defensive stance and an expectation of further volatility (72).

Consumer confidence also remains under pressure. The Ipsos Global Consumer Confidence Index for May 2025 remained muted at 47.4, with the investment sub-index down (78). In the U.S., consumer confidence rebounded somewhat in May after five months of decline, according to the Conference Board, but experts worry that the optimism may be short-lived because of the potential impact of tariffs on prices (79).

This phenomenon, where soft data (sentiment surveys) signal a possible downturn before hard economic data reflects it, is sometimes called a “vibecession.” Consumer and business concerns, fueled by political uncertainty and tariff anxiety, can become a self-fulfilling prophecy, negatively affecting consumer spending and investment decisions even before the macroeconomic data actually worsens (27). A cautious stance by institutional investors, reflected in a move towards bonds and alternative currencies such as the euro, as well as gold (28), signals an expectation of continued volatility and potential negative surprises, which could limit upside for broad equity markets. The divergence between institutional caution and potentially more optimistic (or speculative) retail investor sentiment (such as the interest in cryptocurrencies noted by Commonfund71) can create pockets of irrational behavior in the market and increase volatility.

Conclusion: Formation of an investment portfolio in the era of transformations

The global economy in 2025 presents a complex kaleidoscope of challenges and opportunities, dominated by geopolitical uncertainty, particularly in international trade. Global growth forecasts remain muted and uneven, and inflationary pressures, while easing, may remain persistent, posing dilemmas for central banks. Global trade and labor markets are adjusting to the new realities of protectionism, technological shifts, and demographic changes.

Key challenges for investors center around the escalation of trade wars, especially between the US and China, which pose risks of lower global GDP, higher inflation and disruption of supply chains. Regional conflicts and “hot spots” in different parts of the world add another layer of uncertainty, affecting energy markets, food security and logistics. The interrelationship of geopolitics with such fundamental aspects of economic stability as the resilience of supply chains, energy security and sovereign debt levels is becoming increasingly clear and requires close attention.

Despite these challenges, 2025 also presents investment opportunities. In an environment of heightened volatility, strategic asset allocation, diversification, and active risk management are key. Investor interest is shifting towards quality assets, alternative investments, and selected growth sectors. Technology, especially artificial intelligence, continues to be a strong growth driver, opening up new horizons in various sectors, including healthcare. The energy transition and the need to modernize infrastructure also create long-term investment themes. At a regional level, individual emerging markets such as India, Mexico, and Southeast Asia are showing resilience and growth potential, thanks to domestic factors and the benefits of global economic restructuring.

An analysis of investor sentiment suggests caution prevails, but also a willingness to seize emerging opportunities, particularly in private markets and innovative sectors.

Ultimately, building an investment portfolio in 2025 requires investors to not only deeply analyze economic data, but also understand complex geopolitical processes. Flexibility, the ability to adapt to rapid changes, careful selection of assets and regions, and a focus on long-term structural trends will be the key to success in this era of global transformation. Constant monitoring of geopolitical events and policy decisions of leading countries will be crucial for timely adjustment of investment strategies and navigation in these turbulent but potentially fruitful waters of the global economy.

Source used

- The Global Economy Enters a New Era – International Monetary Fund (IMF)

- Global economic outlook, January 2025 – Deloitte

- World Economic Outlook, April 2025: A Critical Juncture amid Policy …

- World Economic Outlook – All Issues – International Monetary Fund (IMF)

- IMF Published the Global Economic Outlook Report for April 2025 – Ministry of Trade

- World Economic Outlook, April 2025; A Critical Juncture amid Policy …

- The 2025 Energy Security Scenarios | Shell Global

- Global Economy Stabilizes, But Developing Economies Face …

- Ayhan Kose Explains the January 2025 Global Economic Prospects – World Bank

- Global economic outlook uncertain as growth slows, inflationary pressures persist and trade policies cloud outlook – OECD

- OECD Economic Outlook, Interim Report March 2025 | OECD

- agroreview.com

- Fitch downgrades global GDP growth forecast for 2025 – AgroReview

- Global Economic Outlook: May 2025 | S&P Global

- Global economic outlook: April 2025 – S&P Global

- Economic Outlook 2025 – PwC

- 2025 global economic outlook: momentum and uncertainty | EY – US

- US Economic Forecast Tariffs | Deloitte Insights

- Global Economic Outlook 2025: A Widespread Growth Slowdown | Morgan Stanley

- KPMG Economics

- Global Economic Prospects – January 2025 [EN/AR/RU/ZH] – World – ReliefWeb

- US economic outlook May 2025 – EY

- How Tariffs and Geopolitics Are Shaping the 2025 Global Economic …

- Shifting ‘superfundamentals’ shake up global economic outlook

- April 2025 update to TIGER: The world economy shudders and could stall

- Roaring tariffs: The global impact of the 2025 US trade war | CEPR

- Introducing the RSM US Recession Monitor

- Asset Allocation Committee Outlook – Neuberger Berman

- Emerging markets adapting to a changing world order – Triodos Investment Management

- Global employment forecast downgraded by up to 7 million jobs in …

- WTO sounds alarm on trade risks and other trade news | World …

- Global trade set for mild contraction in 2025, reveals WTO report – Gulf Business

- bit.ly

- Unemployment Rates, OECD – Updated: May 2025

- World Employment and Social Outlook: May 2025 Update

- World Economic Outlook (April 2025) – Unemployment rate

- Top Ten Global Risks for 2025 • Stimson Center

- Hit by Trump trade wars, U.S. economy falls 0.2% in first quarter, an upgrade from initial estimate – AP News

- Global Supply Chain Disruptions in 2025: Causes, Effects, and Resilience Strategies

- What Is the Probability of a Recession? | J.P. Morgan Research

- Top 5 Geopolitical Threats to Businesses in 2025 – SHRM

- Top geopolitical risks 2025 – KPMG agentic corporate services

- 2025 Geostrategic Outlook | EY

- Global trade 2025 – Chatham House

- www.blackrock.com

- Energy Insecurity in Ukraine: An Overview of Humanitarian and Socio-Economic Impacts, March 2025 – ReliefWeb

- Russia-Ukraine Conflict in 2025: Scenarios and Global Impacts – MAX Security

- Conflicts to Watch in 2025 amid Global Focus on Trade War | Steptoe

- Moody’s credit outlooks: research, analysis, and insights

- Geopolitics in 2025: Risks, opportunities, and deepening uncertainties

- A new US-Africa blueprint for Trump amid China’s rise – Brookings Institution

- Top 10 geopolitical risks in 2025 Geostrategic Outlook | EY – US

- Chatham House Expert Reveals What’s Changed in Africa in 2025. | YIP Institute

- Foresight Africa 2025-2030 – Brookings Institution

- The end of exceptionalism – HSBC Asset Management Denmark

- Supply chain outlook 2025: Key trends and risks to follow

- Global Energy Outlook 2025: Headwinds and Tailwinds in the Energy Transition – Resources for the Future

- Global Debt 2025: Rising Risks Ahead – Clairinvest

- Debt is Higher and Rising Faster in 80 Percent of Global Economy

- 2025 Global Investment Outlook | Franklin Templeton

- Best Asset Allocation Strategies For Investors In 2025 (+Examples) | The Luxury Playbook

- 2025 Year Ahead Investment Directions | BlackRock

- 2025 Mid-year Outlook Comfortably Uncomfortable – J.P. Morgan

- Asset allocation in 2025: Between optimism and uncertainty – Candriam

- privatewealth.goldmansachs.com

- 2025 Outlook: Keep on Truckin’ | Marcus by Goldman Sachs®

- UBS House View Monthly Letter | April 2025

- Asset allocation: An eventful start to 2025 | UBS Global

- Global Midyear Investment Outlook 2025: All Eyes on the U.S. …

- 2025 Private Markets Outlook | Adams Street Partners

- Institutional Investors Split on U.S. Economic Outlook – Commonfund

- Institutional Investor Indicators: April 2025 | State Street

- Institutional Investor Indicators: March 2025 – State Street

- Digital Economy Outlook 2025 – Moody’s

- A new era: Healthcare investing and AI in 2025 | Aberdeen

- 2025 State & Future of the Power Industry – Guidehouse

- Top Emerging Market Economies for US Investors in 2025 – Nomad Capitalist

- May 2025: Global consumer confidence remains muted – Ipsos

- US consumer confidence rebounds after five straight months of declines amid tariff anxiety – AP News