Nepal’s Insurance Market on the Verge of Transformation

Rationale for the study

The insurance market of Nepal, despite its significant potential, has long remained in the shadows, like a “sleeping giant”. The relevance of its awakening and dynamic development today is difficult to overestimate. In the context of growing economic uncertainty, aggravated by climate change and new technological challenges such as cyber threats, insurance is becoming not just a financial instrument, but a vital element of the economic stability and social well-being of the nation. Nepal’s economy has traditionally relied on agriculture, which provides employment for a large part of the population and makes a significant contribution to the GDP.1, and on money transfers from labor migrants.2Both of these pillars of the national economy are exposed to serious risks. The agricultural sector suffers from the effects of climate change, including droughts, floods and other natural disasters, while the flow of remittances can be unstable due to global economic downturns or political changes in the host countries. In this context, insurance is a key risk management mechanism that can increase the resilience of both individual households and the economy as a whole. Current low penetration of insurance services8 indicates a huge untapped potential of the market, which, with the right approach, can become one of the drivers of economic growth.

Objectives and tasks of the study

This study aims to develop a comprehensive roadmap for the development of the insurance market in Nepal. The main focus is on two key areas: the introduction of innovative insurance products that meet modern challenges and a systematic increase in the level of financial literacy of the population as a foundation for conscious demand for insurance services. The objectives of the study include:

- An analysis of the current status of the Nepalese insurance market, its structure, regulatory environment and key barriers to growth.

- Assessment of the macroeconomic and socio-cultural context influencing the development of insurance.

- A detailed examination of the prospects for the implementation and development of agricultural insurance and cyber risk insurance as priority innovative areas.

- Development of strategies and practical measures to improve financial literacy and public confidence in insurance institutions.

- Formulation of specific recommendations for government agencies, insurance companies and other stakeholders.

Methodology

The study is based on the analysis of secondary data obtained from a wide range of sources. These include official reports and statistics from the National Bank of Nepal (NRB), Nepal Insurance Authority (NIA), Ministry of Finance and other government agencies. Publications of international organizations such as the World Bank (WB), International Monetary Fund (IMF), Asian Development Bank (ADB), Food and Agriculture Organization of the United Nations (FAO) were also used. An important part of the source base was made up of scientific articles, industry studies and analytical materials on the economy, finance and insurance in Nepal and developing countries.

Report structure

The report is divided into several key sections. The introduction is followed by an analysis of the macroeconomic and socio-cultural context of Nepal. This is followed by an overview of the current state of the country’s insurance market. The central sections are an analysis of the potential of innovative products – agricultural insurance and cyber insurance, as well as strategies for improving financial literacy. The report concludes with regulatory and policy recommendations, marketing strategies, and a roadmap for market development with specific activities.

Macroeconomic and Sociocultural Context of Nepal: Foundation for Insurance Growth

A. Nepal Economic Outlook 2024-25

Nepal’s economic outlook in 2024-25 is characterized by moderate growth and relative stabilization after previous periods of volatility. GDP growth projections for fiscal year 2024/25 range from 3.3% to 4.9%, according to estimates from various national and international institutions.11For example, the World Bank forecasts growth of 4.5% in FY25.16while the Nepalese government in its economic survey indicated an expected growth of 4.61%.17Inflation is also showing a downward trend, approaching the central bank’s target of 4.72%-5.5%.18Nepal Rastra Bank (NRB) has been pursuing a cautiously accommodative monetary policy by cutting its key interest rate to 5%, which is aimed at stimulating economic activity.

The country’s foreign exchange reserves are at a sufficient level, capable of covering imports of goods and services for more than 12-17 months. This ensures a certain macroeconomic stability and the stability of the national currency, which is an important factor for insurance companies, especially when working with international reinsurers. However, Nepal’s economy still faces structural challenges, such as a significant trade deficit and high dependence on remittances from migrant workers, which constitute a significant share of GDP (about 25% of GDP in 2023, according to the World Bank21, and according to NRB, remittance inflows for the 9 months of FY2024/25 amounted to NPR 1191.31 billion). This dependence makes the economy vulnerable to external shocks and may create risks associated with the so-called “Dutch disease”22, when the inflow of foreign currency from one sector (remittances) can negatively affect the competitiveness of other sectors of the economy, including agriculture and industry.

Table 1: Key Macroeconomic Indicators of Nepal (2024-25 Forecast)

Moderate economic growth and stabilization of inflation create a generally favorable background for the development of financial services, including insurance. Increased consumer and business confidence, as well as the potential release of funds from households and businesses due to lower interest rates, can stimulate demand for insurance products. However, structural vulnerabilities of the economy highlight the urgent need for effective risk management tools, which are insurance services.

Global economic trends have a significant impact on Nepal. Forecasts by international organizations (IMF, World Bank, OECD) for 2025 indicate a slowdown in global economic growth and continued uncertainty.26Trade wars, especially between the US and China33, and geopolitical conflicts create additional volatility in global markets. This may affect Nepal through foreign trade channels (impact on the cost of imported goods and raw materials), remittances, and tourist flows. In such circumstances, the importance of internal mechanisms for ensuring economic resilience increases, and insurance can play an important role here, helping to mitigate the effects of external shocks.

B. Demographic and social factors

Nepal’s demographic structure is characterized by a predominantly young population.35This represents a significant potential market for long-term insurance products such as life, health and pension insurance. However, engaging young people requires tailored products and modern communication channels, given their greater openness to digital technologies. Urbanization continues, but a significant portion of the population (about 63-79%, according to various estimates) still lives in rural areas.35

Agriculture dominates the employment sector, employing between 50.4% and 65% of the active population.1This indicates a high potential demand for agricultural insurance. One of the serious social problems is the “brain drain” – the mass labor migration of skilled specialists and young people abroad in search of better economic opportunities.37This phenomenon not only reduces the country’s innovative potential, but may also lead to a shortage of qualified personnel for the developing insurance industry, especially for the development and underwriting of complex products.

The financial literacy level of Nepal’s population remains relatively low. According to the NRB survey, the overall financial literacy rate is 57.9%.42There are significant gaps in financial knowledge (average score 47.3%) and financial behavior. This directly impacts demand for insurance products, as the population may not fully understand their value or trust insurance institutions. Research shows that improving financial literacy has a positive impact on making informed financial decisions, including decisions about insurance.43There are significant differences in financial literacy levels across regions (for example, Bagmati province performs better than Madhesh province), age groups (18-30 year olds are more literate) and education levels.42Women also often exhibit lower levels of financial literacy.36This dictates the need to develop targeted educational programs.

Nepal’s cultural characteristics play a significant role in financial decision-making. High levels of trust in personal connections and informal networks (afno manche)44), collectivism and the desire to “save face”46influence interactions with financial institutions. Insurance agents and companies that can build trust with customers and local communities will have a significant advantage. Word of mouth marketing (WOMM) is a powerful marketing tool in Nepal51, and a positive customer experience, particularly in terms of claims handling, can significantly enhance an insurer’s reputation. The cultural characteristic of “saving face” can make customers reluctant to express dissatisfaction directly, which requires companies to be proactive in collecting feedback and resolving problems.

C. Technological development and infrastructure

Nepal’s digital penetration rate has been steadily growing. As of early 2025, internet penetration has reached 55.8%, and the number of active mobile connections exceeds 132% of the total population. There has been an exponential growth in the use of digital payment systems such as eSewa (over 12 million app downloads)53), Khalti and IME Pay (each with about 5 million users54), as well as Fonepay.55The popularity of QR payments is growing.57This creates favorable conditions for the development of InsurTech, mobile insurance and simplified customer interaction processes. However, the digital divide between urban and rural areas remains59, which requires differentiated strategies to ensure access to digital insurance services across the country.

Nepal’s logistics infrastructure, especially in rural and mountainous areas, remains a major challenge.60This directly affects the development of certain types of insurance, particularly agricultural insurance and property insurance in remote areas. Difficulties with transportation and communication make it difficult to conduct risk assessments, monitor insured assets and promptly settle claims. Nepal’s poor performance in the Logistics Performance Index (LPI)64 are a confirmation of these problems. Improving the logistics infrastructure is a prerequisite for the effective functioning and reduction of operating costs of insurers.

Current State of Nepal’s Insurance Market: “Sleeping Giant”

A. Market structure and key players

The insurance market in Nepal consists of companies operating in the life, non-life, micro-insurance and reinsurance segments.66 As of mid-2024-25 fiscal year, there were 13 life insurance companies, 12 non-life insurance companies, two reinsurance companies and three micro-insurance companies operating in the country.66

The market is characterized by a certain degree of concentration, especially in the life insurance segment, where Nepal Life Insurance Company is the leader, having collected NPR 36.59 billion in premiums in the first 10 months of the current financial year. Among non-life insurance companies, Shikhar Insurance stands out with the largest market share in terms of gross premiums (around 12-13%).68 Recently, there have been mergers and acquisitions that may lead to further consolidation of the market.68 The emergence of specialized micro-insurers 70 is a positive signal indicating the desire of the regulator and market participants to expand the coverage of insurance services to previously unserved segments of the population, especially in rural areas and among low-income groups.

B. Insurance penetration and density

Despite some growth in recent years, insurance penetration in Nepal remains low compared to other South Asian countries and emerging markets in general. According to the Nepal Insurance Authority (NIA), the overall insurance penetration rate reached 47.39% as of mid-May 2025.9 However, this figure includes specific types of insurance such as micro-insurance, short-term insurance, and overseas employment insurance. When only traditional life insurance policies are considered, the penetration rate is significantly lower, at about 16.77%.8

There has been a positive growth trend in insurance premiums in recent years. For example, in the first 10 months of the current fiscal year 2024/25, life insurance premiums collected grew by 15.55% year-on-year to reach NPR 140.35 billion.9 Total premiums for the entire sector (life and non-life) in the first month of the current fiscal (till mid-Baisakh) stood at NPR 1.76 trillion, up 14.03% year-on-year.72 These figures suggest potential for growth, but the low base and dominance of specialty lines of insurance in the overall coverage support the ‘sleeping giant’ thesis.

Table 2: Insurance penetration and density rates in Nepal (mid-2025)

Note: Data on insurance density (premium per capita) require additional calculation based on total premiums and population.

A comparison with other countries in the region shows that Nepal has room for improvement. For example, in India, the insurance penetration rate (total) was around 4.2% of GDP in 2022-23, which is higher than Nepal if only traditional products are considered. This indicates significant scope for market expansion through awareness, accessibility, and development of relevant products.

C. Product Offering

The range of insurance products offered in the Nepalese market mainly includes traditional types of insurance. In the life insurance segment, these are endowment, risk and term insurance. In non-life insurance, auto insurance, property insurance, health insurance and various types of liability insurance predominate.

The new Insurance Regulation 2081 (2025 AD) has expanded the classification of products to include, for example, term life insurance, home insurance, business insurance, transport insurance, as well as specialised products such as agricultural insurance, livestock insurance and herbal insurance. This demonstrates the regulator’s intention to encourage diversification of the product offering.

Microinsurance stands out as a rapidly growing segment targeting low-income and rural populations.70 NIA has licensed specialized microinsurance companies to help develop and promote affordable and simple insurance solutions for this target audience.

However, innovative products such as parametric insurance (based on weather indices or crop yields) or comprehensive cyber risk insurance for businesses are still virtually non-existent or at a very early stage of development. The potential for their implementation is huge, given the vulnerability of agriculture to climate change and the growing digitalization of the economy.

D. Distribution channels

Traditionally, agent networks have been the dominant channel for selling insurance products in Nepal. Insurance agents play a key role in establishing personal contact with customers, explaining policy terms and collecting premiums, especially in an environment where financial literacy is low. However, the effectiveness of agent networks, especially in remote rural areas, can be limited by high transaction costs and logistical challenges.

Bancassurance, or the sale of insurance products through banking channels, is also gaining popularity. Many commercial banks in Nepal have partnered with insurance companies to offer insurance products to their customers.15 For example, Himalayan Bank has partnered with MetLife, LIC Nepal, and a number of non-life insurance companies80, while Nabil Bank offers insurance products in partnership with Sanima GIC Insurance Ltd. and MetLife.79 This channel has significant potential for growth given the banks’ wide branch network and existing customer base. However, its successful development requires closer integration of processes, simplification of product offerings, and training of bank staff.

Online sales channels and digital platforms are still in their infancy, but their role is rapidly growing amid the overall digitalization of financial services in Nepal.58 The rise of mobile banking and digital wallets is paving the way for direct sales of simple insurance products via the internet and mobile apps. Insurance brokers are also present in the market, but their share is still small.

Developing alternative distribution channels, such as partnerships with cooperatives, microfinance institutions (MFIs) and retailers, especially to promote microinsurance products, can significantly expand the reach of insurance services, especially in rural areas.82

E. Regulatory environment

The Nepal Insurance Authority (NIA), formerly known as the Insurance Council (Beema Samiti), plays a key role in regulating the insurance market in Nepal. The NIA is responsible for licensing insurance companies, formulating regulations, supervising their activities, and protecting the rights of insurance consumers.

In recent years, the regulator has been actively working to modernise the regulatory framework. The new Insurance Act 2079 (2022 AD) 76 was passed, which expanded the powers of the NIA and laid the foundation for further development of the market. The NIA has issued a number of important directives, including the Uniform Directives for Insurers 84, the Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) Directives 86, and regulations pertaining to micro-insurance.70 In 2025, the Insurance Regulations 2081 (2025 AD) were enacted, which detailed many aspects of the activities of insurers, including product classification and requirements for foreign investors.

NIA also focuses on corporate governance, risk management and the implementation of international financial reporting standards. It plans to move from compliance-based supervision to risk-based supervision (RBS).76

In terms of consumer protection, the NIA is responsible for handling complaints against insurance companies. It recently announced the creation of a special judicial panel under the NIA to expedite the resolution of insurance claim disputes.87 This is an important step, given the growing number of complaints of delays and denials of claims, especially in the case of mass events such as floods and landslides.87 The issue of misselling is also on the radar of the regulator.89

For securities market participants, including brokers, the Securities Exchange Board of Nepal (SEBON) is also introducing new rules on capital, licensing and permitted activities, which may indirectly affect the investment activities of insurance companies.90

F. Key Challenges and Barriers to Growth

Despite positive developments, Nepal’s insurance market faces a number of serious challenges that hinder its full development:

- Low level of public awareness and trust: A significant portion of the population, especially in rural areas, is poorly informed about the benefits of insurance and does not trust insurance companies, which is a result of both a lack of information and negative experiences.10

- Lack of financial literacy: The overall level of financial literacy remains low, making it difficult to understand complex insurance products and assess risks.42

- Limited access to services: In rural and remote areas, physical access to insurance company offices and agents is difficult.10

- Problems with claims settlement and misselling: Delays and difficulties in receiving insurance payments, as well as cases of unfair sales of policies, undermine confidence in the sector.87

- Shortage of skilled workers: The market is experiencing a shortage of professional underwriters, actuaries and risk management specialists, which limits the ability to develop and implement complex and innovative products.39

- Weak infrastructure: Insufficient development of logistics and telecommunications infrastructure in some regions creates obstacles for insurers’ operational activities and risk assessment.60

- Cultural barriers: Traditional attitudes and preference for informal mechanisms of mutual aid and support within the community or family may reduce the perceived need for formal insurance.46

Overcoming these barriers requires a comprehensive and coordinated approach from all market participants – the regulator, insurance companies, educational institutions and the public.

Innovative Insurance Products: Catalysts for Growth in Nepalese Market

A. Agricultural insurance: protection of the main sector of the economy

Agriculture is the cornerstone of Nepal’s economy, contributing a significant share of GDP (ranging from 24.1% to 31.7% according to various estimates1) and employment for more than half of the country’s population (from 50.4% to 65%1). This dependence makes the economy particularly vulnerable to risks inherent in the agricultural sector, such as adverse weather conditions (droughts, floods, hail), plant and animal diseases, and fluctuations in market prices. In this context, agricultural insurance is not just a financial instrument, but a strategic necessity for ensuring food security and income stability for farmers.

The Government of Nepal recognizes the importance of agricultural insurance and has implemented programs to subsidize insurance premiums for farmers.98These programs are aimed at reducing the financial burden on farmers and stimulating demand for insurance services. In particular, a subsidy of up to 80% of the insurance premium for certain types of agricultural insurance is provided.101However, the effectiveness of these programs is limited by a number of factors, including problems with the targeting of subsidies, which do not always reach small and most needy farmers.102, bureaucratic complexities and the concentration of subsidies on a limited list of crops, primarily rice and wheat.107

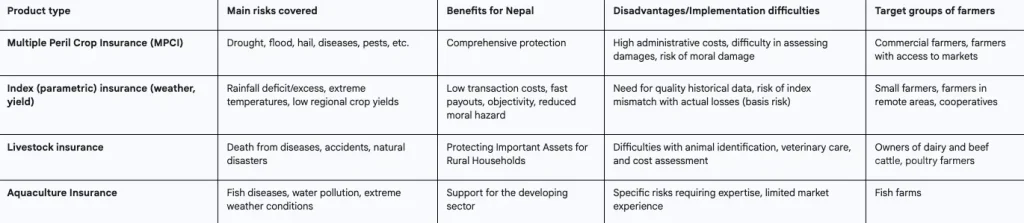

Various types of agricultural insurance products are relevant for Nepal. Traditional Multi-Peril Crop Insurance (MPCI) provides comprehensive coverage, but its implementation is associated with high administrative costs and difficulties in assessing losses on a farm-by-farm basis. In Nepal’s context, characterized by smallholder landholding, geographical fragmentation, and limited resources for detailed underwriting, MPCI may be more promising index (parametric) insurance. Such products are based on objective and easily measurable indices, such as the amount of precipitation in a given area, average temperature, the vegetation index (NDVI), or the average crop yield in a region. Payments under such policies are made automatically when the index reaches a threshold value, which significantly simplifies the process of settling losses and reduces the risk of moral damage and anti-selection. Livestock insurance is also an important area, given the role of livestock in the rural economy.

The implementation of agricultural insurance in Nepal faces a number of challenges:

- Lack of reliable data: The lack of detailed historical data on crop yields, weather conditions and other parameters at the local level makes it difficult to accurately assess risks and develop adequate insurance products, especially index ones.

- Low awareness among farmers: Many farmers are not aware of the options and benefits of insurance or do not trust insurance companies.109

- Difficulties with risk assessment and loss adjustment: Especially in remote and hard to reach areas.

- Availability and cost: Even with subsidies, the cost of insurance policies can be high for small, low-income farmers.

International experiences, such as those of India and Bangladesh, where various agricultural insurance models, including index products and public-private partnership schemes, are actively developing, could be useful for Nepal.

Technology is playing an increasingly important role in modernizing agricultural insurance. Satellite monitoring, the use of unmanned aerial vehicles (drones) to assess crop conditions and damage, and mobile applications for farmers can significantly improve the efficiency and accessibility of insurance services. In Nepal, there are already examples of successful use of agricultural technology, such as the GeoKrishi platform and the Kisan App.112, which provide farmers with agricultural advice, weather information, and market prices. Integrating such platforms with insurance products could create synergies, making it easier for farmers to access insurance and increasing its value. Satellite data and drones can provide objective and rapid damage assessments, which is especially relevant for parametric insurance and for work in hard-to-reach mountainous areas.

Table 3: Comparative Analysis of Potential Agricultural Insurance Products for Nepal

B. Cyber Risk Insurance: Protecting the Growing Digital Economy

With Nepal’s economy accelerating digitalization, growing internet usage, and the rapid adoption of digital financial services, cybersecurity issues are coming to the forefront. Cyberattacks and data breaches are on the rise in the country113highlights the growing vulnerability of both public and private sector organisations, including the financial sector and small and medium enterprises (SMEs). Recent incidents include the Foodmandu and Vianet Communications customer data breaches117, as well as attacks on banking systems (for example, the incident with NIC Asia Bank and the NEPS system117), emphasize the relevance of the problem.

Despite this, the cyber insurance market in Nepal is relatively undeveloped. The main types of cyber threats that Nepalese companies face include personal and financial data breaches, ransomware attacks, distributed denial of service (DDoS) attacks, and phishing.116Potential demand for cyber insurance exists from financial institutions, IT companies, e-commerce enterprises, digitally active SMEs, and government organizations storing large volumes of sensitive information.

Cyber insurance products could cover a wide range of risks, including:

- Liability to third parties in the event of data leakage.

- Losses from business interruption due to a cyber attack.

- Data and system recovery costs.

- Incident response costs, including forensics, legal support and customer notification.

- Damage from cyber extortion.

However, implementing cyber insurance in Nepal faces a number of challenges:

- Insufficient data to assess risks: The lack of comprehensive statistics on cyber incidents and their consequences makes it difficult for insurers to adequately assess risks and set tariffs.

- Low business awareness of the product: Many companies, especially SMEs, underestimate cyber threats or are unaware of the existence of insurance solutions.

- High cost of policies: Cyber insurance can be perceived as an expensive product, especially for SMEs with limited budgets.

- Shortage of local specialists: Lack of qualified personnel in the field of cybersecurity and cyber risk underwriting in insurance companies.122

The development of the cyber insurance market requires close cooperation between insurers, IT companies specializing in cyber security, and government regulators. It is necessary to create databases of incidents, develop industry standards for cyber security, and raise business awareness of risks and available insurance solutions. The government could play a stimulating role, for example by introducing requirements for the availability of cyber insurance for certain critical industries or providing methodological support to insurers.

Improving Financial Literacy and Consumer Confidence: The Key to the Mass Market

A. Assessing the Current Level of Financial Literacy in Nepal

The level of financial literacy of the population is one of the fundamental factors determining the demand for insurance and other financial services. A study conducted by the National Bank of Nepal (NRB) showed that the overall financial literacy level in the country is 57.9%.42This indicator was calculated based on the assessment of financial knowledge, financial behavior and financial attitudes. The financial knowledge component received the lowest score – 47.3% (3.31 points out of 7), while financial behavior was assessed at 63.5% (5.71 out of 9), and financial attitudes – at 64.1% (2.56 out of 4).42Only 27.5% of the adult population achieved the minimum target for all three components of financial literacy simultaneously.

The study also found significant disparities in financial literacy levels among different groups of the population. Bagmati province had the highest level, while Madhesh province had the lowest results. The younger generation (18-30 years) had higher financial knowledge (63.2%) compared to the older age group (60 years and above – 27.9%).42There is also a direct correlation between the level of formal education and financial literacy. World Bank data on Nepal also highlights the need to improve financial literacy, especially in the context of using digital financial services.95These findings highlight the need to develop targeted education programmes that take into account the specificities of different demographic and social groups, including rural residents, women, youth and those with low levels of education, who are often the most vulnerable.

B. The Impact of Financial Literacy on Demand for Insurance Services

Financial literacy directly impacts the ability of the population to understand the concept of risk, recognize the need for financial protection, and make informed decisions about purchasing insurance products. People with higher levels of financial knowledge have a better understanding of how insurance works, what risks it covers, and why it is important to have an insurance policy. They are also better able to compare different insurance offers, analyze contract terms, and choose products that best suit their needs and financial capabilities.43

Improving financial literacy helps build trust in insurance institutions.125 When consumers understand the principles of insurance and see its value, they are more likely to trust insurers and use their services. In contrast, a lack of knowledge can lead to misunderstandings, unreasonable expectations, and, as a result, disappointment and mistrust, especially in the event of an insured event and the claims process. Investments in improving financial literacy are therefore direct investments in increasing demand for insurance services and developing the insurance market as a whole.

C. Strategies for Improving Financial Literacy

To effectively improve financial literacy in Nepal, a comprehensive and multi-level approach that involves various stakeholders is needed.

- Development and implementation of national programs: The coordinating role should be played by government agencies such as NRB, Ministry of Finance, Ministry of Education and NIA.21A national financial education strategy with clear objectives, target audiences and monitoring mechanisms needs to be developed.

- Integration into the education system: Financial literacy fundamentals, including basic concepts of insurance, risk management and personal finance, should be integrated into school and university curricula.21This will allow the younger generation to develop the necessary knowledge and skills from an early age.

- Use of media and digital channels: Extensive use of mass media (TV, radio, print media) and digital platforms (websites, social media, mobile apps) to conduct educational campaigns, disseminate information materials and interactive learning tools.128Content must be accessible, understandable and adapted to different target groups.

- Active participation of insurance companies and agents: Insurers and their agents have direct contact with potential and existing customers and should play an active role in their financial education, explaining product terms, insurance principles and the importance of risk management.

- Involvement of non-governmental and public organizations: NGOs and community-based organizations can make a significant contribution to reaching vulnerable groups with financial education, including rural residents, women and ethnic minorities, using adapted methodologies and approaches.

D. Strengthening confidence in the insurance sector

Trust is the cornerstone of the insurance business. Without it, even the most innovative products and high levels of financial literacy cannot ensure sustainable market growth. The following steps should be taken to build trust in Nepal’s insurance sector:

- Increasing transparency of insurers’ activities: Publishing regular and clear reports on financial performance, investment structure, and claims handling practices. NIA has already started publishing monthly industry data, which is a step in the right direction.130

- Simplification of insurance products and contract terms: Insurance policies should be written in clear and understandable language, without hidden conditions and complex wording. NIA is working to unify guidelines and can help simplify products.70

- Improving customer service: This includes prompt response to requests, professionalism of agents, ease of interaction at all stages – from product selection to settlement of losses.47Particular attention should be paid to first impressions and building long-term relationships.

- Effective and fair settlement of losses: Delays, unjustified refusals or underpayments are the main reasons for customer dissatisfaction and undermine confidence in the entire market.87The creation of a judicial panel at the NIA is an important step, but internal improvements are also needed within companies.

- Combating misselling and unfair practices: There is a need to tighten controls over the activities of agents, ensure full disclosure of information about products and prevent the imposition of unnecessary or inappropriate services.89

- Effective work of the regulator to protect consumer rights: NIA must promptly respond to consumer complaints, conduct investigations and impose sanctions on violators.86

Only comprehensive and consistent efforts by all stakeholders to improve financial literacy and build trust will help unlock the enormous potential of Nepal’s insurance market.

Regulatory and policy recommendations to stimulate the market

A. Improving the regulatory framework

To stimulate the development of the insurance market in Nepal and the introduction of innovations, the regulatory environment should not only be supervisory but also supportive. Key areas for improving the regulatory framework include:

- Further development of risk-based supervision (RBS): NIA is already declaring a transition to RBS.76This approach will allow the regulator to allocate resources more efficiently, focusing on the most significant risks to financial stability and consumer protection, and will reduce the excessive regulatory burden on low-risk companies.

- Simplifying licensing procedures for innovative products and InsurTech startups: Current procedures may be too cumbersome for new players and innovative solutions. More flexible and faster mechanisms for bringing new products to market should be created, especially in areas such as microinsurance, parametric insurance and digital solutions. The NRB is already creating an innovation hub for fintech, and similar initiatives could be useful for the insurance sector.

- Creating a Regulatory Sandbox: This is a controlled environment in which InsurTechs and traditional insurers can test innovative products, services and business models under the supervision of the regulator, but with some regulatory requirements temporarily relaxed. This will reduce barriers to entry and promote competition and innovation, especially in new areas such as cyber insurance or the use of artificial intelligence in underwriting.

- Improving legislation in the field of data protection and cybersecurity: With the increasing digitalization of insurance services, the importance of protecting customers’ personal data and ensuring cybersecurity for insurers themselves is growing. Nepalese legislation needs to be brought into line with international standards (e.g. GDPR) and clear requirements for insurers to protect information and respond to cyber incidents need to be established.113This will increase consumer confidence in digital insurance services.

- Adapting regulations to new distribution channels: Clear rules need to be developed for online sales of insurance products, the activities of insurance aggregators and the use of mobile platforms, while ensuring an adequate level of consumer protection.

B. State support and incentives

Targeted government support can play an important role in accelerating the development of priority segments of the insurance market and increasing its accessibility for the population.

- Expansion and improvement of the efficiency of agricultural insurance subsidy programs: Existing programs for subsidizing agricultural insurance premiums98need to be improved. They need to be better targeted, focusing on small and vulnerable farmers, as well as regions most exposed to climate risks. The list of subsidized crops should be expanded to include more than just rice and wheat107, but also other crops important for food security and export, such as legumes and oilseeds.107It is also important to simplify the procedures for receiving subsidies and insurance payments.

- Consideration of the possibility of introducing tax incentives: To stimulate demand for certain types of socially important insurance, tax deductions or exemptions for individuals on long-term life insurance, pension insurance, or health insurance could be considered. Similarly, tax incentives could be provided to small and medium enterprises that purchase insurance against specific risks (e.g., cyber risks or business interruption insurance). Nepal already has tax exemptions for some sectors, including agriculture.98

- Support for the development of infrastructure for data collection: Effective underwriting and pricing, especially for new types of insurance (agriculture, cyber), requires high-quality and detailed data. The state can facilitate the creation or support of national or industry databases on meteorological events, crop yields, cyber incident statistics, etc. This can be implemented through public-private partnerships.

C. Development of human resources

Skilled labor shortage is one of the key constraints to growth and innovation in Nepal’s insurance sector.

- Training and Certification Programs: National standards and training programs for insurance agents, underwriters, claims adjusters and actuaries need to be developed and implemented.39Certification should become a requirement for certain positions.

- Cooperation with universities: It is important to establish cooperation between the insurance industry and higher education institutions to develop specialized educational programs in the field of insurance, risk management and actuarial mathematics.96This will help ensure an influx of young professionals into the market.

- Attracting and retaining talent: Insurance companies need to create attractive working conditions and career development opportunities to attract and retain qualified professionals, including in the context of a “brain drain”.

D. Improving the investment climate for the insurance sector

Attracting both domestic and foreign investment into the insurance sector can contribute to its development, increase competition and introduce advanced technologies and practices.

- Ensuring macroeconomic and political stability: Predictability of economic policy and stability of the regulatory environment are key factors for investors.12

- Simplification of procedures for foreign investors: Registration and licensing procedures for foreign insurance companies wishing to enter the Nepalese market should be simplified, while meeting the requirements for their financial strength and experience. This could include creating a one-stop shop for investors and clearly defining the rules of the game.

- Capital market development: A developed capital market provides insurers with more opportunities to effectively manage their investment portfolios, which is important for their financial stability.

Marketing and Distribution Strategies: Reaching the Unreached

A. Adaptation of Marketing Communications to Cultural Specifics of Nepal

Effective insurance marketing in Nepal requires a deep understanding and sensitivity to local cultural specificities. Directly copying Western marketing models is unlikely to succeed.

- Language and cultural images: Communication materials should be in Nepali and use images that are familiar and understandable to the local population.47This applies to both advertising messages and the insurance documents themselves.

- Focus on collective values: In Nepalese society, characterized by strong community and family ties, marketing messages that emphasize the benefits of insurance in protecting the family, securing the future of children and the well-being of the community will be more effective than focusing on individual benefits.47

- Word of Mouth Marketing (WOMM) and Opinion Leaders: Personal recommendations and opinions of trusted people play a huge role in decision making.51Insurance companies should actively work to build a positive reputation, encourage satisfied customers to share their experiences and collaborate with local opinion leaders (teachers, doctors, respected community members, popular bloggers and social media influencers).139). Examples of successful use of WOMM in Nepal include campaigns by brands such as Coca-Cola (“Mann Kholau Coke Sanga”) and the rise of Bajeko Sekuwa.51

- Building Trust: Given the historically low level of trust in financial institutions, the main focus of marketing should be on building long-term trusting relationships, rather than on quick sales. This involves honesty, transparency, and a willingness to meet the client halfway.

B. Development of digital sales and service channels

Digitalization opens up new opportunities to expand coverage and reduce costs in the insurance sector.

- Mobile applications and online platforms: Developing user-friendly and intuitive mobile apps and websites for calculating costs, purchasing policies, managing contracts, filing claims and receiving consultations. An example is the nBank app from Nabil Bank, which offers a wide range of online banking services143, or mobile applications of insurance companies such as Nepal Life Insurance.145

- Use of social networks: Active presence on popular social networks (Facebook, Instagram, TikTok) to promote products, conduct educational campaigns, interact with the audience and handle customer requests.51

- Partnership with fintech companies and payment systems: Integration with popular digital wallets (eSewa, Khalti, IME Pay149) and payment gateways to simplify the process of paying insurance premiums and receiving benefits. This is especially relevant given the rapid growth of digital payments in Nepal.

C. Strengthening the role of insurance agents and brokers

Despite the development of digital channels, the role of insurance intermediaries, especially agents, will remain important, especially when working with the population in rural areas and when selling complex insurance products that require personal consultations.

- Training and professional development: Regular training programs for agents and brokers should cover not only product knowledge but also sales skills, business ethics, customer focus and financial advice fundamentals. It is important to ensure that agents provide clients with complete and accurate information, avoiding misselling.

- Implementation of digital tools for agents: Equipping agents with mobile CRM systems, online calculators, tablets with access to product information and the ability to issue policies “in the field” can significantly increase their efficiency and productivity.

D. Development of alternative distribution channels

To expand the coverage of insurance services, especially in regions with insufficient presence of traditional insurance companies, it is necessary to develop alternative channels.

- Bancassurance: Deepening cooperation between banks and insurance companies. This requires developing simple and understandable insurance products adapted for sale through banking channels, as well as training bank employees in the basics of insurance.15

- Partnership with cooperatives and microfinance organizations: Agricultural and credit cooperatives, as well as microfinance organizations, have an extensive network and enjoy the trust of the population in rural areas.82They can become effective channels for distributing simple microinsurance products such as crop, livestock, or small-value life and health insurance.

- Partnerships with retailers and mobile operators: Selling packaged insurance products (e.g. accident insurance, mobile device insurance) through retail chains or telecom operators.

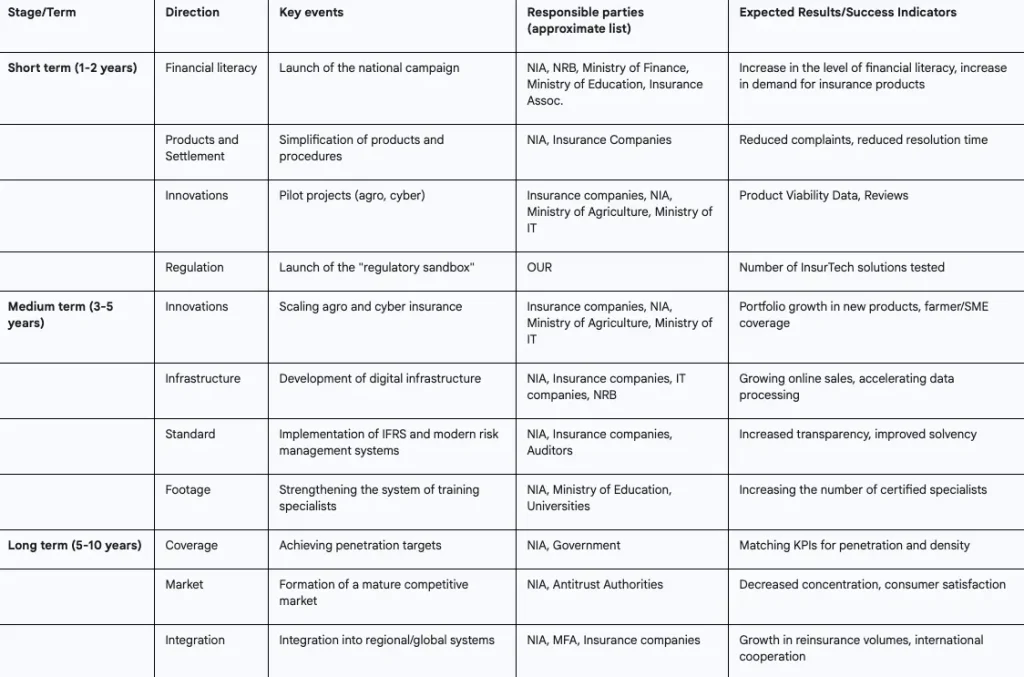

Nepal Insurance Market Development Roadmap: Key Activities and Timelines

A systematic and step-by-step approach is needed to awaken the sleeping giant – Nepal’s insurance market – and realize its enormous potential. The proposed roadmap includes key activities, distributed over time horizons, with possible accountabilities and success indicators.

A. Short-term measures (1-2 years): Laying the foundation

- Launch of a nationwide campaign to increase financial literacy and insurance awareness:

- Events:Development and broadcasting of educational programs on TV and radio, publications in the media, creation of information portals and mobile applications, conducting seminars and trainings in the regions.

- Responsible:NIA, NRB, Ministry of Finance, Ministry of Education, Insurance Associations, Insurance Companies.

- Success indicators:Increased level of financial literacy (according to surveys), increased requests for insurance products, increased traffic to information resources.

- Simplification of existing insurance products and claims procedures:

- Events:Review of regulatory requirements for the content of policies, development of standard “boxed” products with clear terms, introduction of standards for terms and procedures for settling losses. NIA is already working in this direction.70

- Responsible:NIA, insurance companies.

- Success indicators:Reduction in the number of complaints about unclear contract terms, reduction in the average time for settling losses.

- Pilot projects for innovative products (agricultural and cyber insurance):

- Events:Launching pilot projects on index-based agricultural insurance in several climate-vulnerable regions, developing and piloting basic cyber insurance products for SMEs in urban centers.

- Responsible:Insurance companies (with the support of NIA and international partners), agricultural cooperatives, IT associations.

- Success indicators:Number of contracts concluded within the pilots, feedback from participants, assessment of the economic efficiency of products.

- Activation of the “regulatory sandbox”:

- Events:Creation and launch of the NIA “regulatory sandbox” for testing InsurTech solutions and innovative business models.

- Responsible: OUR

- Success indicators:Number of applications and successfully tested projects in the sandbox.

B. Medium-term measures (3-5 years): Development and scaling up

- Scaling up successful pilot projects for innovative products:

- Events:Expanding the geography and product line of agricultural and cyber insurance based on the results of pilot projects, developing subsidy mechanisms for these products.

- Responsible:Insurance companies, NIA, Ministry of Agriculture, Ministry of Information Technology.

- Success indicators:Growth of the portfolio of agricultural and cyber insurance, increasing coverage of farmers and SMEs.

- Development of digital infrastructure for the insurance sector:

- Events:Creation of unified databases (for example, for insurance cases, weather data for agricultural insurance), development of standards for online sales and settlement platforms, development of mobile applications for insurers.

- Responsible:NIA, insurance companies, IT companies, NRB.

- Success indicators:Increase the share of online sales, reduce the time for data processing and loss settlement.

- Implementation of international standards of financial reporting and risk management:

- Events:Phased transition of insurance companies to IFRS, implementation of modern risk management systems (including Solvency II or similar).

- Responsible:NIA, insurance companies, audit firms.

- Success indicators:Increased transparency of reporting, improved solvency indicators.

- Strengthening the system of training and certification of insurance specialists:

- Events:Establishment of a national insurance institute or accreditation of existing training centers, development of training and certification programs for actuaries, underwriters, agents.39

- Responsible:NIA, Ministry of Education, Universities, Insurance Associations.

- Success indicators:Increasing the number of certified specialists on the market.

C. Long-term measures (5-10 years): Achieving market maturity

- Achieving insurance penetration targets:

- Events:Continuous monitoring and adjustment of market development strategies to achieve target penetration indicators (for example, bringing the penetration level of traditional products to the regional average).

- Responsible:NIA, government.

- Success indicators:Achieving established KPIs for insurance penetration and density.

- Formation of a mature and competitive insurance market:

- Events:Ensuring healthy competition, developing diverse products and distribution channels, and a high level of consumer protection.

- Responsible:NIA, antitrust authorities, insurance companies.

- Success indicators:Decreasing market concentration, emergence of new players, high level of consumer satisfaction.

- Integration of Nepalese insurance market into regional and global systems:

- Events:Harmonization of legislation with international standards, development of cooperation with international reinsurers, participation in regional initiatives for the development of insurance.

- Responsible:NIA, Ministry of Foreign Affairs, insurance companies.

- Success indicators:Increasing the volume of incoming and outgoing reinsurance, participation of Nepalese companies in international projects.

Table 4: Roadmap for Nepal Insurance Market Development (Key Activities)

Successful implementation of this roadmap will require political will, coordinated efforts of all stakeholders, as well as continuous monitoring and flexible adaptation to changing conditions.

Conclusion: Realizing Nepal’s Insurance Potential

Nepal’s insurance market truly has the characteristics of a “sleeping giant”. With relatively low current insurance penetration and density, especially in traditional product lines, the country shows significant growth potential. This is supported by moderate macroeconomic stabilization, a young and growing population, and a growing awareness of the need to manage risk in the face of global uncertainty and specific national challenges such as agricultural vulnerability and remittance dependence.

The key drivers for the awakening of this giant should be innovations And Improving financial literacy. The introduction of popular innovative products, such as locally adapted agricultural insurance (including parametric models) and cyber risk insurance for the growing digital segment of the economy, can not only expand the market, but also increase its social and economic significance. However, without a significant increase in the level of financial literacy of the population and strengthening trust in insurance institutions, these innovations will not be able to reach the mass consumer.

The proposed roadmap outlines concrete steps in the short, medium and long term, covering improvement of the regulatory environment, government support for priority areas, development of human resources, and adaptation of marketing and distribution strategies to the unique socio-cultural and technological conditions of Nepal. Particular attention is paid to the need to simplify products, improve transparency of insurers and improve customer service, especially in terms of claims settlement.

The implementation of this ambitious plan requires coordinated efforts from all stakeholders: the government, which must ensure a stable and predictable environment; the regulator (NIA), which must combine effective supervision with incentives for innovation; insurance companies, which must invest in new products, technologies and staff training; educational institutions and public organizations that can contribute to improving financial literacy; and society itself, which must be open to new financial instruments for protecting its well-being.

Despite the existing challenges such as infrastructure limitations, shortage of skilled labor and cultural barriers, the prospects for the development of the insurance market in Nepal look optimistic. Consistent implementation of the proposed roadmap will not only “wake up the sleeping giant” but also turn the insurance sector into one of the significant factors for sustainable economic growth and improving the quality of life of the people of Nepal.

Source used

- agriculture – Investment Board Nepal

- Economy of Nepal – Wikipedia

- Nepal expects 4.61-pct growth for 2024-25 – Xinhua

- Nepal’s economy to grow by 4.61 percent – The Kathmandu Post

- Current Macroeconomic and Financial Situation – English (Based on Nine Months Data of 2024/25) – Nepal Rastra Bank

- Current Macroeconomic and Financial Situation – English (Based on Seven Months Data of 2024/25) – Nepal Rastra Bank

- The Role of Remittances in Household Spending in Rural Nepal – MDPI

- Life insurance access hits record high, yet over half of Nepalis remain uncovered

- Life insurance coverage reaches record 47.39% despite rise in policy surrenders: NIA

- Growing opportunities and challenges for inclusive insurance in Nepal

- Nepal’s Economy Expected to Remain Resilient in Face of Economic Shocks, says World Bank

- Nepal’s Economy Will Likely To Grow By 4.4 In Fiscal Year 2025: ADB

- Publication: Nepal Development Update, April 2024: Nepal’s Economy on a Recovery Path but Private Investment Remains Low

- 2025 Monitoring Report – the United Nations

- MetLife Nepal Launches First-of-its-Kind Double Protection Plus Plan with Dual Benefits

- World Bank projects Nepal’s economic growth at 4.5 percent – myRepublica

- FinMin Presents Economic Survey, Projects 4.61pc growth for current FY

- Nepal Inflation Rate Outlook, Average Consumer Prices (I:NIRA5NJM) – YCharts

- Nepal: Fourth Review Under the Extended Credit Facility Arrangement-Press Release; Staff Report; and Statement by the Executive Director for Nepal in: IMF Staff Country Reports Volume 2024 Issue 225 (2024) – IMF eLibrary

- Nepal Inflation Rate – Trading Economics

- Nepal’s long-term growth may stall below 4 percent, World Bank warns

- Remittance inflows pose Dutch Disease risk in Nepalese economy – CESLAM

- Symptoms of Dutch Disease in Nepal

- Monetary Policy for 2024/25 – Nepal Rastra Bank

- Macroeconomic Snapshot of 9 Months: Inflation at 3.39%; Foreign Reserves Reach USD 17.63 Billion; Remittance Surges 10% – || ShareSansar ||

- World Economic Outlook Update, January 2025: Global Growth: Divergent and Uncertain

- Ayhan Kose Explains the January 2025 Global Economic Prospects – World Bank

- OECD Economic Outlook, Volume 2025 Issue 1

- OECD Economic Outlook, Interim Report March 2025

- Global Economic Prospects, January 2025 – World Bank Open Knowledge Repository

- OECD economic outlook: volume 2025 issue 1

- World Economic Outlook – All Issues – International Monetary Fund (IMF)

- Trump says after Xi call that US and China will resume trade talks

- What to expect from the US-China trade talk? – The World Economic Forum

- Nepal: Population Vulnerability and Resilience Profile – U.S. Census Bureau

- Demographics Of Nepal – Nepal Structural Diary

- Breaking The Cycle Of Brain Drain – The Rising Nepal

- Brain Drain and Its Effects on Livelihood: An Analysis of Phalewas Municipality, Nepal

- Nepal’s Labor Market Dilemma: Bridging the Gap Between Workers and Employers

- How economic inequality is driving youths abroad – The Annapurna Express

- Youth Employment Issues and their Impact on the Economic Development of Nepal

- Baseline Survey on Financial Literacy in Nepal

- (PDF) Behaviour Bias and Investment Decision in Nepalese Investors – ResearchGate

- A Guide to Business Etiquette in Nepal | ClickUp™

- Afno Manche | PDF | Social Network – Scribd

- Cultural Considerations in Nepal – Rivermate

- Customer Satisfaction Score CSAT in Nepal | TCN

- Resource conflicts and conflict resolution in Nepal – HimalDoc

- (PDF) Resource Conflicts and Conflict Resolution in Nepal – ResearchGate

- Nepal’s Workplace Culture “A blend of Respect, Relationships, and Reform” – Learn-Moodle

- Word Of Mouth Marketing: A Great Way People Advertise Digital …

- Social Media Marketing and Brand Awareness of Customers: Evidence from Nepal

- eSewa Pioneering Digital Payments in Nepal – B360 – Business 360°

- Khalti and IME Pay Merger: A threat to eSewa? – GadgetByte Nepal

- Fonepay Sets Record with Over 1 Million QR Transactions in a Single Day

- Fonepay Breaks Records: Over 1 million+ QR transaction in Single-Day – Our Blogs

- QR code drives Nepal’s digital payment boom – The Kathmandu Post

- FinTech innovations: Transforming Nepal’s banking landscape – Onlinekhabar English

- Development in Digital Capitalism: Challenges and Prospects of Nepal

- Why Nepal Struggles to Adopt Better Technology, And Alternative Routes to Development

- Nepal: World Bank Report Outlines Key Reforms to Boost Growth, Create Jobs

- The World Bank in Nepal: Lessons on building institutions and Influencing policy

- What is Last Mile? Complete Guide on Challenges & Future Trends – FarEye

- Nepal ranking in the Global Innovation Index 2024 – WIPO

- International LPI – Logistics Performance Index (LPI) – World Bank

- Insurance companies aggressively expand stock market investments – myRepublica

- Nepali Insurance Sector Sees Steady Growth in Employment and Coverage

- Shikhar Insurance Company Limited: Rating upgraded to [ICRANP-IR] AA-

- Shikhar Insurance becomes second insurer to get ‘Double A Plus’ issuer rating

- Publication of INSURANCE REGULATION 2081 (2025 A.D.) – Pradhan & Associates

- Life insurance coverage reaches record 47.39% despite rise in policy surrenders: NIA

- Insurance Sector Shows Significant Growth in Nepal’s Fiscal Year 2081/82 | NEPSE Trading

- Nepal: World Bank Approves $150 Million to Improve Resilience of Bridge Network, Connectivity, and Access to Services

- Bancassurance in ASEAN Market Size, Share, Trends & Forecast

- Insurance authority issues directives on monetary loss insurance – myRepublica

- Second Strategic Plan 2023-2027 – Nepal Insurance Authority

- Bancassurance Market Size, Share and Growth Report 2034

- IFC’s $56-Million Investment in Global IME Bank to Bolster Gender and Climate Financing in Nepal

- Insurance Benefits of Nabil Dhukka Bachat Khata

- Himalayan Bank Bancassurance

- Himalayan Bank – Annual Report 2016-17

- The Role of Cooperative on the Socio-economic Growth and Stability – Nepal Journals Online

- Cooperatives as Pillar of Economy to Improve Agriculture Production …

- Insurance Authority to Issue Unified Directives for Insurers – Beemapost.com

- Nepal Insurance Authority has 62 types of directives, no unified document

- AML/CFT Directives Archives – the official site of the Central Bank of Nepal

- NIA setting up judicial bench to expedite solving of insurance claims – myRepublica

- NIA to Establish Judicial Bench for Faster Insurance Claim Settlements – ShareSansar

- Reasons for life insurance policy surrender in Nepal and ways to reduce it

- SEBON and SBAN Hold Strategic Discussion; Proposal Submitted to Amend Securities Businessperson Regulations – || ShareSansar ||

- What are the proposals of the Brokers Association to amend the six rules of the regulations before Sebon? – Insurance Khabar

- Securities Issuance and Trading Regulations for Small and Medium Enterprises, 2081 (2025) – T.R. Upadhya & Co.

- SEBON Introduces Broker Merger Directive to Ease Capital Constraints – ShareSansar

- Review on Insurance and their Present Status in Nepalese Economy – ResearchGate

- Nepal – World Bank Data

- Inclusive insurance and risk financing in Nepal Snapshot and way forward 2024 – UNDP IRFF

- Actuarial Profession and Factor Impacting on the Role of Partly Qualified Actuaries in Insurance Companies of Nepal – ResearchGate

- sectoral profile – agriculture – Investment Board Nepal

- A homegrown vision of commercial agriculture in Nepal that puts small-scale farmers at its heart | International Institute for Environment and Development

- Income from agricultural insurance falls after government sets subsidy limit

- Agriculture Insurance

- When Help Hurts – GMC Nepal

- Relationship between Agriculture Subsidy and Agricultural Production in Nepal. – Nepal Journals Online

- 107 billion rupees spent on agricultural subsidy in five fiscal years | The Farsight Nepal

- agricultural support policy of nepal: cases of subsidies – International …

- Assessment of Government Policies, Farm Subsidies, and Agriculture Growth | Request PDF

- Status of fertilizer and seed subsidy in Nepal: review and recommendation

- Status of fertilizer and seed subsidy in Nepal: review and recommendation

- (PDF) COMMERCIALIZATION OF AGRICULTURE: FORMS …

- Agricultural Mechanization in Nepal – IFPRI South Asia

- (PDF) Constraints on the use and adoption of information and communication technology (ICT) tools and farm machinery by paddy farmers in Nepal – ResearchGate

- Nepal | Digital Villages Initiative in Asia and the Pacific | Food and Agriculture Organization of the United Nations

- Sensitive Data of Nepal’s PM’s Office Allegedly for Sale – Cyber Press

- April 2025: Major Cyber Attacks, Ransomware Attacks and Data Breaches

- Global law enforcement action in Asia nets large infrastructure seizure, 32 arrests

- Cyber threats impacting the financial sector in 2024 – focus on the main actors

- A brief study into Cyber attacks and preventive measures in Nepal – ResearchGate

- Data Breaches in Nepal: Understanding the Risks and Solutions – myRepublica

- Nepal’s Digital Frontier: How Safe Are We from Cyber Attacks? – myRepublica

- Digital banking in Nepal: A never-ending blessing or a curse? – OnlineKhabar English News

- Nepal Cybersecurity Job Market: Trends and Growth Areas for 2025

- Best Data Science Courses in Nepal – Stamford College Kathmandu

- What jobs come from data science courses in Nepal – IABAC

- Most Trending IT Courses in Nepal: What’s Hot in 2025 – Presidential Graduate School

- Enhancing Customer Satisfaction in Nepalese Banks and Financial Institutions: The Influence of Service Quality on Different Dim – ResearchGate

- (PDF) Service Quality and Customer Loyalty in Nepalese Commercial Banks: A Mediating Role of Customer Trust – ResearchGate

- Financial Literacy and Digital Payment System in Nepal – ResearchGate

- Assess the Adoption of Improved Maize Production Technologies in Gulmi, Nepal

- ADOPTION OF RIVERBED FARMING TECHNOLOGIES IN KAMALA …

- Nepal: Regulator commences the release of industry data on a monthly basis

- Nepal Insurance Authority begins monthly KPI publication

- Exploring Consumer Satisfaction and Service Quality at Bhatbhateni …

- (PDF) Exploring Consumer Satisfaction and Service Quality at Bhatbhateni Supermarket

- Grievance Handling – Nepal Insurance Authority

- Keep Current Insurance Coverage Growth Going – myRepublica

- April 2025 Analysis – CESIF Nepal

- How Social Media Marketing is Revolutionizing Brand Building in Nepal

- (PDF) Cultural Influences on Consumerism and Lifestyle Choices …

- Influencer Marketing in Nepal: Skyrocket Your Revenue – Digital Gurkha

- Unleashing the Power of User-Generated Content Marketing In Nepal – Uptrendly

- Top 20 Influencers in Nepal in 2025 – Favikon

- Remote Brand Ambassador Jobs in Nepal – Himalayas.app

- nBank on the App Store

- nBank on the App Store

- Nepal Life Insurance – Apps on Google Play

- Nepal Life Insurance

- Social Media Marketing in Nepal: Trends & Opportunities

- Social Media Marketing in Nepal | Build Brand Reputation – Keroneva Design

- Financial Technology Adoption in Nepal – Hamzah Academy

- NIC Asia Bank partners with Khalti to facilitate digital payments – :: Business 360°

- Global IME Bank Partners with IFC to Advance Digital Banking and Fintech in Nepal

- “If I were a fintech entrepreneur in Nepal, I would start by mapping out the existing fintech landscape’ – B360 :: Business 360°